Investment Environment

As central banks continued to combat inflation, investors focused on the risk of a recession and earnings contraction into 2023. The FTSE All Share Index dropped by 3.5% in sterling terms, as inflation and interest rate rises heightened worries about a deep recession, undoing July’s strong performance.¹In September, a government tax cut proposal unnerved investors because it threatened the country’s fiscal position. This pushed sterling to a record low against the US dollar and prompted the Bank of England (BoE) to announce an emergency plan to halt turmoil in the UK bond market.

In the same month, the BoE raised interest rates by 50 basis points (bps) to 2.25% –the seventh consecutive increase –and warned of a looming downturn. Gross domestic product (GDP) expanded by 0.2% over the second quarter, following 0.7% growth over the previous quarter, while the annual inflation rate unexpectedly dipped to 9.9% in August from July’s 40-year high of 10.1%. However, retail sales fell in August from their July levels and consumer confidence sank to a record low in September -underlining the fragile state of the economy.¹

Sterling weakened against the US dollar during the quarter, dragged down by the gloomy economic outlook and investor anxiety about the government’s fiscal policies. Smaller companies underperformed their larger counterparts with the Numis Smaller Companies ex-Investment Companies Index down 6.4% against a fall in the FTSE All-Share Index of 3.5%.¹

Portfolio Review

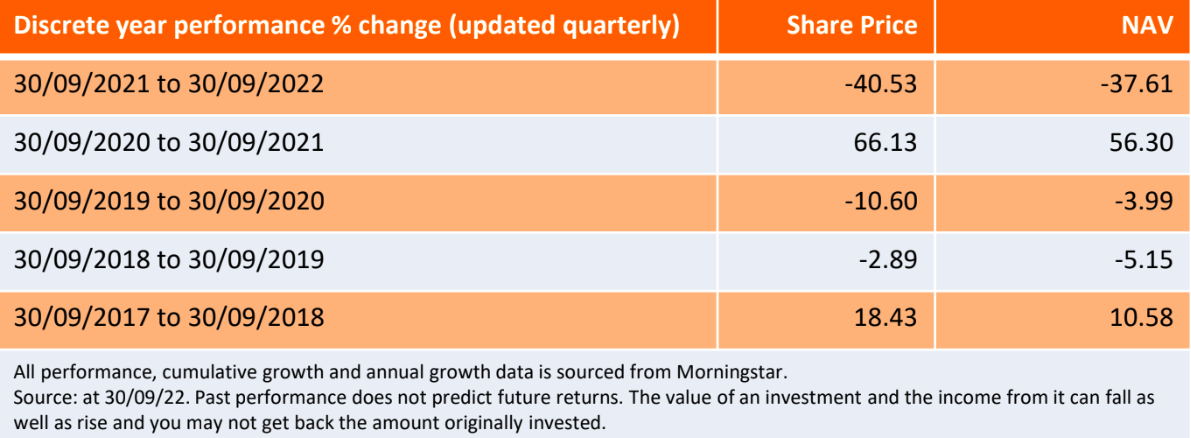

The Company fell 12.0% over the quarter compared to the Numis Smaller Companies ex-Investment Companies Index, which returned -6.3%.¹

The biggest contributors to performance included Serica, RPS and Balfour Beatty. Serica, a North Sea oil and gas company, rose as gas prices spiked. Consulting engineer RPS rose after the company announced it had received an agreed takeover approach from a WSP, a Canadian rival. Balfour Beatty, an international infrastructure investor and construction group, rose as the company delivered strong results and investors were comforted by the underpinning of the company’s strong balance sheet.

The biggest detractors from performance included Synthomer, Future and Alliance Pharma. Synthomer, the diversified chemicals group, fell as the company warned of a decline in demand for nitrile gloves and that general weakness in European coatings demand would impact its profits. Future, a specialist media group, fell during the period due to a rotation away from quality growth stocks and towards value stocks. Additionally, the potential departure of the company’s highly regarded CEO in 2023 clouded investor sentiment. Alliance Pharma, a pharmaceutical products business, fell as the company highlighted that achieving its anticipated full-year results would require a number of large orders towards the end of the year.

In terms of activity, we initiated a position in Trainline, the online ticket retailer. We felt that the company was well placed to carve out a dominant position in its market across the UK and Europe. We added to our positions in Ascential, the B2B information and events organiser, and Sigmaroc, the European aggregates business, as recent declines in their share prices left the companies looking attractively valued from our perspective.

