Key takeaways:

- A resurgence in transaction volumes is indicating a turnaround for asset valuations, setting the stage for a rebound in listed real estate.

- Listed REITs are well-positioned to use improved liquidity and better financing terms and access to acquire assets and engage in development projects.

- REITs are again showing their potential for earnings growth and long-term capital appreciation.

Listed REIT prices declined sharply two years ago, as the market anticipated and priced in the forthcoming drop in property prices, moving lower ahead of the broader commercial real estate market. However, following a prolonged period of weakness for listed real estate, we are now seeing a beacon of optimism for the asset class. A recent resurgence in transaction volumes suggests that the bulk of the private market has now absorbed necessary write-downs, instilling confidence that private market values are stabilizing. Consequently, we believe the stage is set for real estate investment trust (REIT) investors to look forward with a renewed sense of optimism and potentially benefit from the pricing in of potential growth in earnings and assets values.

Early signs of a recovery

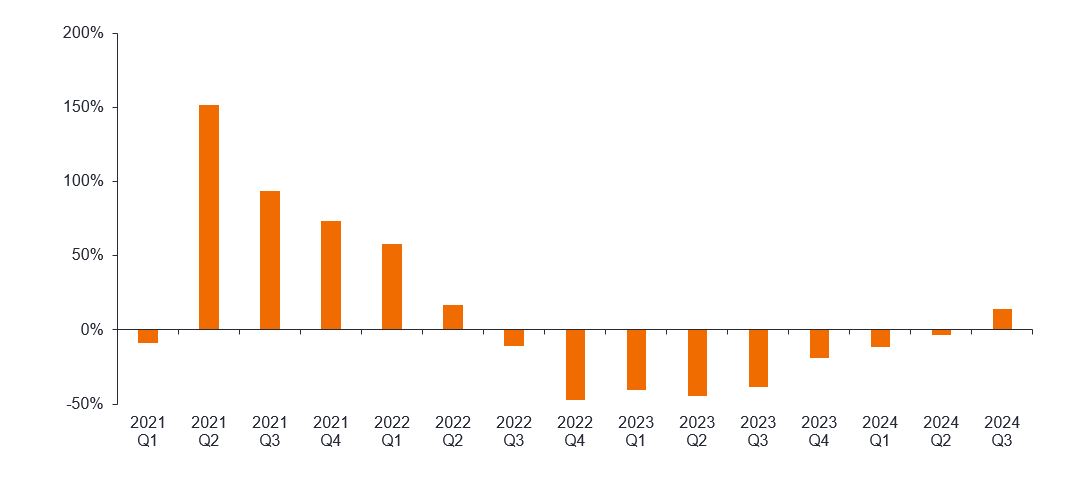

In the third quarter of 2024, for the first time in over two years, US real estate transaction volumes look to have increased as reported by CBRE, the world’s largest property brokerage ─ a bellwether for the corporate real estate sector. This is very welcome news for property investors following a painful period of higher borrowing costs, economic uncertainty, and declining asset values. All told, these factors contributed to transaction levels that collapsed nearly 70% from peak levels in 2021.1 With large gaps between buyer and seller pricing expectations, liquidity was not available at private real estate’s reported valuations. Non-traded (private) REITs’ gated investor funds, queues of unmet redemption requests in core property funds formed, and eventually losses for investors and lenders slowly crystalized through the private markets’ gradual adjustments to reported values. With reported real estate prices now starting to reflect their underlying asset values, supported by central banks beginning to lower interest rates, investor optimism has grown alongside improving real estate debt markets, fostering a recovery in real estate transactions.

CBRE advisory sales (year-on-year % change)

Source: CBRE, as at end 3Q 2024. Past performance does not predict future returns.

CBRE also reported a 20% revenue increase from US investment sales (also known as advisory sales – ie. buy/sell transactions) in the third quarter. According to its CEO, “Capital markets transaction activity has passed an inflection point and is in early stages of recovery.” Management further noted, “We think buyers and sellers have largely come together for most asset classes or are very close to having come together…there is debt available now…there’s increased interest in multi-family. We’ve seen a little bit of cap rate (rate of return) compression in multi-family and industrial.”

