Widening the aperture: Multi-asset investing in a late-cycle economy

Global Head of Multi-Asset Adam Hetts argues that investors should balance the opportunities presented by the extension of the economic cycle with the risks posed by policy uncertainty and elevated valuations when calibrating portfolio allocations in 2025.

8 beknopt artikel

Kernpunten

- Opportunities for incremental risk taking exist in the late-cycle environment as long as one is mindful of valuations and identifies which market segments may benefit from supportive policy.

- Even if the Federal Reserve’s (Fed) rate-cutting trajectory is shallower than anticipated, the global economy is still primed to benefit from less restrictive monetary policy and more stimulus from China.

- In our view, adding risk can be accomplished by broadening equities exposure to include more economically sensitive and leveraged names and by selecting high-yield bonds with attractive income streams and less exposure to rate volatility.

This past year was marked by consequential elections across major democracies and the global economy continuing to adjust to a higher interest rate regime than it had experienced for much of the past 15 years. The ramifications of these developments will be felt well into 2025.

Also extending its influence is a resilient economic cycle. While a robust U.S. economy defied expectations as the Fed battled inflation, economic growth must now balance optimism around rate cuts with downside risks if the anticipated cuts don’t fully materialize. To be determined is the degree to which a change in policy by the incoming U.S. administration could impact domestic and global growth. Another potential tailwind for the global economy is more aggressive stimulus in China.

While many of these developments will be welcomed by investors, the global economy remains late cycle, and any incremental risk taking should be approached with caution. Narrowing the tolerance for error is the surge in riskier assets’ valuations in the wake of the U.S. election. As global monetary policy diverges and economic broadening impacts sectors in varying degrees, investors should seek to balance a security’s ability to benefit from the cycle’s extension with its valuation.

The macro: Diverging cycles

The U.S. economy’s streak of outperforming other advanced countries looks set to continue now that the Fed has begun to lower the cost of capital. This is not, however, the full-throated risk-on environment typically associated with the advent of a new cycle. Employment has proven durable, but the trend – notwithstanding the temporary effects of recent storms – has been downward. Rising consumer delinquencies represent another area of concern.

We remain neutral on Europe, despite signs of steadying consumption. The region’s central banks were earlier than the Fed in lowering rates, but that was due to necessity. China, on the other hand, could break out of an extended stupor now that the central government has initiated more action to address structural issues. Furthermore, the country’s equity valuations do not reflect what we view as an improving earnings backdrop.

