Investment Environment

The extreme volatility in global equity markets continued over the third quarter as investors were concerned about the weakening economic environment. The uncertainty this caused meant that some of the areas that had performed well in the previous quarter were among the weaker areas this time. The FTSE World Index was up 1.8%, led by strong US market returns.¹

Ongoing supply-chain issues, surging energy costs and higher food prices pushed inflation to multi-decade highs in major economies. The war in Ukraine continued to have an impact on European stock markets, with Russia’s shut down of the Nord Steam pipeline leading to fears of energy rationing this winter. Cost-of-living crises in the UK and Europe also pressured stocks, with investors fearful of slowing demand from consumers. In response to rising inflation, developed market central banks continued to raise interest rates. However, investors grew concerned that the pace of these rate hikes, especially from the US Federal Reserve (Fed), would cause an adverse economic shock.

Despite overall market weakness, there were developments that may be positive for some of the companies in the portfolio. The passing of the Inflation Reduction Act by US Congress in mid-August is potentially good news for industrial companies such as Roper and Union Pacific. The US government also passed the CHIPS and Science Act to support domestic semiconductor manufacturing capabilities, which we think could be beneficial for holdings such as TSMC in Asia and ASML in Europe.²

Portfolio Review

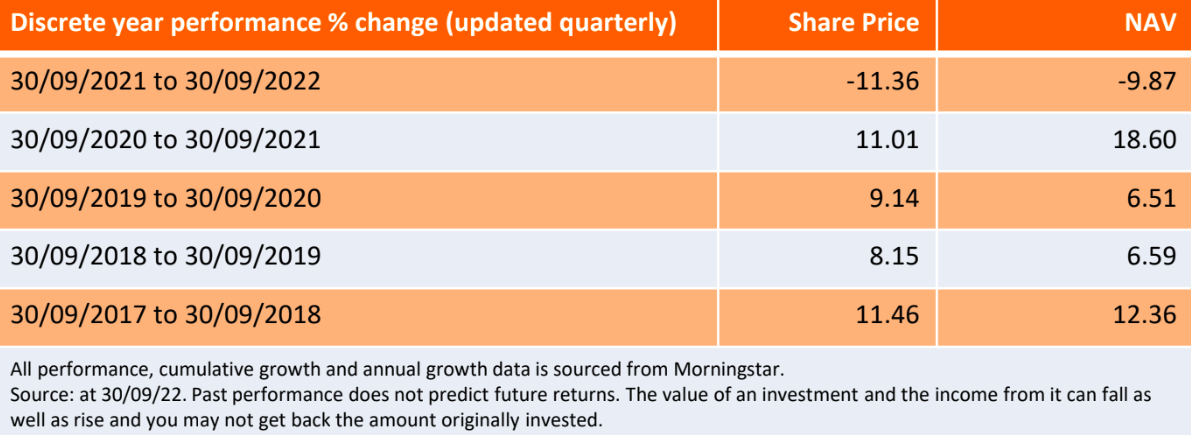

The Company underperformed its benchmark index and ended the period down 2.4%. Although the overall returns were negative, our decision to hold higher levels of cash helped to manage some of the volatility.

Pacific ex-Japan was the strongest performer, while exposure to European equities also contributed positively to relative performance, led by strong stock selection. Although the US portion contributed positively to absolute performance, the underweight position against the benchmark detracted from relative returns as the US substantially outperformed other regions. This was also true of the overweight exposure to the UK, where the government’s mini-budget towards the end of the quarter caused government bond yields to move sharply higher and had a negative impact on stocks of housebuilding companies and mortgage lenders. China reversed its gains from the previous quarter with ongoing concerns around Covid-19 lockdowns affecting investor sentiment. This was a detractor from returns during the quarter. Nonetheless, we believe the market is still attractively valued and the underlying economy remains on a path for long-term growth.

In terms of individual stocks, the leading contributors included some non-UK financial companies, such as Italian bank UniCredit and US-based Moody’s. Exposure to the materials sector through the holding in Australian miner Oz Minerals also had a favourable impact. In contrast, health care companies Sanofi and AstraZeneca were among the detractors, following strong relative performance in previous quarters. Some consumer stocks were also weaker, with the shares of Hilton Food Group in the UK falling after the company issued a profit-warning, saying that it was unable to pass on higher costs to end consumers and that this would have an impact on profit margins.

The UK portion of the portfolio had performed well for most of the year but experienced weakness in September. During the quarter, the manager took the opportunity to reduce the level of exposure and raise cash by trimming some UK holdings.

Manager Outlook

Given the uncertainty in markets, we retain a generally cautious stance. One of the benefits of the way the Company is managed is the ability to adjust levels of investment across regions to take advantage of changes that may be happening in any part of the world. Having sold some holdings to raise cash, we are in the favourable position of being able to react quickly and take advantage when income and capital opportunities arise.

As a diversified fund, the Company’s performance is driven more by its allocation to sectors and regions. We are looking for signs of an earlier recovery relative to markets elsewhere and our feeling is that this may happen in Asia, as the region has been weak for much of this year, rather than the US or Europe, where we believe recovery is still a more distant prospect. China will probably look to expand its economy by stimulating activity through measures such as lower interest rates and by supporting the weak housing market, whereas other economies are likely to be raising rates as a response to higher inflation.

The current outlook remains uncertain given upward pressure on interest rates. Leading indicators of economic activity are weakening while household budgets are strained as a result of high inflation and the energy crisis in Europe. To us, it makes sense to remain cautious with regards to portfolio positioning. Nevertheless, as active investors we continue to look for the best opportunities to take advantage of market dislocations for our clients.

¹Source: Bloomberg as at 30 September 2022.

²Source: https://www.whitehouse.gov/briefing-room/statements-releases/2022/08/09/fact-sheet-chips-and-science-act-will-lower-costs-create-jobs-strengthen-supply-chains-and-counter-china/

Inflation – The rate at which the prices of goods and services are rising in an economy. The CPI and RPI are two common measures.

Volatility – The rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. Higher volatility means the higher the risk of the investment.

Yield – The level of income on a security, typically expressed as a percentage rate. For equities, a common measure is the dividend yield, which divides recent dividend payments for each share by the share price. For a bond, this is calculated as the coupon payment divided by the current bond price.