Key takeaways:

- Inflation impacts demand and increases costs for companies. Exciting thematic areas with long payback periods can be squeezed as the cost of capital rises; this requires tech investors to apply a more rigorous valuation discipline and focus on balance sheet strength.

- Technology does however, have a long track record of making products and processes cheaper, faster and better.

- Digital transformation and adoption of technology solutions can be used as a long-term strategy to combat higher inflation by increasing productivity, automation and resource optimisation.

During the height of the COVID-19 pandemic, governments and businesses around the world had to shut down most forms of physical production and investment, essentially taking the supply curve to zero. At the same time, unprecedented levels of fiscal and monetary stimulus had to be provided to manage through the crisis. Shifts in demand and supply have unsurprisingly created an inflation spike with ongoing supply chain difficulties, labour shortages, rising healthcare costs, transportation bottlenecks, and higher fuel costs amid the backdrop of an ever-present demographic time bomb coming more into focus.

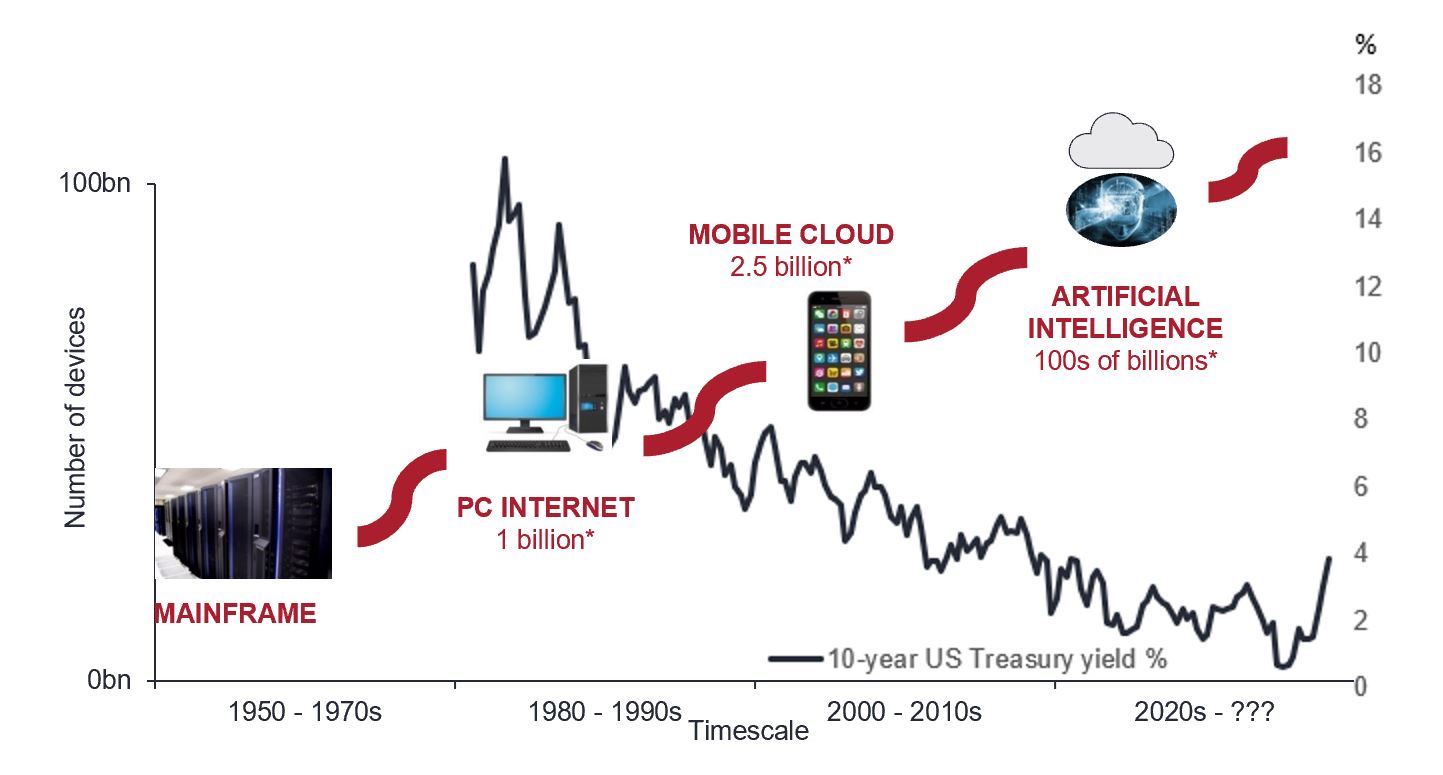

While goods inflation may abate with energy prices, the greatest costs pressure comes from services, primarily wages, which may prove stickier and more difficult for central banks to address with higher interest rates. As economics scholars remind us of Gibson’s paradox and the Fisher effect, governments and central banks globally are wrestling with how to sustain a post-COVID economic recovery and manage soaring inflation. Philosophically, the Global Technology Leaders Team has always considered technology to be the science of solving problems. The relationship between lower bond yields and inflation, and the adoption of technology has been evident over a 25-year period. Historically, the combination of technology adoption and globalisation via increased productivity, reduction in labour and input costs, integration of supply chains etc, lowered expectations for inflation and drove down bond yields.

