Global Sector Views

Quarterly Equity Overview and Sector Highlights

Key Takeaways

- A number of leading economic indicators suggest the U.S. economy, now more than 10 years into its expansion, could be nearing a recession.

- But while growth appears to be slowing, we believe the U.S.-China trade war has amplified worries over the economic outlook and could be distorting some indicators.

- As such, we think investors should be prepared for heightened market volatility and focused on so-called defensive growth companies: firms with secular growth drivers, strong balance sheets and competitive advantages.

MARKET OVERVIEW

Navigating an Uncertain Economic Outlook

More than 10 years since the Global Financial Crisis, the U.S. economic expansion is now the longest on record – leading many investors to wonder whether a recession is just around the corner.

Plenty of signals suggest a contraction could be nearing. In August, the yield on the 10-year U.S. Treasury temporarily fell below that of the two-year note, creating a so-called inverted yield curve – a phenomenon that has occurred before every U.S. recession since 1955. During the same month, economic activity in the U.S. manufacturing sector contracted for the first time in nearly three years as measured by the Institute for Supply Management’s Purchasing Managers’ Index (PMI). Manufacturing activity declined even more in September, while PMIs also contracted in the UK, eurozone, Japan and select emerging markets.

The Trade War Wrench

We track these signals closely. And yet, we also believe that trade tensions could be distorting the outlook. Take private-sector capital expenditures (capex): In recent months, spending plans by large manufacturers, many of which have multinational operations, have plummeted as a result of uncertainty about supply chains and waning overseas demand. However, capex plans by small-cap manufacturers, which tend to be domestically oriented, have stayed relatively consistent. Furthermore, although some management teams tell us they are hitting the pause button on “want-to” capex (say, to expand capacity), needed capex (i.e., maintenance) is continuing. And in some secular growth industries, such as warehouse automation, orders have actually picked up.

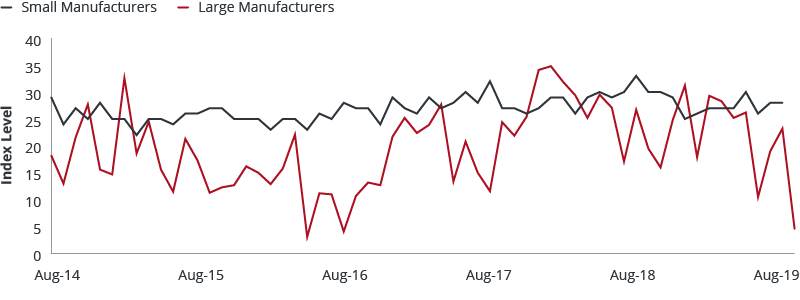

Exhibit 1: Manufacturing Capex Plans

Capital spending plans among large manufacturers dropped precipitously in September, but spending among smaller companies, less vulnerable to trade uncertainties, has been more consistent.

Notes: Data based on NFIB Small Business Capital Expenditure Plans and US Empire State Manufacturing Survey 6-Month Ahead Capital Expenditures (Seasonally Adjusted).

Then there’s the consumer. In the U.S., rising wages, low unemployment and declining interest rates are creating a favorable backdrop for households. In turn, personal expenditures have continued to expand, retail sales are growing and existing home sales hit a 17-month high in August. Consumer confidence measures have dropped recently but still remain elevated (and, historically, tend to be volatile).

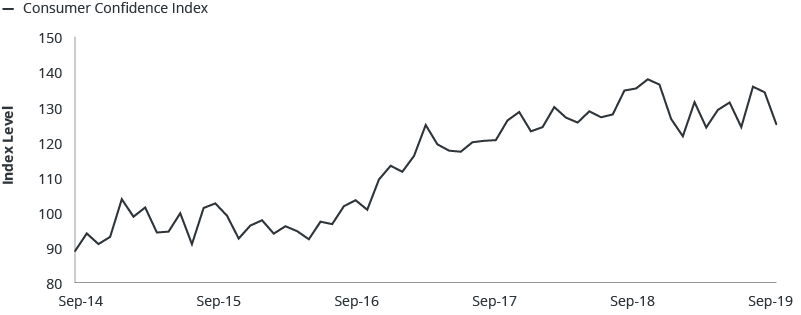

Exhibit 2: Consumer Strength

Trade uncertainty has led to volatility in consumer confidence but has not stopped spending in areas such as home purchases.

Source: Bloomberg, Conference Board, and the National Association of Realtors.

Consumer confidence data are as of 9/30/14 – 9/30/19, and existing home sales data are as of 1/31/18 – 8/31/19.

In short, most signals suggest the U.S. economy is slowing but is not at the point of jumping headfirst into a recession. However, when growth slows, external shocks can deliver outsized blows to sentiment and ratchet up market volatility. We do not see significant financial or structural risks to the U.S. economy, such as excessive household or bank debt. But we have had to absorb geopolitical shocks, such as the escalation of the trade war and the recent attack on Saudi Arabian oil facilities. What’s more, these types of events could proliferate as the deadline for Brexit nears, the 2020 U.S. presidential election approaches and China grapples with its own economic slowdown. Plus, there are other issues to potentially contend with, including what happens if monetary policy loses its firepower after years of easing.

