Knowledge. Shared Blog

March 2020

Millennials’ First Market Correction: Advice from an Ancient Philosopher

-

Ben Rizzuto, CRPS®

Ben Rizzuto, CRPS®

Retirement Director

Younger investors experiencing their first major market correction may be feeling anxious, fearful and uncertain about whether they want to remain invested. Drawing on the teachings of the Greek Stoic philosopher Epictetus, Retirement Director Ben Rizzuto illustrates the importance of maintaining a long-term perspective during times of short-term volatility.

You’re young. You’ve recently entered the workforce and you’re discovering what it feels like to support yourself and be financially independent. And while retirement feels like a long way off, you’ve started investing some of your discretionary income to save for the future.

But then, just as you dip your toe into the investing pool, COVID-19 causes the formerly robust and seemingly invincible stock market to sink into bear market territory in a matter of days.

Welcome to investing!

If current events and the volatility they’ve created are making you rethink your asset allocation and question how much volatility you can handle, you’re not alone. It’s perfectly normal to experience some level of stress or anxiety in the face of such dramatic market moves, not to mention unprecedented uncertainty about what the future may hold.

Where do you turn for guidance in these volatile times? Turns out, the wisdom of a philosopher who lived between c. 55 and 135 A.D. may hold some useful insight for today’s younger investors.

The Greek Stoic philosopher Epictetus provided his students with ideas on how to live one’s life. Based on his teachings, the following are some ideas that may help provide perspective.

What Can You Control?

Here is Epictetus’ take on the concept of control:

The chief task in life is simply this: to identify and separate matters so that I can say clearly to myself which are externals not under my control, and which have to do with the choices I actually control.”

Epictetus, Discourses, 2.5.4-5

The Takeaway: You can’t control the markets – none of us can. They go up AND down and have done so for years. What we’re going through now is something many others have experienced over the years.

If you can’t control the markets, what can you control? The key to navigating this type of volatility is our reaction. Over the past several days, you may have felt despair, anger and frustration. Those emotions can lead us to make untimely (and costly) errors, such as selling investments near or at a market bottom. Remember, the basic rule of stock market investing is to buy low and sell high; if you give in to these emotions and sell now, you could be being doing the exact opposite.

Separating Short-Term and Long-Term Events

First off, don’t let the force of the impression carry you away. Say to it, ‘hold up a bit and let me see who you are and where you are from – let me put you to the test…”

Epictetus, Discourses, 2.18.24

While the ups and downs of the market are out of your control, the way you’re invested – also known as your asset allocation – is something you can control.

Just as the name suggests, asset allocation is the percentage of assets you have allocated among equities, fixed income or other asset classes. As a younger person, your time horizon (i.e., when you will need this money) is quite long. You’re not going to retire for at least 20 – if not 30 or even 40 – years. Your longer time horizon allows you to be more aggressive by allocating more of your assets to equities and less to fixed income.

The reason you can afford to take on more risk is because you have more time to make up for any losses you see in your portfolio. As you get older and closer to retirement, your asset allocation will likely become more conservative, but this is a change that happens gradually over your lifetime and should not be based on short-term swings.

Unfortunately, the emotions that are stirred during significant market shifts can lead many investors to make drastic changes in their asset allocation. Loss aversion – the idea that the pain we experience from losses greatly exceeds the contentment we derive from gains – looms large during volatile markets. Sometimes, this pain leads people to move completely to cash in an effort to limit losses and gain a sense of control and security. And while it may help ease our anxiety, it is only a short-term fix.

The worst part is that, once the markets return to normal, investors often fail to reallocate themselves appropriately. They may continue to be more conservative with their investments than they should be or stay in cash because they are still affected by the emotions recent events have elicited.

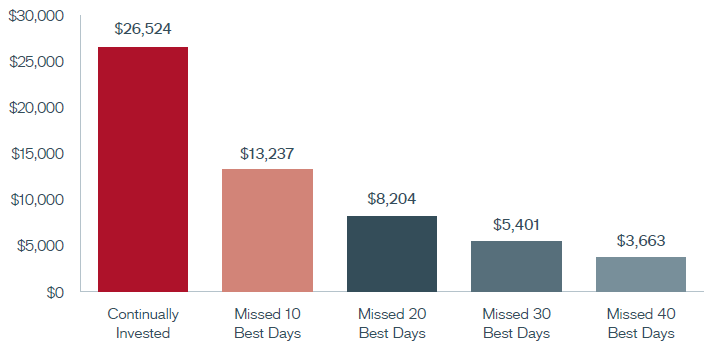

The Takeaway: You may not need to make drastic changes in your long-term asset allocation based on short-term events. As the chart below illustrates, doing so has historically led investors to miss out when the market rebounds.