Rising technology adoption has driven lower inflation and falling bond yields over the long term

Source: Janus Henderson Investors, *Citi Research, as at 30 December 2016. Bloomberg US 10-year Treasury yields March 1980 to September 2022.

To be upfront, we are not suggesting that technology spending will benefit in the short or medium term from inflationary pressures. The fight against inflation requires not just central bank monetary tightening but also for governments and corporates to scrutinise all areas of expenditure, including technology. However, we agree entirely with the sentiments of Satya Nadella, CEO of Microsoft, that “technology is a deflationary force in an inflationary economy.” We believe that in the long term, investment in digital transformation, productivity and resource optimisation tools will be viewed as areas of spending to combat rather than fuel inflation.

Why is technology such a deflationary force?

Essentially, technology has been making products and processes cheaper, faster and better. In 1965, Gordon Moore posited that roughly every two years the number of transistors on microchips would double and prices would halve. Moore’s Law enabled compute power to ramp up exponentially with falling costs. It democratised compute power – over the following 50 years enabling the power of a1960s NASA supercomputer to be in the pockets of half of the people on the planet. While the principle of Moore’s Law is now under stress for microchips, the basic notion that technology can make products and processes cheaper, faster and better is alive and well. We can see this across many areas, for instance, in hyper scale data centres where the leading cloud service providers are driving down compute and storage costs, and within clean energy and in electric vehicles (EVs) where technology is enabling affordability and functionality.

How can growth in technology adoption help reduce the impacts of higher inflation?

We discuss some examples of technology providing solutions to improve productivity, automation and resource optimisation:

- Low carbon, low power infrastructure

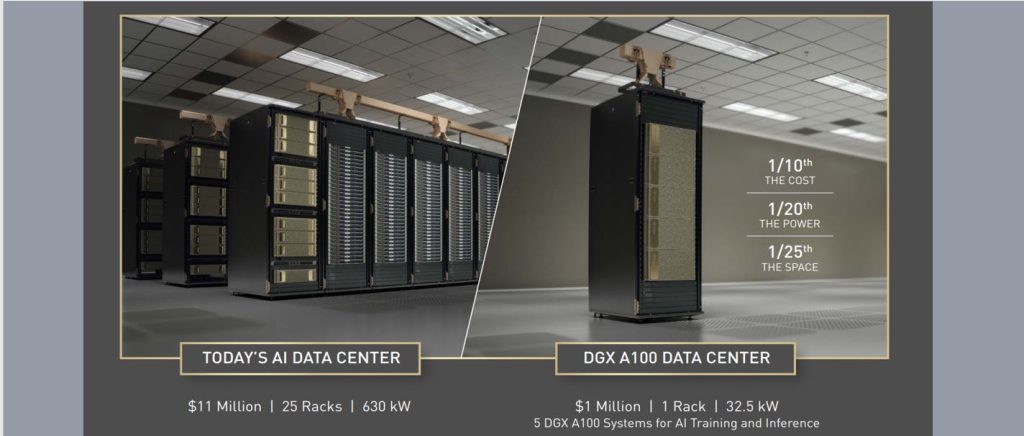

Compute proliferation drives exponential leaps in power consumption. This is a climate change and energy resource constraint challenge that requires a transition to low carbon cloud and 5G architectures. Despite the explosion in data, data centre electricity consumption has stayed nearly flat over the last ten years because of a shift to cloud compute and hyperscalers with super-efficient datacentres. Hyperscalers have significantly better power usage efficiency (PUE). In 2018 a study by Microsoft showed that its Azure cloud platform could be up to 93% more energy efficient and up to 98% more carbon efficient compared to on-premise solutions. Investment in vertically-integrated solutions, such as nVIDIA’s graphics processing units (GPUs) in server racks that use 1/20th of the power consumption of traditional racks or flash storage systems that can result in over 50% energy savings. Hyperscale companies are also leading the path in the use of renewable energy, moving beyond the offsetting of carbon emissions towards using fully carbon-free electricity. Alphabet’s Google has set a target to power its data centres and offices 24/7 with carbon-free electricity by 2030. Meanwhile, enterprises had been considering a shift to the public cloud as a means to enhance digital transformation, flexibility and a more operating rather than capital expenditure-driven IT budget cycle. Now, energy costs, energy security and carbon emissions are emerging as powerful motivators for the transition.

Problem: High energy costs

Solution: Next generation, low carbon infrastructure

Source: nVIDIA, as at 31 May 2022. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

- Technology and new business creation

In 2021, almost 5.4 million people in the US applied for small business licences – a rise of more than 50% from 20191. Global start-up funding reached $643bn, a tenfold increase compared to a decade ago.2 Why have we seen this boom in business start-ups? Interest rates and funding have been relatively low and readily available but at the core of the start-up trend has been the fact that technology has made it easier for start-ups. Unlike in the dot.com era, companies don’t need to borrow tens of millions of dollars to buy compute power and storage – they can simply rent it from a cloud service provider now. Nor are enormous budgets required for advertising and sales to get to market and open and connect to distribution channels. The likes of Alphabet, Meta and TikTok have created targeted and self-service means to advertise, while marketplaces from Etsy to eBay and Amazon offer access to customers, with the latter also offering warehousing and logistics. Payment digitisation has made invoicing, inventory management and logistics easier than ever before. So while many criticisms have been levelled at large-cap tech companies, they have enabled many more start-ups that are uniquely poised for innovation and creativity. One of the fastest growing small business sectors is the ‘creator economy.’ Linktree’s 2022 Creator Report noted there are now 200 million content creators3 including those on creator platforms such as Instagram, YouTube, Facebook and TikTok monetising their content and making supplemental income.

- Resource optimisation and the circular economy

Being able to track and reuse products can significantly boost productivity. Asset tracking in the supply chain, transport and logistics can help to optimise the storage of goods as well as their transportation saving miles driven and optimising capacity. By using microchips and software to track assets, companies in sectors as diverse as retail, healthcare, airlines and manufacturing are now able to view asset locations in real time, gaining visibility into equipment status and better able to plan resource use.

- Enabling electrification

Clean energy and sustainable transportation is being powered by technology, which is enabling the transition to renewable energy and sustainable transportation, including zero emission vehicles, ride hailing and autonomous driving. But how does this fit into addressing inflation? Look no further than the Inflation Reduction Act in the US, which was passed in August this year. This was the largest piece of federal legislation ever to address climate change. The bill created tax incentives to shift to electric vehicles made in the US, build a cleaner manufacturing sector and enhance wind and solar energy capacity. Investment in technology enables solar costs to keep declining and efficiency to improve, and for EVs to become more competitive. For example, solar inverters and micro inverter advances can not only improve solar conversion rates but also reliability and more seamless integration of solar power with the grid. For EVs, power semiconductors, using greener technologies like silicon carbide and more advanced intelligent battery management systems can drive battery efficiency. Ultimately, this can increase range as well as extend the lifespan of batteries via a second life in energy storage.