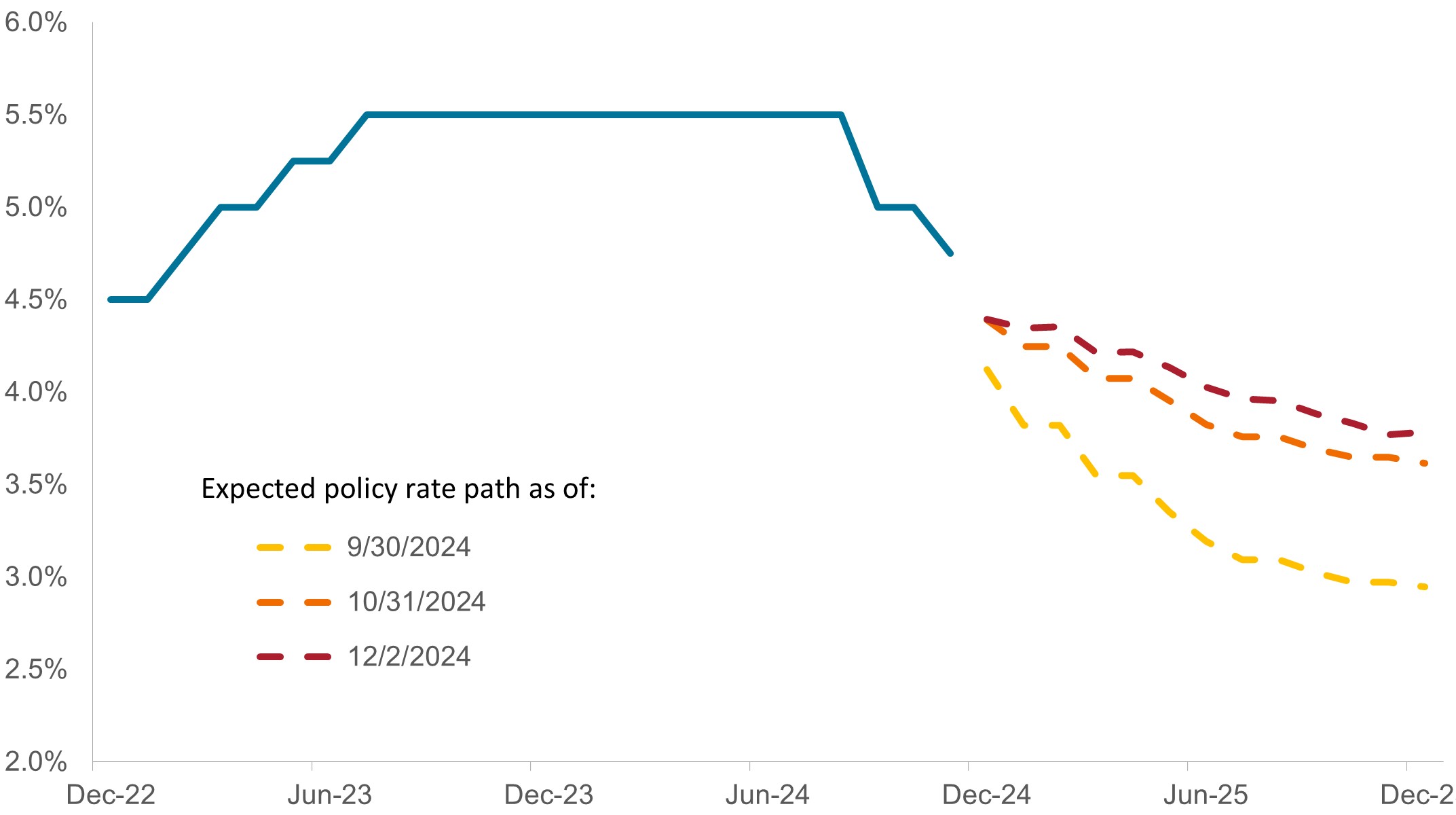

Market’s evolving expectations for Fed’s overnight policy rate

While forward-looking markets’ upwardly revised expectations for the federal funds rate can be viewed as a vote of confidence in the extension of the economic cycle, it also means borrowing costs likely won’t dip to previously anticipated levels.

Source: Bloomberg, Janus Henderson Investors, as at 15 November 2024.

Any shift in U.S. economic policy will undoubtedly reverberate through the corporate sector and financial markets. Deregulatory, corporate tax, and other pro-growth aspects of the incoming administration’s agenda would be favorable for riskier assets. However, tariffs, other policy initiatives or staffing decisions may present risks to growth.

Financials and energy have been highlighted as two sectors that could benefit from more relaxed oversight. The outlook for the tech sector is more nuanced as questions loom over the size and scope of industry behemoths and the protections afforded to social media platforms. Multiple sectors could benefit from a more favorable mergers and acquisitions climate.

Roadblocks to the efficient flow of goods and capital tend to be inflationary, and deterioration of the U.S. fiscal position could spur inflation and put upward pressure on longer-dated interest rates. Pro-growth initiatives would pay off if the rate of economic expansion exceeded the cost of capital but that bar would likely be raised should trade and fiscal policy send interest rates higher.

Equities: Balancing tailwinds and valuations

Although an extension of the cycle should be conducive for riskier assets, we believe that for equities, a modest rotation within the asset class is preferable to increasing overall equities exposure at the expense of core fixed income. Rate cuts stand to benefit small-cap companies that tend to carry more debt. Since they are less dependent on borrowing costs, midcaps don’t necessarily need lower rates to enjoy the tailwinds of economic expansion. The extension of the 2018 tax reform would likely support earnings across the corporate sector.