CBRE’s commercial mortgage originations advanced over 50% over the same quarter, signaling burgeoning strength in real estate lending as well. We see conditions as being ripe for increased lending as the transaction market recovers and evidence of stronger asset pricing surfaces and becomes better appreciated by the market.2

Mounting evidence for a revival

Elsewhere, there are notable recent transactions illustrating healthy asset pricing and attractive lending, supporting our team’s view that real estate pricing has bottomed and a new cycle is beginning:

- KKR/Lennar: In June this year (2024), private equity company KKR acquired 5,200 apartment units from home construction company Lennar’s multifamily division for US$2.1bn, representing an estimated 15-20% premium to asset value for the listed residential REITs. 3

- Brookfield/DRA: In May, investment firm Brookfield acquired a 14.6m square foot portfolio of industrial warehouses from real estate investment adviser DRA for US$1.3bn. The deal encompasses 128 properties across 20 markets and is 98% leased. 4

- Tishman Speyer/Rockefeller Center: In October, diversified real estate firm Tishman Speyer completed a US$3.5bn refinancing of NYC’s Rockefeller Center in the CMBS market for a 6.5% interest rate. For much of the past two years, office transactions remained dormant and plagued by distressed lending conditions. This refinancing marks the largest single-asset office debt deal in history and was significantly oversubscribed by debt investors. 5

What does the transactions recovery mean for REITs?

Within real estate, REITs are enviably positioned, with 30% loan-to-value ratios (compared to 60% for private real estate), have cheaper cost of funds, and can issue equity in public markets to grow, thereby taking advantage of the resurgent liquidity to buy assets. However, for the past two years, REITs have been stymied in their acquisition pursuits by lack of deal-flow and wide bid-ask spreads. As transactions pick up and pricing improves, REITs across sub-sectors are increasingly deploying capital for acquisitions or development projects, which we believe will advance earnings growth. Furthermore, many REITs have joint ventures or fund management platforms capable of delivering additional returns when assets are sold. These profits have largely diminished over the prior two-year standstill in the transaction market; but as deal volumes recover, REITs are likely to once again be positioned to harvest gains from these vehicles, bolstering profits.

The recovery in transactions, therefore, highlights multiple avenues for REITs to boost earnings growth, strengthening the outlook for asset values, and ultimately, the potential for higher share prices and growing dividends in a new cycle.

1 Green Street Advisors, annual transactions in 2023 versus the 2021 peak.

2 CBRE 3Q 2024 earnings call, 24 October 2024.

3 CoStar.com; KKR Makes $2.1 Billion Bet on Multifamily in Buying Apartments From Lennar’s Quarterra, 26 June 2024.

4 Connectcre.com; Brookfield Closes on $1.3B Light Industrial Portfolio, 19 July 2024.

5 PRNewswire.com; Tishman Speyer Completes $3.5 Billion Refinancing for Rockefeller Center, 21 October 2024.

6 Green Street Advisors, Morgan Stanley, Janus Henderson Investors Analysis, as of December 31, 2022.

Bid-ask spread: the difference between the bid price and the ask price for a particular security.

Capital markets: financial markets that bring buyers and sellers together to trade stocks, bonds, currencies, real estate, and other financial assets.

Cap rate compression: occurs when the capitalization rate (rate of return) on a real estate investment property based on the income that the property is expected to generate decreases.

CMBS: Commercial Mortgage-Backed Securities are fixed rate bonds that represent an investment in a portfolio of mortgages on a range of commercial properties.

Gated fund: a fund with restrictions placed on redemptions/withdrawals, usually when the assets of a fund are illiquid and difficult to turn into cash for redemption in a timely manner.

Liquidity: a measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as ‘liquid’.

IMPORTANT INFORMATION

REITs or Real Estate Investment Trusts: invest in real estate, through direct ownership of property assets, property shares or mortgages. As they are listed on a stock exchange, REITs are usually highly liquid and trade like shares.

Real estate securities, including Real Estate Investment Trusts (REITs), are sensitive to changes in real estate values and rental income, property taxes, interest rates, tax and regulatory requirements, supply and demand, and the management skill and creditworthiness of the company. Additionally, REITs could fail to qualify for certain tax-benefits or registration exemptions which could produce adverse economic consequences.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.