Value of a Hypothetical $1,000 Investment in the U.S. Equity Market, 1988-2019

[caption id=”attachment_278669″ align=”alignnone” width=”704″] Source: FactSet Research Systems, Inc., 1/1/88 – 12/31/19. U.S. equity market represented by the S&P 500® Index. Each of these bars represents the value of a hypothetical $1,000 investment in the U.S. equity market over a 31-year period. The differences among them reflects small pockets of market rallies in which the investor did not participate. Thee example provided is hypothetical and used for illustration purposes only. It does not represent the returns of any particular investment. Past performance is no guarantee of future results. [/caption]

Source: FactSet Research Systems, Inc., 1/1/88 – 12/31/19. U.S. equity market represented by the S&P 500® Index. Each of these bars represents the value of a hypothetical $1,000 investment in the U.S. equity market over a 31-year period. The differences among them reflects small pockets of market rallies in which the investor did not participate. Thee example provided is hypothetical and used for illustration purposes only. It does not represent the returns of any particular investment. Past performance is no guarantee of future results. [/caption]

The Educated Investor

Only the educated are free.”

Epictetus, Discourses, 2.1.21-23a

While you don’t need to be an expert on the markets to be a successful investor, it is important to be educated and to understand how financial markets function from a historical perspective.

There have been several corrections and recessions over the years. A correction is defined as a decline of 10% or more from the recent peak, whereas a recession is often defined as a period when a country’s GDP growth rate is negative for two consecutive quarters. We have seen corrections and recessions in 1990, 2000, 2008 and several other periods in the past. And during each of these phases, young investors like you have felt the same dread you may be experiencing now. But if you look at the patterns that have unfolded over time, you can see that staying in the market over the long term has paid off.

Viewing the performance of the market over a short period of time can look like this:

[caption id=”attachment_278680″ align=”alignnone” width=”716″] Source: Daily closing levels for the Dow Jones Industrial Average, 12/3/07 – 6/30/09.[/caption]

Source: Daily closing levels for the Dow Jones Industrial Average, 12/3/07 – 6/30/09.[/caption]

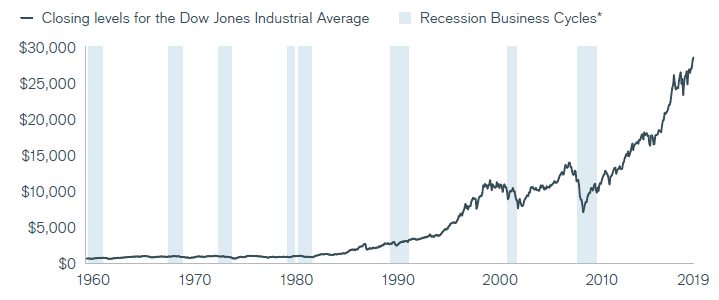

The chart above looks like a losing proposition. But if we zoom out and look at a longer period, we can see that this only a small piece of a larger – much more favorable – picture.

[caption id=”attachment_278691″ align=”alignnone” width=”719″] Source: Morningstar, Inc. from 4/29/60 – 12/30/19. Monthly closing levels for the Dow Jones Industrial Average from 4/29/60 – 12/31/19. Shaded areas represent recession business cycles. Recession business cycles are defined by the National Bureau of Economic Research. Recessions noted: 4/60-2/61, 12/69-11/70, 11/73-3/75, 1/80-7/80, 7/81-11/82, 7/90-3/91, 3/01-11/01 and 12/07-6/09. [/caption]

Source: Morningstar, Inc. from 4/29/60 – 12/30/19. Monthly closing levels for the Dow Jones Industrial Average from 4/29/60 – 12/31/19. Shaded areas represent recession business cycles. Recession business cycles are defined by the National Bureau of Economic Research. Recessions noted: 4/60-2/61, 12/69-11/70, 11/73-3/75, 1/80-7/80, 7/81-11/82, 7/90-3/91, 3/01-11/01 and 12/07-6/09. [/caption]

The bottom line is, it’s generally wise to stay invested. History has shown that taking the long view and staying invested has paid off in the end. If you look at several past recessions, they look like bumps in the road along the path of long-term growth.

Your experience with the market may be relatively short. And it may be off to a rocky start. But remember: Your long-term financial success won’t be made on short-term emotions. In fact, during these times it might be a good idea to turn off the TV, stop looking at the market and contemplate some philosophy.

Knowledge. Shared

Blog

Back to all Blog Posts

Subscribe for relevant insights delivered straight to your inbox

I want to subscribe