Kernpunten

- Small-cap aandelen stegen na de verkiezingen door optimisme over het beleid van de nieuwe Amerikaanse regering, vergelijkbaar met wat er gebeurde tijdens de eerste termijn van Trump in 2016. De performance werd in beide perioden breed gedragen, waar zelfs bedrijven van mindere kwaliteit van profiteerden.

- De markt gaat nu over van aanvankelijke euforie naar een periode van evaluatie, waarin de effecten van nieuw beleid duidelijker worden en we meer spreiding in de bedrijfsprestaties zullen gaan zien naarmate de markt winnaars en verliezers identificeert.

- Tegen deze achtergrond is het van cruciaal belang om te beoordelen in hoeverre bedrijven in staat zijn om met beleidsveranderingen om te gaan in een nieuwe economische realiteit. Naar onze mening moeten beleggers zich richten op small-caps van hoge kwaliteit met sterke balansen en robuuste winsten, maar moeten ook de small-caps met prudente waarderingen en blootstelling aan de binnenlandse Amerikaanse economie.

De verkiezing van Donald Trump in 2016 zorgde voor een golf van optimisme over Amerikaanse small-caps. Beleggers anticipeerden op lagere vennootschapsbelastingen, deregulering en een focus op binnenlandse economische groei. Na de verkiezingen van 2024 en de eerste maanden van 2025, zijn de parallellen tussen de eerste en tweede regering-Trump opvallend.

Na de bekendmaking van de verkiezingsuitslag stegen de small-caps opnieuw, aangejaagd door vergelijkbare beleidsverwachtingen. Nu de aanvankelijke euforie is weggeëbt, vragen veel beleggers zich af: wat is de volgende stap en hoe kunnen we ons positioneren in het evoluerende landschap van small-caps?

De drie fasen van Trump

De reactie van de markt op de overwinning van Trump is in grote mate vergelijkbaar met wat er tijdens zijn eerste termijn gebeurde. We herkennen daarbij drie fasen:

Aanvankelijke euforie: ongeveer 4-6 weken na de verkiezingen

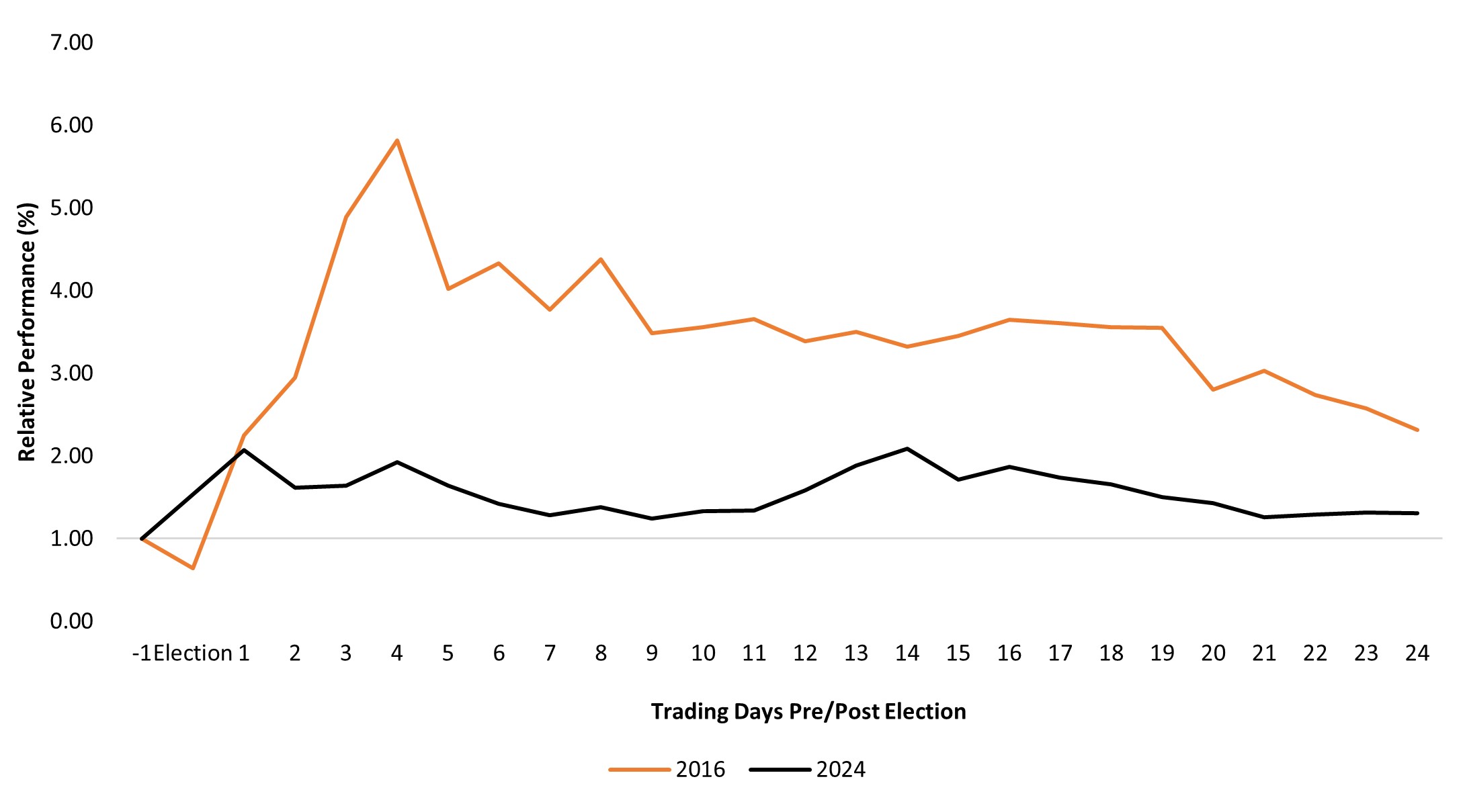

Zowel in 2016 als in 2024 zorgden de overwinningen van Trump voor enthousiasme over kleinere Amerikaanse bedrijven. Beleggers stortten zich op de small-cap indices, waardoor eigenlijk iedereen meeliftte op een breed gedragen rally - zelfs bedrijven van mindere kwaliteit.

Tijdens deze fase richtten de markten zich op de potentiële positieve effecten van deglobalisering, belastingverlagingen en deregulering. Er werd ook verwacht dat invoerheffingen Amerikaanse bedrijven konden helpen om het gat met overzeese concurrenten te dichten, omdat zij hierdoor minder kostenconcurrerend worden. Deze periode werd meer bepaald door perceptie en sentiment dan door fundamentele analyse.

Afbeelding 1: Positieve eerste reactie van small-caps op overwinningen van Trump in 2016 en 2024

Relatieve prestaties, Russell 2000 Index, S&P 500® Index

Bron: Bloomberg. Rendementen van de Russell 2000 Index en de S&P 500 Index van 7 november 2016 tot 13 december 2016 en van 4 november 2024 tot 10 december 2024.

Beleidsevaluatie: de periode van 12 maanden na de eerste fase

In de tweede fase, ruwweg het kalenderjaar na de verkiezingen, beginnen de markten een onderscheid te maken tussen winnaars en verliezers naarmate beleidsvoorstellen uitkristalliseren. In deze periode wegen beleggers de impact af van invoerheffingen, belastingverlagingen, immigratiehervormingen en deregulering. Dit is waar actief beheer doorgaans waarde toevoegt: het onderscheidt de bedrijven die hiervan zullen profiteren van de bedrijven van mindere kwaliteit, die aanvankelijk meeliftten op het sentiment.

In 2017 bleek tijdens deze periode dat er prestatieverschillen bestonden tussen bedrijven van hoge en lage kwaliteit. Anno 2025 zullen beleggers moeten beoordelen hoe specifiek beleid de inflatie, het monetaire beleid en individuele sectoren en bedrijven zal beïnvloeden.

Economische realiteit: na 13 maanden

In de derde fase worden de werkelijke economische gevolgen duidelijk. In 2018 ondervonden small-caps tegenwind van de stijgende rente en zorgen over de inflatie. Bedrijven met voorzichtige waarderingen en sterke fundamentals doorstonden deze storm echter beter dan hun overgewaardeerde sectorgenoten.

De inflatie is nog steeds aanzienlijk, en de Federal Reserve heeft aangegeven dat de beleidsrente mogelijk langer hoger zal blijven. Dit kan gunstig zijn voor small-caps met een hoog rendement op geïnvesteerd vermogen (ROIC) en een hoge winstgevendheid, omdat zij beter gepositioneerd zijn om door hogere kapitaalkosten te navigeren. Omgekeerd kunnen onrendabele bedrijven met kasstromen ver in de toekomst het moeilijk krijgen.

