Key takeaways:

- Inflation among developed markets had tended to be synchronous since the initial COVID shock but something odd has emerged in the UK during 2023, which has caused UK inflation to be stubbornly higher and similarly gilt yields.

- Explanations for the inflation conundrum range from benign/temporary reasons through to potentially more persistent inflation.

- For international investors, there are potentially easier markets in which to invest, where the inflation outlook offers an earlier return to normality and the potential for rate cuts.

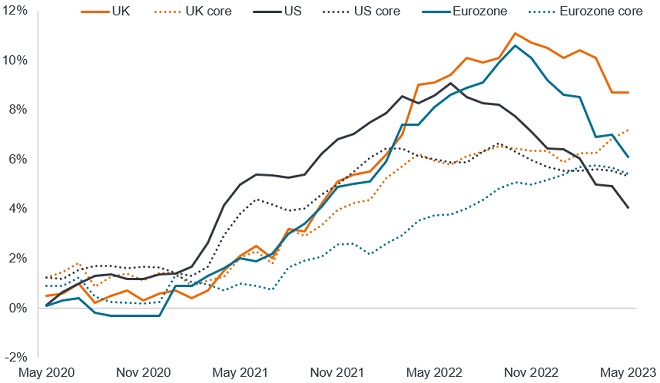

The experience of inflation among developed markets tended to be synchronous since the initial COVID shock but something odd has emerged in the UK during 2023.

Nearly all developed markets experienced a period of low inflation following the 2007-9 Global Financial Crisis (GFC). This came to a rude halt as a combination of monetary and fiscal stimulus to counter the economic effects of COVID lockdowns melded with the supply shocks caused by the war in Ukraine in 2022. Inflation rates of 9-11% – levels not seen since the 1980s – made headlines. While inflation peaked and has come down rapidly in recent months across both emerging and developed markets, in the UK it has proved much more stubborn. Specifically, core inflation has continued to rise in recent months causing a profound crisis of confidence in UK monetary policy.

A regime shift

In the decades before the GFC, UK gilts had typically yielded more than US government bonds and German government bonds. Post the Brexit vote, gilt yields tended to be lower, sitting midway between US government bond yields and German government bond yields. In 2023, they have decisively broken out of this regime and returned to being the highest yielding of the three countries.

Various factors might explain this. Among them are the UK’s large fiscal deficit and its composition (the UK government needs to issue a lot of gilts and has a relatively high number of index-linked gilts that have to pay out more when inflation is higher). Faded appetite from buyers for gilts after recent political upheavals has also not helped. But most important in 2023 is the inflation outlook. The conundrum is why should core inflation have continued to rise at alarming rates in the UK?

Fig 1: Inflation rates across the UK, the US and the Eurozone

Source: Refinitiv Datastream, Consumer Price Index, year-on-year % change, headline inflation in bold lines, core in dotted lines, 31 May 2020 to 31 May 2023. Core inflation excludes energy and food in the US and additionally alcohol and tobacco in the UK and the Eurozone.

Core inflation (which excludes the volatile items of food and energy) typically lags headline inflation. In the US, it is likely to come down further as we know what wholesale used car prices and market rents are doing and these feed into official inflation statistics with a lag. In the UK bizarrely, it is not just services but core goods prices have started reaccelerating and core inflation is still ticking up as a result.

There are a number of ways to try and explain the UK inflation conundrum ranging from benign/ temporary explanations to one of a much more problematic persistent inflation problem.

Be patient

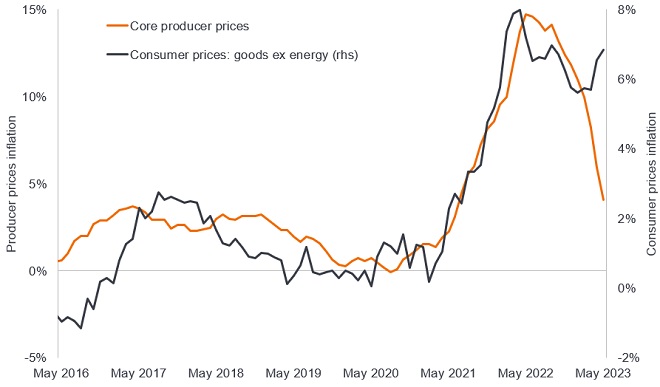

The first is it may be down to time lags and measurement quirks so no need to panic. If we look at producer price indices, these are coming down swiftly and are likely to follow through into consumer prices (although recent profit margin expansion and pass through of exchange rate costs disrupted the downward trajectory). The energy price cap drops are likely to feed into drops in the July data when it is released in August. Monthly core inflation prints are subject to huge overshoots/undershoots in either direction and it will take time to assess the true trend.

Fig 2: Core consumer goods inflation curiously ticked up as producer prices moderate

Source: Refinitiv Datastream, UK Producer Price Index: output prices ex food, beverages, tobacco and petroleum; UK Consumer Price Index: non-energy goods, year-on-year % change, 31 May 2016 to 31 May 2023.