Looking for Defensive Growth

Consequently, we think investors should brace themselves for more market volatility. In September, as trade tensions seemed to ease, investors quickly bought up stocks of cyclical companies (firms whose revenues tend to be tied to the economic cycle), which previously had been beaten down. The rotation was so swift that it led to the largest divergence in performance this decade between these stocks and those of faster growth companies, according to one industry report.

Rather than chase market whims, we’d prefer to look for what we call defensive-growth companies. These are firms whose business models are benefiting from secular growth drivers – say, from the electronification of global payments or the shift to the cloud – and therefore are less dependent on economic expansion for growth. The companies also tend to have strong balance sheets, positive free cash flow and competitive advantages that make it possible to defend or increase market share. The stocks may not always outperform. But while we don’t see signs of an imminent recession, we’d rather throw our hat in with firms that have the potential for consistent growth, no matter what the next shock might be.

Download a PDF of the 3Q Global Sector Views here.

SECTOR OVERVIEW

Consumer

Consumer

Consumers Stay Calm and Carry On

Despite worries about slowing economic growth and ongoing trade wars, U.S. consumers have been resilient. Monthly spending continues to rise, while consumer confidence has been choppy but still elevated. Meanwhile, falling interest rates are helping grease an already-easy borrowing environment: In mid-September, a weekly measure of home refinancing activity was up 169% from the year before. President Trump’s decision to postpone tariffs on a large swath of consumer goods from China also boosted confidence and helped to lift stocks of merchandisers viewed as sensitive to economic growth.

Investment Implications

Although the consumer backdrop is encouraging, we remain focused on finding companies that we believe have long-term secular growth potential. These include firms that operate in strong product categories, offer leading brands and have opportunities to expand market share. In beverages, for example, changing consumer preferences are lifting sales of non-U.S. beer brands, which remain underrepresented on store shelves. Cable operators also appear well positioned in light of rising U.S. household formations, while we think home-supply stores could benefit from the aging U.S. housing stock as homeowners spend on repairs and renovation. At the same time, new competition in over-the-top streaming services is creating volatility for these firms. Long term, however, we believe both content and scale are essential for this category, which should lead to industry

Energy & Utilities

Energy & Utilities

Uncertainty in the Middle East

A drone attack on Saudi Arabian oil facilities in September drove one of the largest one-day rallies in crude prices in recent history, with Brent jumping 15% to $69 per barrel and West Texas Intermediate (WTI) rising by the same percentage to $63. (Brent measures global crude prices, while WTI is a benchmark for U.S.-produced oil.) The attack temporarily disrupted 5% of the global oil supply and highlighted the vulnerability of Saudi Arabia, the world’s largest exporter. Meanwhile, forecasts for oil demand have edged lower on concerns about slowing economic growth. In September, the U.S. Energy Information Administration estimated that global oil demand would rise by just 0.9 million barrels per day (bpd) in 2019, down from 1.3 million bpd the year before.

Investment Implications

In light of weaker oil demand and restored supplies (helped by Saudi Arabia’s ample reserves and spare capacity), we expect WTI to range from $55 to $65 per barrel through the end of the year, and Brent to be priced from $60 to $70. However, market volatility could continue given increasingly complex supply/demand variables for crude. As a result, we remain focused on high-quality exploration and production (E&P) companies that could still be profitable in a range-bound environment. We also think Canadian oil sands producers could benefit if market participants increasingly favor firms located in politically stable regions. Meanwhile, U.S. E&Ps continue to improve efficiencies, boosting output with fewer rigs. In our opinion, the trend is a positive for midstream operators, which manage pipelines and transport systems, but a headwind for oilfield service companies.

Financials

Financials

Rate Moves Lead to Volatility

Sharp moves in bond yields and uncertainty about the global economy led to volatility in the sector during the third quarter. Defensive subsectors such as property insurance, real estate investment trusts (REITs) and securities exchanges outperformed as the yield on the 10-year Treasury swooned, only to underperform more rate-sensitive categories such as banks and e-brokers when rates rebounded. Outside the U.S., the environment was more consistently negative given political unrest in Hong Kong, trade worries in China, uncertainty around Brexit and the European Central Bank’s decision to push rates further into negative territory. India, however, was one notable exception as the country announced plans to drastically cut the corporate tax rate. Beyond rates and geopolitics, a number of structural tailwinds continued, including the electronification of trading markets, rising global demand for wealth management services and growth opportunities created by data analytics and technology.

Investment Implications

Rather than try to make a call about future rate moves, we continue to look for companies across the sector that we believe have the best potential for risk-adjusted growth. That includes banks with large U.S. deposit franchises that are leveraging their scale and technology to take market share. We also favor securities exchanges, which continue to build organic growth drivers through electronification, data and analytics. Similarly, payments firms continue to benefit from the rise of digital transactions, including new growth channels such as business-to-business and person-to-person payments. In emerging markets, we favor firms that benefit from a rising middle class that increasingly seeks banking services, wealth management and insurance. And in India, we believe corporate banks will be strong beneficiaries of recently announced tax cuts.