Valuations are elevated, with most equity segments’ price-to-earnings ratios residing in the top quartile of their long-term average. Despite the possibility of broadening economic growth, value stocks are one of the few categories where earnings estimates still have meaningful potential to grow into their valuations. And although broader participation in the equities rally is a welcome development, investors should not lose sight of the Magnificent 7’s continuing ability to beat expectations and justify their persistently high valuations.

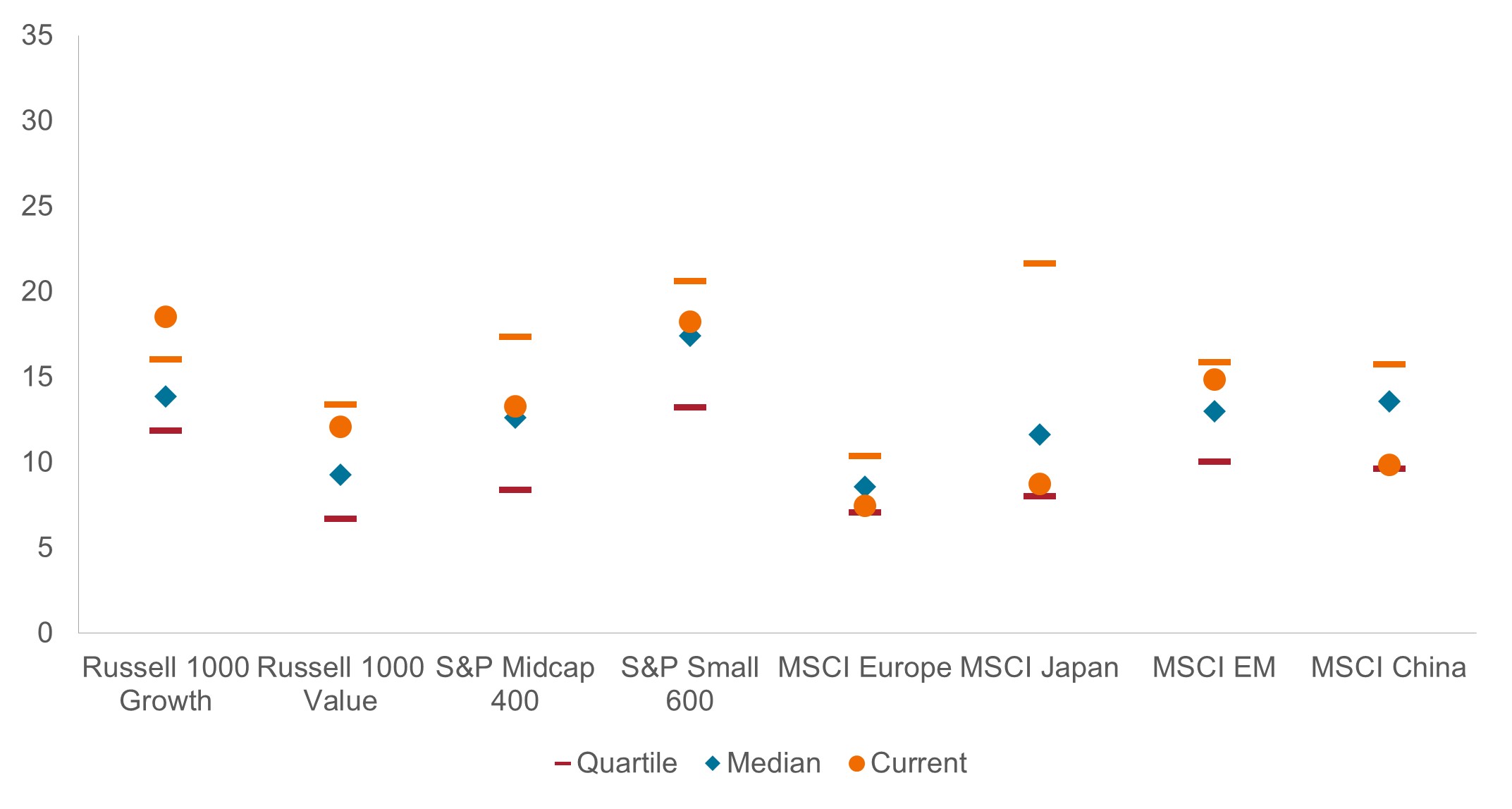

Global 12-month earnings growth forecasts

Although U.S. earnings estimates are above long-term averages – as are price-to-earnings multiples in most markets – more modest expectations for ex-U.S. stocks indicate that earnings may have potential to grow into their valuations.

Source: Bloomberg, Janus Henderson Investors, as at 15 November 2024.

An already tenuous situation for European stocks could worsen should deglobalization accelerate. Still, consumption within the region indicates green shoots, and Chinese stimulus could cast a lifeline to Europe’s capital goods and luxury products exporters. In Japan, any consumption-related benefit from an appreciating yen could be tempered by headwinds for its sizeable export sector.

Fixed income: Navigating a higher and tighter environment

The price of fighting inflation was steep for bond investors. But with most of that battle behind us, the new – higher – range of bond yields globally has left the asset class in a better position to deliver steady income, diversification to riskier assets and, in certain jurisdictions, the potential for capital appreciation.

In the U.S., the Treasuries yield curve reset to higher levels and steepened in the wake of November’s election. Should the market’s forecast of notably fewer rate cuts prove correct, shorter-date bonds will have lost a promising tailwind. In only a few weeks, the anticipated terminal rate for this cycle has reset to a materially higher range of 3.5% to 4.0%. Although having already sold off, longer-dated bond yields could face additional pressure if economic growth further surprises to the upside or trade policies and robust wages prove inflationary.

