Perspectives Test article Conor/Jazz/Milo

-

Chris Herringshaw

Chris Herringshaw

Chief Technology Officer -

Olivia Hails, APMA®

Olivia Hails, APMA®

Director, Advisor Solutions Group -

Madeline Saldutti

Madeline Saldutti

Internal Sales Consultant -

Kelly Hagg

Kelly Hagg

Global Head of Product Strategy and ESG -

Nick Sandford, FRM

Nick Sandford, FRM

Risk Analyst -

Emmanuel Cahn

Emmanuel Cahn

Sales Manager -

Dan Fox

Dan Fox

Sr. Director -

Sara Tegethoff Lowery, CRPC®

Sara Tegethoff Lowery, CRPC®

Retirement Director -

Jack Yuan, PhD – REMOVED

Deputy Head of Investment Risk -

Cindy Yan

Investment Risk Associate

Perspectives Test article Conor/Jazz/Milo

-

Chris Herringshaw

Chief Technology Officer -

Olivia Hails, APMA®

Director, Advisor Solutions Group -

Madeline Saldutti

Internal Sales Consultant -

Kelly Hagg

Global Head of Product Strategy and ESG -

Nick Sandford, FRM

Risk Analyst -

Emmanuel Cahn

Sales Manager -

Dan Fox

Sr. Director -

Sara Tegethoff Lowery, CRPC®

Retirement Director -

Jack Yuan, PhD – REMOVED

Deputy Head of Investment Risk -

Cindy Yan

Investment Risk Associate

Given fluctuating markets and changing leadership as the economic recovery progresses, Portfolio Manager Nick Schommer discusses how it may be prudent to sharpen the focus on sources of risk and return within one’s portfolio and seek to ensure these are not overly correlated.

Key Takeaways

- The recovery to date has been highlighted by distinct swings in leadership ‒ between value and growth, smaller- and larger-capitalizations and cyclical and secular growth stocks.

- Given fluctuating markets and changing leadership it may now be prudent to sharpen the focus on sources of risk and return within one’s portfolio and seek to ensure these are not overly correlated.

- A portfolio not dependent on specific market capitalizations, styles or sectors, but rather, focused on quality business models, may benefit from uncorrelated sources of risk and return with the potential to perform across multiple market scenarios.

In our view, the shifting nature of the COVID economic recovery has brought into focus the potential value of owning diversifying equity assets. A blend of holdings that do not look like the S&P 500® Index, are not dependent on specific market capitalizations, styles or sectors, but rather exhibiting the attributes of durable business models with the potential to perform in different market scenarios, may prove beneficial at this stage in the cycle.

The COVID recovery has been swift, but uneven

While COVID initially created a severe economic contraction – akin to a natural disaster – we believed for some time that a health care solution to the pandemic would enable a similarly swift rebound. As the vaccination effort has steadily progressed in the U.S., consumers eager to re-engage with the physical economy have released substantial pent-up demand, and GDP growth has accelerated significantly. Powerful fiscal and monetary stimulus, strong capital market performance and a robust housing market have likewise positioned both individuals and corporations to reinforce an already widening economic recovery. Recently, though, the Delta variant has raised fears of slowing consumer demand. At the same time, supply chain bottlenecks and raw material and labor shortages have stoked inflation concerns and the potential for stormier weather ahead from an interest rate and economic data standpoint.

So, we have witnessed an ongoing push-pull in markets, and the recovery to date has been highlighted by distinct swings in leadership ‒ between value and growth, smaller- and larger-capitalizations and cyclical and secular growth stocks. At the end of last year and earlier this year, cyclical, more value-oriented stocks assumed market leadership. These were companies positioned to benefit from a reopening and a normalization of the economy in industries like travel where consumers directed pent-up demand and savings. Cyclical companies ‒ which tend to have a greater degree of operating leverage and perform better during periods of higher GDP growth – in general, rebounded strongly as the market gained confidence in a v-shaped recovery.

Diversifying Away from Big Tech

This is a stark reversal of the theme that saw the digital economy continue to thrive while the physical economy stalled at the onset of the pandemic, when a handful of large technology companies benefitted directly from the COVID environment. As with any crisis, the pandemic created a set of economic challenges that exposed weakness in certain business models and created opportunity for others. As businesses and consumers became increasingly dependent on ‒ and comfortable with ‒ digital technology during widespread lockdowns, big tech companies’ prominence in the economy grew.

As it stood in August, the information technology and communication services sectors made up 39% of the S&P 500 Index (as of 8/16/21). Out of eleven economic sectors, information technology alone was larger than six sectors combined (energy, utilities, materials, real estate, consumer staples and industrials). What’s more, the largest five stocks represented nearly 22% of the index, a level of concentration not seen even in the 2000 dot-com bubble (as of 6/30/21).

Chart 1: S&P 500 Index – sector weightings (%)

PLACEHOLDER

Chart 1: S&P 500 Index – sector weightings (%)

PLACEHOLDER

Many investors’ primary exposure to U.S. equities is associated with the S&P 500 Index, which represents approximately 80% of the total value of the U.S. market.1 However, as illustrated above, the S&P 500 has become ‒ perhaps unwittingly to many ‒ an index increasingly concentrated in a handful of large-cap technology stocks ‒ a development that is certainly not without risk. This is not to say these stocks are not worth owning or bad companies. On the contrary, they have seen strong growth in recent years. As illustrated in the table below, over the trailing three years through to the end of September 2020, the S&P 500 (which is market capitalization weighted, giving greater influence to the largest stocks) outperformed the equal-weighted S&P 500, due largely to the strong performance of the mega-cap tech stocks. But, particularly as the economic recovery has broadened, we have witnessed a substantial leadership change, as illustrated in the period since September last year during which the equal weighted index has significantly outperformed.

Featured Funds

JUCIX

Short Duration Income ETF

JUCIX

Short Duration Income ETF

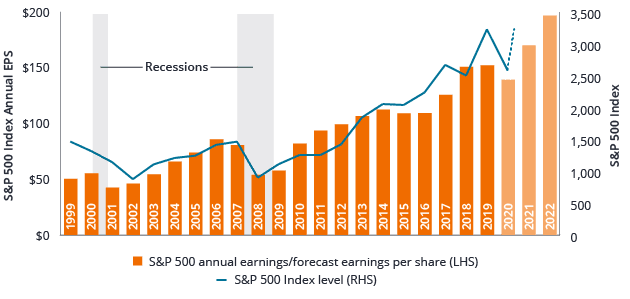

Yet, we believe 2020’s highfliers have the potential to be joined by other sectors as evidence builds that a “V-shaped” recovery is emerging. We are witnessing considerably improving data across the economy. Major global purchasing manager indices have returned to expansion territory, as seen in Exhibit 2. These leading indicators align with consensus expectations that after contracting by 3.9% in 2020, global economic output should rise by 5.2% next year and 3.6% in 20221.

Glossary Expand Global Perspectives Asset Class Tag 1 Tag 2 View All Perspectives