UK inflation has been brought forward

The second is the notion that inflation was sucked into the first half of this year. Firms that set prices in response to events are referred to as “state dependent” whilst those that change prices at regular fixed intervals e.g. annually are described as “time dependent”. The Bank of England’s Decision Maker Panel (DMP) Survey of firms noted that state dependent price setting firms have been raising prices more than time dependent firms. Companies may have pushed through prices while they could in the expectation inflation would be softer later in the year. Encouragingly, when asked about price rises for next year, state dependent firms (which make up about 60% of firms) predicted lower inflation than time dependent price setters.

A persistent inflation problem

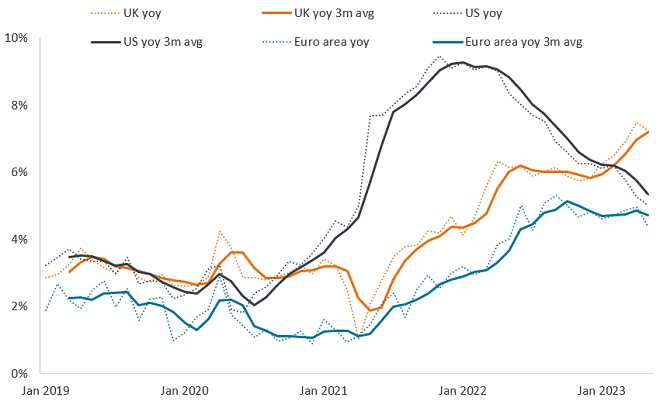

The third is that the UK has become unhinged from the US and Europe and has more persistent inflation. Reasons might be due to greater trade friction post Brexit leading to higher costs and a peculiarly tight labour market. While wages in the US and Europe are moderating, this is not yet evident in the UK.

Fig 3: Wage growth in UK is still accelerating while moderating elsewhere

Source: Indeed Wage Tracker, January 2019 to May 2023. Yoy = year-on-year % change. The euro area series is an employment-weighted average of France, Germany, Ireland, Italy, Netherlands, and Spain. The 3-month average compares a 3-month period with the same 3-month period a year ago to smooth out distortions in an individual month.

Such profound uncertainty sourced from a lack of true understanding about what is driving UK inflation has caused a crisis of confidence on the interest rate outlook. UK peak rate expectations surged higher in early July on little/no meaningful economic data, reaching over 6.5%.1 A sudden concern that interest rates may be having little impact on the UK economy created this airpocket in rate expectations. This argument ignores lags inherent in monetary policy but reveals the crisis of confidence surrounding UK monetary policy at present. Last October, the crisis of confidence was of course about fiscal policy.

Overseas preference

Given the uncertainty surrounding the drivers of UK core inflation for most international investors there are much easier bond markets in which to invest. This includes economies where the inflation story is showing the potential for a return to normality, albeit for core inflation this will still take some time as it typically lags. In emerging markets there are already nascent debates about the first rate cuts, while for most central banks in the developed world the debate is about the last rate hike or two in this cycle. Sitting in the UK, the global covid inflation shock can look very different to other economies e.g. China where CPI inflation has hit 0% in June 2023 or the US down to 3% (from 9.1% a year ago).2

1Source: Bloomberg, interest rate projections, correct at 6 July 2023.

2Source: Refinitiv Datastream, China CPI inflation, US CPI inflation for June 2023, as at 12 July 2023.

Gilts: Government bonds issued by the UK government to finance UK national debt. Index-linked gilts have coupon (interest payments) and final maturity value (amount repaid on the date the bond matures) that are adjusted in line with the inflation rate.

Inflation: The rate at which the prices of goods and services are rising in an economy. Headline inflation refers to inflation across all goods and services, whereas core inflation excludes components that exhibit large amounts of volatility from month to month such as fuel and food prices.

Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Il Fondo investe in obbligazioni ad alto rendimento (non investment grade) che, sebbene offrano di norma un interesse superiore a quelle investment grade, sono più speculative e più sensibili a variazioni sfavorevoli delle condizioni di mercato.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Le spese correnti possono essere prelevate, in tutto o in parte, dal capitale, il che potrebbe erodere il capitale o ridurne il potenziale di crescita.

- I CoCo (Obbligazioni contingent convertible) possono subire brusche riduzioni di valore in caso d’indebolimento della solidità finanziaria di un emittente e qualora un evento trigger prefissato comporti la conversione delle obbligazioni in azioni dell’emittente o il loro storno parziale o totale.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo eterogeneo sulle diverse obbligazioni. Nello specifico, di norma i prezzi delle obbligazioni si riducono all’aumentare dei tassi d’interesse. Ciò accade soprattutto alle obbligazioni maggiormente sensibili alle variazioni dei tassi d’interesse. Poiché una quota significativa del fondo potrebbe essere investita in tali obbligazioni (o in derivati obbligazionari), un rialzo dei tassi d’interesse potrebbe incidere negativamente sui rendimenti del fondo.