Corporate credits are richly valued, with the difference between their yields and those of their risk-free benchmarks the tightest since 1997. A candidate for incremental allocation in this space would likely be higher-quality, high-yield issuers, as this category provides more carry, a larger yield cushion, and stands to benefit from lower borrowing costs. Corporate defaults trending lower indicates that issuers have withstood the most intense period of restrictive financial conditions. At current spreads, the interest rate sensitivity of investment-grade credits in a still-volatile Treasuries market cannot be ignored. Securitized credits, by contrast, appear more fairly valued and stand to benefit from rising values of their underlying assets.

U.S. and European corporate spreads

Fed rate cuts and a resilient corporate sector have left bond valuations elevated, but within the space, high-yield issuance has the potential to provide additional carry and less sensitivity to moves in a still-volatile rates market.

Source: Bloomberg, Janus Henderson Investors, as at 15 November 2024.

Outside the U.S., diverging economic fortunes and monetary policy create opportunities. Europe, for example, likely has little choice but to continue its accommodative course. Higher U.S. rates and the accompanying dollar strength, however, would present a challenge for emerging market issuers dependent upon financing in the U.S. currency.

Carry is het extra rendement dat een belegging met een hoger rendement heeft opgeleverd ten opzichte van een andere belegging.

Kredietspread is het renteverschil tussen effecten met dezelfde looptijd maar van verschillende kredietkwaliteit. Verruimende spreads betekenen over het algemeen dat de kredietwaardigheid van zakelijke kredietnemers verslechtert, verkrapping betekent dat deze verbetert.

Diversificatie garandeert geen winst. Ook neemt diversificatie het risico op beleggingsverliezen niet weg.

Excess Return indicates the extent to which an investment out- or underperformed an index.

Monetair beleid verwijst naar het beleid van een centrale bank dat erop gericht is de inflatie en de groei van een economie te beïnvloeden. Dat houdt onder meer in dat de rentevoeten en de geldtoevoer onder controle worden gehouden.

De koers-winstverhouding (K/W) meet de aandelenkoers in verhouding tot de winst per aandeel voor een of meer aandelen in een portefeuille.

Volatiliteit is een maatstaf voor het risico op basis van de spreiding van de rendementen voor een bepaalde belegging.