- Improving labour productivity

Productivity and resource optimisation are key to addressing skilled labour shortages. Technology’s role is not limited to enabling education and skills access online. Robotics and artificial intelligence (AI) are providing smart ways to upskill the workforce. Software is enabling better alignment with peak customer demand times with enhanced labour scheduling. Additionally, cloud software companies are helping many industries to restructure workflow and automate responses, while in healthcare, robotic surgery is facilitating the sharing of best practice from the most skilled surgeons.

- Managing healthcare costs

Over the last 25 years consumer prices have rarely risen faster than healthcare inflation (doctor visits and prescription costs), and even after the financial crisis in 2008 when overall inflation slowed, medical prices continued to grow. Post-COVID, the impact on healthcare costs has lagged but a recent study by business consultants McKinsey noted the inevitability of healthcare inflation catching up again to overall services. The recommendations for how governments and healthcare providers could prepare and offset this were unsurprisingly very technology-centric, with a need for “healthcare organisations to fundamentally reset themselves to achieve greater productivity through the addition of digital and advanced analytics”. Administrative spending accounts for approximately 25% of $4 trillion spent on US healthcare.4 Automating scheduling, patient access, and streamlining clinical workflows are all ways to address rising costs in the sector. In the long term, using AI to hone in faster on compounds that are clinically promising can reduce time spent on preclinical drug development by as much as 75% and reduce early stage development costs by up to half. AI, harnessing massive compute power will also be key to lowering costs of expensive blood screening, which could lead to early detection of illnesses and cheaper treatment plans.

A focus on valuation discipline remains imperative for tech investors

This gives just a flavour and a subset of areas and examples that can explain why companies will continue to invest in digital transformation, even in a period of weaker economic growth and higher inflation. However, it is important to note that while these areas may offer exciting investment opportunities, the uncertain macro backdrop also demands that investors apply more rigorous valuation discipline and seek out companies with strong balance sheets and solid free cash flow prospects. This entails having a focus on navigating the hype cycle, looking at how to invest in companies benefiting from secular themes with long-term growth potential but doing so only when there are rational expectations of growth and reasonable valuations, coupled with balance sheet strength that allows companies to capitalise on their competitive advantages.

Sources:

1 https://home.treasury.gov/news/press-releases/jy0924

2 https://news.crunchbase.com/business/global-vc-funding-unicorns-2021-monthly-recap/

3 https://linktr.ee/creator-report/#ToC

4 McKinsey.com: The gathering storm: the transformative impact of inflation on the healthcare sector, 19 September 2022.

Disclaimers:

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Gibson’s paradox is the observed, long-run, positive correlation between interest rates and the price level in Great Britain under the gold standard. John Maynard Keynes later called this relationship a paradox because he claimed that it could not be explained by existing economic theories. The Fisher Effect is an economic theory created by economist Irving Fisher that describes the relationship between inflation and both real and nominal interest rates. The Fisher Effect states that the real interest rate equals the nominal interest rate minus the expected inflation rate.

Graphics processing units (GPUs) are designed for parallel processing. A GPU is a specialised electronic circuit card that works alongside the brain of the computer, the central processing unit (CPU), to enhance the performance of computing.

Bond yield: the level of income on a security, typically expressed as a percentage rate. Note, lower bond yields mean higher prices and vice versa.

Monetary tightening: refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money.

Hype cycle: represents the different stages in the development of a technology from conception to widespread adoption, which includes investor sentiment to that technology and related stocks during that cycle.

Inflation/deflation: Inflation is the rate at which the prices of goods and services are rising in an economy. The opposite is deflation, a decrease in the price of goods and services across the economy, usually indicating that the economy is weakening.