Marktomstandigheden vergelijken

De politieke context in 2025 weerspiegelt die van 2017, met een focus op invoerheffingen, belastingverlagingen en deregulering. Met name de heffingen zijn een belangrijk raakvlak. In beide regeringen heeft Trump deze gebruikt als instrument om beleidsprioriteiten te realiseren, wat zowel uitdagingen als kansen creëert voor small-caps.

Een andere gelijkenis is de focus op binnenlandse economische groei. Small-cap aandelen, die meer blootstelling hebben aan de Amerikaanse economie dan hun grotere tegenhangers, kunnen profiteren van beleid dat binnenlandse producenten begunstigt. Lagere vennootschapsbelastingen en een soepeler regelgevingsklimaat kunnen de prestaties van small-caps verder stimuleren, zoals we in 2017 en 2018 hebben gezien. Een versoepeling van het regelgevend toezicht zou kunnen leiden tot meer fusies en overnames, waarbij large-caps goed gepositioneerde small-caps opkopen.

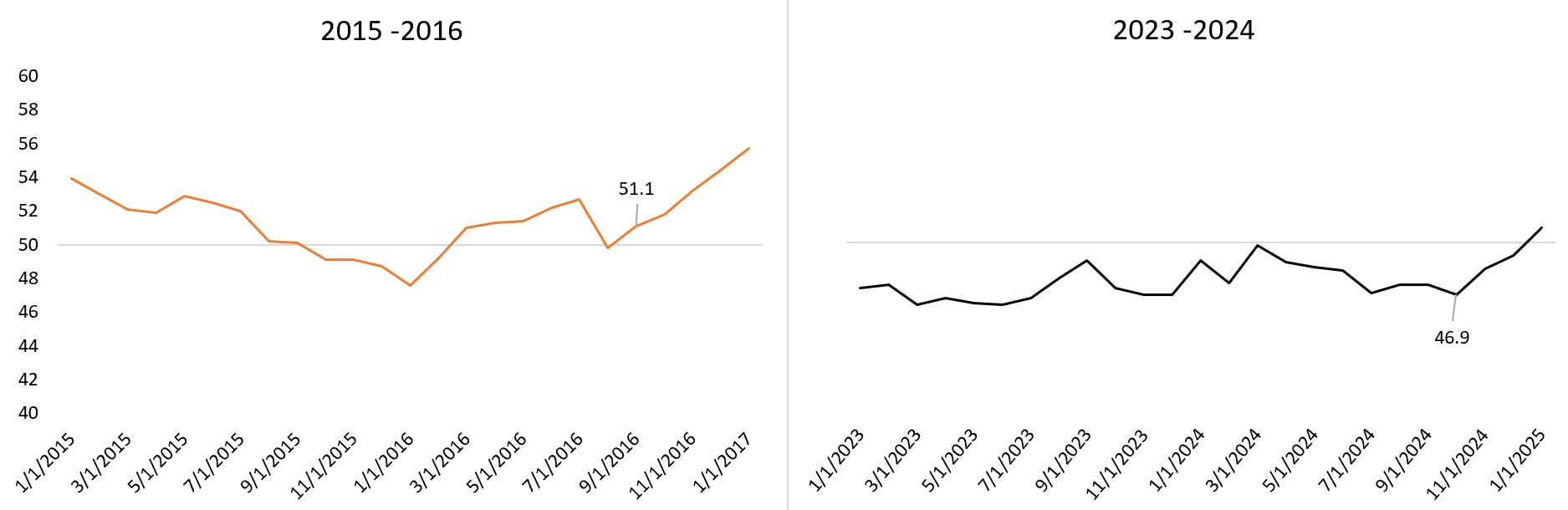

In beide perioden was er sprake van een vertraging van de industriële productie, zij het in verschillende mate. De ISM Manufacturing Index laat zien dat de VS zich sinds november 2022 in een periode van industriële krimp bevindt, vergelijkbaar met de zwakte van 2016 (zie Afbeelding 2). Er is optimisme dat een bedrijfsvriendelijk beleid de aanzet kan geven tot een opleving zoals we de vorige keer zagen.

Er zijn echter belangrijke verschillen. Hoge rentetarieven in 2025 kunnen de 'animal spirits' in bedwang houden die de rally in small-caps aanjoegen tijdens de eerste termijn van Trump. Daarnaast is de markt nog meer dan in 2016 gericht op de weerbaarheid van toeleveringsketens en inflatierisico's.

Afbeelding 2: ISM Manufacturing Index: overgang van krimp naar groei

Bron: Bloomberg. ISM Manufacturing Index.

Welke lessen hebben we geleerd?