Een rentecurve geeft de rendementen (rente) weer van obligaties met dezelfde kredietkwaliteit, maar met verschillende vervaldata. Obligaties met langere looptijden hebben meestal hogere rendementen.

Belangrijke informatie

Energiebedrijven kunnen heel gevoelig zijn voor schommelingen in de energieprijzen en in de vraag naar en het aanbod van brandstoffen, natuurbehoud, het succes van exploratieprojecten en fiscale en andere reglementering.

Aandelen brengen risico's met zich mee, waaronder marktrisico's. Rendementen fluctueren als reactie op ontwikkelingen bij de emittent en in de politieke en economische situatie.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Vastrentende effecten zijn onderhevig aan het rente-, inflatie-, krediet- en wanbetalingsrisico. De obligatiemarkt is volatiel. Als de rentes stijgen, dalen de obligatiekoersen meestal en vice versa. Terugbetaling van de hoofdsom is niet gegarandeerd, en de koersen kunnen dalen als een emittent zijn betalingsverplichtingen niet tijdig nakomt of wanneer zijn kredietwaardigheid afneemt.

Buitenlandse effecten zijn gevoelig voor bijkomende risico's, zoals valutaschommelingen, politieke en economische onzekerheid, hogere volatiliteit, lagere liquiditeit en afwijkende financiële en informatiegerelateerde rapporteringsstandaarden. Al die werkingen worden versterkt in groeimarkten.

Hoogrentende obligaties of "rommelobligaties" lopen een groter risico op wanbetaling en prijsvolatiliteit. Hun koers kan onverwacht sterk schommelen.

Dit zijn de standpunten van de auteur op het moment van publicatie en kunnen verschillen van de standpunten van andere personen/teams bij Janus Henderson Investors. Verwijzingen naar individuele effecten vormen geen aanbeveling om effecten, beleggingsstrategieën of marktsectoren te kopen, verkopen of aan te houden en mogen niet als winstgevend worden beschouwd. Janus Henderson Investors, zijn gelieerde adviseur of zijn medewerkers kunnen een positie hebben in de genoemde effecten.

Resultaten uit het verleden geven geen indicatie over toekomstige rendementen. Alle performancegegevens omvatten inkomsten- en kapitaalwinsten of verliezen maar geen doorlopende kosten en andere fondsuitgaven.

De informatie in dit artikel mag niet worden beschouwd als een beleggingsadvies.

Er is geen garantie dat tendensen uit het verleden zich zullen doorzetten of dat prognoses worden gehaald.

Reclame.

8 beknopt artikel

Kernpunten

- Opportunities for incremental risk taking exist in the late-cycle environment as long as one is mindful of valuations and identifies which market segments may benefit from supportive policy.

- Even if the Federal Reserve’s (Fed) rate-cutting trajectory is shallower than anticipated, the global economy is still primed to benefit from less restrictive monetary policy and more stimulus from China.

- In our view, adding risk can be accomplished by broadening equities exposure to include more economically sensitive and leveraged names and by selecting high-yield bonds with attractive income streams and less exposure to rate volatility.

Gerelateerde inzichten

This past year was marked by consequential elections across major democracies and the global economy continuing to adjust to a higher interest rate regime than it had experienced for much of the past 15 years. The ramifications of these developments will be felt well into 2025.

Also extending its influence is a resilient economic cycle. While a robust U.S. economy defied expectations as the Fed battled inflation, economic growth must now balance optimism around rate cuts with downside risks if the anticipated cuts don’t fully materialize. To be determined is the degree to which a change in policy by the incoming U.S. administration could impact domestic and global growth. Another potential tailwind for the global economy is more aggressive stimulus in China.

While many of these developments will be welcomed by investors, the global economy remains late cycle, and any incremental risk taking should be approached with caution. Narrowing the tolerance for error is the surge in riskier assets’ valuations in the wake of the U.S. election. As global monetary policy diverges and economic broadening impacts sectors in varying degrees, investors should seek to balance a security’s ability to benefit from the cycle’s extension with its valuation.