We sold the position in Euromoney, the B2B information provider, and Ultra Electronics, the defence products business after they both received agreed bids from private equity. We sold Gooch & Housego, the optical components business, as we were concerned that the business would struggle to deliver its profitability targets due to cost pressures and slow delivery of the order book. We also sold James Fisher, the diversified oil and marine services business. Its debt seemed too high to us, while the company has been struggling with its complicated diversified structure and some aspects of its business have been in structural decline.

Manager outlook

Just as the impact of the COVID-19 pandemic on the global economy was starting to abate, the world was plunged into a new crisis. The conflict between Russia and Ukraine has dramatically shifted the balance of global geopolitics. This has led to a significant jump in oil and other commodity prices, sanctions on the Russian economy, and a humanitarian crisis in Ukraine. The longer-term implications are probably as material, with the isolation of Russia as a pariah state, a stronger more unified Europe and NATO, materiallyhigher defence spending, and an urgent need to reduce European dependence on Russian oil and gas supplies. This has exacerbated inflation, added to the burden on government spending, dampened animal spirits and hurt economic growth.

With inflation prints continuing to remain elevated against both official targets and market forecasts, central banks, led bythe US Federal Reserve (Fed), have become increasingly hawkish. The market now seems to be forecasting further significant rises in interest rates globally and a move from quantitative easing to tightening. Oscillating confidence levels in central banker’s willingness and ability to strike the right balance between containing inflation and supporting economic growth is driving heightened levels of uncertainty and volatility in global equity markets.

The rapid rise of inflation, particularly driven by energy prices, but also by a wider number of other components, is puttingpressure on consumers. Although the labour market is strong and wages are rising, real net disposable income is falling, and consumer confidence is low. Higher energy prices particularly impact lower income households and this has prompted the UK government to bring in measures to help this socioeconomic group. Sectors exposed to consumer spending are likely to face tougher trading as we movethrough 2022 and into 2023.

In the corporate sector, conditions are intrinsically stronger than they were during the Global Financial Crisis of 2008-2009. In particular, balance sheets are more robust. Dividends have been recovering strongly and we are seeing an increasing number ofcompanies buying back their own stock.

We saw a noticeable pickup in corporate activity last year. However, after an active 2021, the initial public offering (IPO) market has become considerably quieter as equity market confidence has diminished. Merger and acquisition (M&A) activity has remained robust as private equity in particular looks to exploit opportunities thrown up by the COVID-19 pandemic and the recent equity market pullback. We expect this to continue in the coming months as UK equity market valuations remain markedly depressed versus other developed markets.

In terms of valuations, the equity market is now trading below long-term averages. Though corporate earnings were sharply down in 2020, we saw a sharp recovery in 2020. We think is likely to continue into 2022 although a weakening economic environment is likely to dampen expectations.

Although uncertainty remains around short-term economic conditions, we think that the portfolio is well positioned to deal with these uncertainties. The movements in equity markets have thrown up some fantastic buying opportunities. However, it is important to be selective as the strength of franchise, market positioning and balance sheet will likely determine the winners from the losers.

¹Source: Bloomberg as at 30 September

Defensive stocks – A defensive stock is a stock that provides consistent dividends and stable earnings regardless of the state of the overall stock market. There is a constant demand for their products, so defensive stocks tend to be more stable during the various phases of the business cycle.

Hawkishness – An inflation hawk, also known in monetary jargon as a hawk, is a policymaker or advisor who is predominantly concerned with the potential impact of interest rates as they relate to fiscal policy. Hawks are seen as willing to allow interest rates to rise in order to keep inflation under control.

Inflation – The rate at which the prices of goods and services are rising in an economy. The CPI and RPI are two common measures.

Gearing – Gearing is the measure of a company’s debt level. It is also the relationship between a companies leverage, showing how far its operations are funded by lenders versus shareholders. Within investment trusts it refers to how much money the trust borrows for investment purposes.

Growth stock – A growth stock is any share in a company that is anticipated to grow at a rate significantly above the average growth for the market. These stocks generally do not pay dividends. This is because the issuers of growth stocks are usually companies that want to reinvest any earnings, they accrue in order to accelerate growth in the short term.

Recession – A recession is a macroeconomic term that refers to a significant decline in general economic activity in a designated region.It had been typically recognized as two consecutive quarters of economic decline, as reflected by GDP in conjunction with monthly indicators such as a rise in unemployment.

Value stock – A value stock refers to shares of a company that appears to trade at a lower price relative to its fundamentals, such as dividends, earnings, or sales, making it appealing to value investors.

Valuation metrics – Metrics used to gauge a company’s performance, financial health, and expectations for future earnings eg, price to earnings (P/E) ratio and return on equity (ROE).