De ervaring van 2016 benadrukt hoe belangrijk het is om te focussen op bedrijven met gezonde waarderingen en sterke fundamentals. De waarderingspieken van de Russell 2000 na de verkiezingen in beide periodes waren kortetermijnverstoringen die uiteindelijk normaliseerden. Nu we langzaamaan overgaan van beleidsspeculatie naar beleidsimplementatie, denken we dat bedrijven met sterke balansen, een hoge ROIC en blootstelling aan de binnenlandse markt als winnaars uit de bus zullen komen.

Een andere les is de waarde van geduld. Een andere les is de waarde van geduld. Hoewel de eerste rally's opwindend kunnen zijn, worden de echte kansen vaak pas later zichtbaar, wanneer de markten stabiliseren. De geschiedenis leert dat wanneer het enthousiasme afneemt, bedrijven met concurrentievoordelen het best gepositioneerd zijn voor veranderende omstandigheden. Door de nadruk te leggen op fundamentele factoren en overgewaardeerde aandelen te vermijden, denken we dat beleggers in een betere positie zullen verkeren om te profiteren van beleidsverschuivingen.

Rendement op geïnvesteerd vermogen (ROIC) is een maatstaf voor hoe effectief een bedrijf het geld heeft gebruikt dat in de operationele activiteiten is geïnvesteerd.

Monetair beleid verwijst naar het beleid van een centrale bank dat erop gericht is de inflatie en de groei van een economie te beïnvloeden. Dat houdt onder meer in dat de rentevoeten en de geldtoevoer onder controle worden gehouden.

Aandelen van ondernemingen met een kleinere beurskapitalisatie kunnen minder stabiel zijn en kwetsbaarder blijken bij ongunstige ontwikkelingen. Ze kunnen ook volatieler en minder liquide zijn dan aandelen van ondernemingen met een grotere beurswaarde.

Dit zijn de standpunten van de auteur op het moment van publicatie en kunnen verschillen van de standpunten van andere personen/teams bij Janus Henderson Investors. Verwijzingen naar individuele effecten vormen geen aanbeveling om effecten, beleggingsstrategieën of marktsectoren te kopen, verkopen of aan te houden en mogen niet als winstgevend worden beschouwd. Janus Henderson Investors, zijn gelieerde adviseur of zijn medewerkers kunnen een positie hebben in de genoemde effecten.

Resultaten uit het verleden geven geen indicatie over toekomstige rendementen. Alle performancegegevens omvatten inkomsten- en kapitaalwinsten of verliezen maar geen doorlopende kosten en andere fondsuitgaven.

De informatie in dit artikel mag niet worden beschouwd als een beleggingsadvies.

Er is geen garantie dat tendensen uit het verleden zich zullen doorzetten of dat prognoses worden gehaald.

Reclame.

Belangrijke informatie

Lees de volgende belangrijke informatie over fondsen die vermeld worden in dit artikel.

- Aandelen/deelnemingsrechten kunnen snel in waarde dalen en gaan doorgaans gepaard met hogere risico's dan obligaties of geldmarktinstrumenten. Als gevolg daarvan kan de waarde van uw belegging dalen.

- Aandelen van kleine en middelgrote bedrijven kunnen volatieler zijn dan aandelen van grotere bedrijven en kunnen soms moeilijk te waarderen of te verkopen zijn op het gewenste moment en tegen de gewenste prijs, wat het risico op verlies vergroot.

- Het Fonds kan gebruikmaken van derivaten om het risico te verminderen of om de portefeuille efficiënter te beheren. Dit gaat echter gepaard met andere risico's, waaronder met name het risico dat een tegenpartij bij derivaten niet in staat is om haar contractuele verplichtingen na te komen.

- Als het Fonds activa houdt in andere valuta's dan de basisvaluta van het Fonds of als u belegt in een aandelenklasse/klasse van deelnemingsrechten in een andere valuta dan die van het Fonds (tenzij afgedekt of 'hedged'), kan de waarde van uw belegging worden beïnvloed door veranderingen in de wisselkoersen.

- Effecten in het Fonds kunnen moeilijk te waarderen of te verkopen zijn op het gewenste moment of tegen de gewenste prijs, vooral in extreme marktomstandigheden waarin de prijzen van activa kunnen dalen, wat het risico op beleggingsverliezen verhoogt.

- Het Fonds kan geld verliezen als een tegenpartij met wie het Fonds handelt niet bereid of in staat is om aan zijn verplichtingen te voldoen, of als gevolg van een fout in of vertraging van operationele processen of verzuim van een derde partij.