The macro: Diverging cycles

The U.S. economy’s streak of outperforming other advanced countries looks set to continue now that the Fed has begun to lower the cost of capital. This is not, however, the full-throated risk-on environment typically associated with the advent of a new cycle. Employment has proven durable, but the trend – notwithstanding the temporary effects of recent storms – has been downward. Rising consumer delinquencies represent another area of concern.

We remain neutral on Europe, despite signs of steadying consumption. The region’s central banks were earlier than the Fed in lowering rates, but that was due to necessity. China, on the other hand, could break out of an extended stupor now that the central government has initiated more action to address structural issues. Furthermore, the country’s equity valuations do not reflect what we view as an improving earnings backdrop.

Market’s evolving expectations for Fed’s overnight policy rate

While forward-looking markets’ upwardly revised expectations for the federal funds rate can be viewed as a vote of confidence in the extension of the economic cycle, it also means borrowing costs likely won’t dip to previously anticipated levels.

Source: Bloomberg, Janus Henderson Investors, as at 15 November 2024.

Any shift in U.S. economic policy will undoubtedly reverberate through the corporate sector and financial markets. Deregulatory, corporate tax, and other pro-growth aspects of the incoming administration’s agenda would be favorable for riskier assets. However, tariffs, other policy initiatives or staffing decisions may present risks to growth.

Financials and energy have been highlighted as two sectors that could benefit from more relaxed oversight. The outlook for the tech sector is more nuanced as questions loom over the size and scope of industry behemoths and the protections afforded to social media platforms. Multiple sectors could benefit from a more favorable mergers and acquisitions climate.

Roadblocks to the efficient flow of goods and capital tend to be inflationary, and deterioration of the U.S. fiscal position could spur inflation and put upward pressure on longer-dated interest rates. Pro-growth initiatives would pay off if the rate of economic expansion exceeded the cost of capital but that bar would likely be raised should trade and fiscal policy send interest rates higher.

Equities: Balancing tailwinds and valuations

Although an extension of the cycle should be conducive for riskier assets, we believe that for equities, a modest rotation within the asset class is preferable to increasing overall equities exposure at the expense of core fixed income. Rate cuts stand to benefit small-cap companies that tend to carry more debt. Since they are less dependent on borrowing costs, midcaps don’t necessarily need lower rates to enjoy the tailwinds of economic expansion. The extension of the 2018 tax reform would likely support earnings across the corporate sector.

Valuations are elevated, with most equity segments’ price-to-earnings ratios residing in the top quartile of their long-term average. Despite the possibility of broadening economic growth, value stocks are one of the few categories where earnings estimates still have meaningful potential to grow into their valuations. And although broader participation in the equities rally is a welcome development, investors should not lose sight of the Magnificent 7’s continuing ability to beat expectations and justify their persistently high valuations.

Global 12-month earnings growth forecasts

Although U.S. earnings estimates are above long-term averages – as are price-to-earnings multiples in most markets – more modest expectations for ex-U.S. stocks indicate that earnings may have potential to grow into their valuations.

Source: Bloomberg, Janus Henderson Investors, as at 15 November 2024.

An already tenuous situation for European stocks could worsen should deglobalization accelerate. Still, consumption within the region indicates green shoots, and Chinese stimulus could cast a lifeline to Europe’s capital goods and luxury products exporters. In Japan, any consumption-related benefit from an appreciating yen could be tempered by headwinds for its sizeable export sector.

Fixed income: Navigating a higher and tighter environment

The price of fighting inflation was steep for bond investors. But with most of that battle behind us, the new – higher – range of bond yields globally has left the asset class in a better position to deliver steady income, diversification to riskier assets and, in certain jurisdictions, the potential for capital appreciation.

In the U.S., the Treasuries yield curve reset to higher levels and steepened in the wake of November’s election. Should the market’s forecast of notably fewer rate cuts prove correct, shorter-date bonds will have lost a promising tailwind. In only a few weeks, the anticipated terminal rate for this cycle has reset to a materially higher range of 3.5% to 4.0%. Although having already sold off, longer-dated bond yields could face additional pressure if economic growth further surprises to the upside or trade policies and robust wages prove inflationary.

