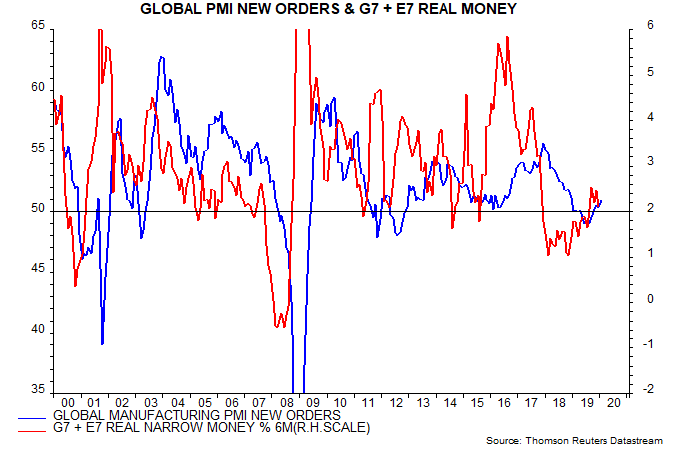

The global manufacturing PMI new orders index reached a 13-month high in January but narrow money trends suggested that it was on course to peak around April and relapse into mid-year. The 2019-nCoV shock will alter this timing, causing near-term weakness and a subsequent bounce-back. A key issue is whether the virus hit acts as a catalyst for further monetary policy loosening sufficient to revive money growth, in which case economic prospects for late 2020 will have improved.

The global manufacturing PMI new orders index rose from a low of 49.0 in June 2019 to 50.9 in January but remains below its long-term average (1998-2019) of 52.6. The June low occurred seven months after a low in global six-month real narrow money growth in November 2018. Real money growth rose to a peak in September 2019, falling back into December. Assuming another seven-month lead, this suggested that the new orders index would peak in April 2020 and fall into July – see first chart.

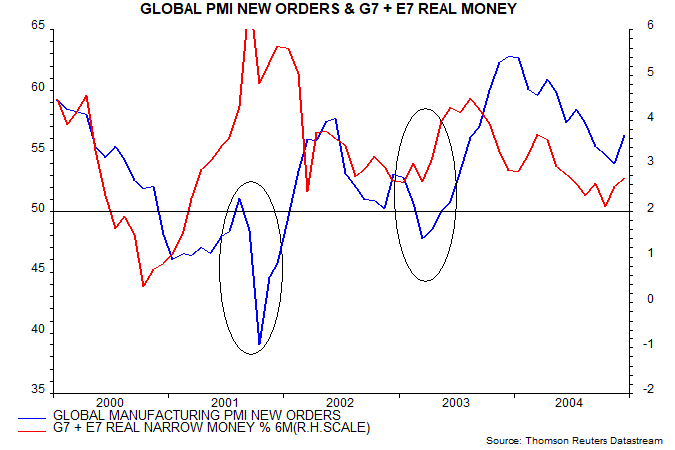

The economic impact of the epidemic may prove similar to that of the 2001 US terrorist attacks and the 2003 SARS epidemic. The global manufacturing PMI new orders index fell by 12.1 and 5.3 points over two and three months respectively. From the low, the index took four months in both cases to surpass the pre-crisis peak – second chart.

The new orders index, therefore, could plunge back below 50 in February, reaching a low in March / April before rebounding into July / August. Global money trends are weaker than in 2001 and 2003: six-month real narrow money growth was strong and rising at the time of the 911 attacks; it was slipping but above the current level when SARS struck – second chart.

Both shocks contributed to an extension of prior monetary policy loosening, helping to sustain monetary strength in 2001 and leading to a sharp pick-up in real money growth over March-June 2003. Economic growth was subsequently strong in H1 2002 and H2 2003 respectively.

Assuming a similar policy response now, real money growth could pick up again from March / April, signalling economic acceleration in late 2020 / H1 2021.