Corporate credits are richly valued, with the difference between their yields and those of their risk-free benchmarks the tightest since 1997. A candidate for incremental allocation in this space would likely be higher-quality, high-yield issuers, as this category provides more carry, a larger yield cushion, and stands to benefit from lower borrowing costs. Corporate defaults trending lower indicates that issuers have withstood the most intense period of restrictive financial conditions. At current spreads, the interest rate sensitivity of investment-grade credits in a still-volatile Treasuries market cannot be ignored. Securitized credits, by contrast, appear more fairly valued and stand to benefit from rising values of their underlying assets.

U.S. and European corporate spreads

Fed rate cuts and a resilient corporate sector have left bond valuations elevated, but within the space, high-yield issuance has the potential to provide additional carry and less sensitivity to moves in a still-volatile rates market.

Source: Bloomberg, Janus Henderson Investors, as at 15 November 2024.

Outside the U.S., diverging economic fortunes and monetary policy create opportunities. Europe, for example, likely has little choice but to continue its accommodative course. Higher U.S. rates and the accompanying dollar strength, however, would present a challenge for emerging market issuers dependent upon financing in the U.S. currency.

Carry is het extra rendement dat een belegging met een hoger rendement heeft opgeleverd ten opzichte van een andere belegging.

Kredietspread is het renteverschil tussen effecten met dezelfde looptijd maar van verschillende kredietkwaliteit. Verruimende spreads betekenen over het algemeen dat de kredietwaardigheid van zakelijke kredietnemers verslechtert, verkrapping betekent dat deze verbetert.

Diversificatie garandeert geen winst. Ook neemt diversificatie het risico op beleggingsverliezen niet weg.

Excess Return indicates the extent to which an investment out- or underperformed an index.

Monetair beleid verwijst naar het beleid van een centrale bank dat erop gericht is de inflatie en de groei van een economie te beïnvloeden. Dat houdt onder meer in dat de rentevoeten en de geldtoevoer onder controle worden gehouden.

De koers-winstverhouding (K/W) meet de aandelenkoers in verhouding tot de winst per aandeel voor een of meer aandelen in een portefeuille.

Volatiliteit is een maatstaf voor het risico op basis van de spreiding van de rendementen voor een bepaalde belegging.

Een rentecurve geeft de rendementen (rente) weer van obligaties met dezelfde kredietkwaliteit, maar met verschillende vervaldata. Obligaties met langere looptijden hebben meestal hogere rendementen.

Belangrijke informatie

Energiebedrijven kunnen heel gevoelig zijn voor schommelingen in de energieprijzen en in de vraag naar en het aanbod van brandstoffen, natuurbehoud, het succes van exploratieprojecten en fiscale en andere reglementering.

Aandelen brengen risico's met zich mee, waaronder marktrisico's. Rendementen fluctueren als reactie op ontwikkelingen bij de emittent en in de politieke en economische situatie.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Vastrentende effecten zijn onderhevig aan het rente-, inflatie-, krediet- en wanbetalingsrisico. De obligatiemarkt is volatiel. Als de rentes stijgen, dalen de obligatiekoersen meestal en vice versa. Terugbetaling van de hoofdsom is niet gegarandeerd, en de koersen kunnen dalen als een emittent zijn betalingsverplichtingen niet tijdig nakomt of wanneer zijn kredietwaardigheid afneemt.

Buitenlandse effecten zijn gevoelig voor bijkomende risico's, zoals valutaschommelingen, politieke en economische onzekerheid, hogere volatiliteit, lagere liquiditeit en afwijkende financiële en informatiegerelateerde rapporteringsstandaarden. Al die werkingen worden versterkt in groeimarkten.

Hoogrentende obligaties of "rommelobligaties" lopen een groter risico op wanbetaling en prijsvolatiliteit. Hun koers kan onverwacht sterk schommelen.