Health Care

Health Care

Reform Stays at the Forefront

Health care stocks continue to underperform the broad equity market as uncertainty about drug pricing reform and the upcoming presidential election weigh on the sector. In July, the Senate Finance Committee passed a bill that would curb price increases for certain prescription drugs while limiting out-of-pocket costs for Medicare beneficiaries. Subsequently, Speaker Nancy Pelosi introduced a bill that would allow the government to negotiate the price of up to 250 name-brand drugs, including insulin. Meanwhile, signs that presidential candidate Sen. Elizabeth Warren is gaining in the polls also raised worries about the possibility of a single-payer health care plan being introduced should she win the 2020 U.S. election.

Investment Implications

With the election nearing, we believe it is unlikely Congress will pass a bipartisan drug pricing bill in the coming months. It is also difficult to accurately forecast who will become the next U.S. president. However, we think political uncertainty could remain an overhang for the sector, particularly for pharmaceutical and private health insurance firms. As such, on the margin, we favor medical device and tool makers, as these companies largely sit outside the debate in Washington, D.C., and, in some cases, offer leading products in areas with long growth cycles, such as robotic-assisted surgery, life science research tools and continuous glucose monitoring for diabetes. Similarly, we also like companies that manufacture cash-pay products, such as contact lenses, as well as animal health. Finally, we continue to focus on biopharmaceutical and biotech firms that are innovating products with the potential to substantially improve patient outcomes. We believe these therapies will be best positioned to receive attractive reimbursement, regardless of the political or economic environment.

Industrials & Materials

Industrials & Materials

Manufacturing Activity Slows

The U.S.-China trade war continues to create volatility for industrials. It has also weighed on PMIs, which now indicate that manufacturing activity is contracting in most major economies. As a result, we’ve seen investors rotate into so-called defensive industrials (firms that have limited exposure to slowing end markets), driving up valuations. The momentum could reverse, however, should a trade deal be struck and capital expenditures start to rebound – a distinct possibility as the 2020 U.S. presidential election approaches and the political will to keep the economic expansion going becomes stronger. Lower borrowing costs, helped by the Federal Reserve’s recent rate cuts, could also incentivize businesses to spend and boost manufacturing activity.

Investment Implications

Our general view is the U.S. economy could deliver moderate growth in the near term, especially if a trade deal is reached. But we are mindful of valuations and the uncertain economic outlook. As such, we are focused on finding companies with organic growth drivers – for example, firms that are using technology to improve their product offerings or realizing efficiencies through mergers and acquisitions – but whose stocks have sold off because the business is viewed as cyclical. At the same time, we also favor defensive firms such as paint manufacturers and metal-packaging makers that tend to hold up well during a slowdown but whose stocks have not been pushed to excessive valuations. Finally, we continue to prioritize strong management teams, which we believe are essential to a company’s ability to deliver positive results.

Technology

Technology

Pockets of Optimism Emerge

Trade tensions between the U.S. and China remained front and center during much of the third quarter, creating an overhang for members of the tech supply chain. At the same time, merger-and-acquisition activity has declined on increased regulatory oversight of internet platforms while initial public offerings have faced scrutiny because of lofty valuations. However, the delay of some tariffs and the absence of further escalation in the trade war raised hopes that a trade deal might be closer. At the same time, cyclical headwinds, such as excess memory and chip inventories, have started to ease. Combined, these trends helped to lift stocks of semiconductors, a key part of the tech supply chain; flash memory and DRAM manufacturers, which are beginning to benefit from improved weekly pricing; and data center providers, as spending on the technology is showing signs of renewed life after significant slowing over the last year.

Investment Implications

Despite quarter-to-quarter fluctuations, the longer-term secular themes we have identified within the space remain intact. These themes include the growth of cloud computing, increased adoption of Software as a Service and advances in artificial intelligence and the Internet of Things. We continue to remain acutely aware of valuations. While multiples of high-growth, small-cap software firms still appear stretched to us, some valuations have come back in as of late. Furthermore, we believe some large-cap software names remain reasonably valued.

Download a PDF of the 3Q Global Sector Views here.

CONTRIBUTORS

-

Carmel Corbett Wellso

Carmel Corbett Wellso

Outgoing Director of Research

-

Andy Acker, CFA

Andy Acker, CFA

Global Life Sciences | Portfolio Manager

-

Noah Barrett, CFA

Noah Barrett, CFA

Research Analyst

-

Jon Bathgate, CFA

Jon Bathgate, CFA

Research Analyst

-

David Chung, CFA

David Chung, CFA

Research Analyst | Assistant Portfolio Manager

-

Joshua Cummings, CFA

Joshua Cummings, CFA

Research Analyst

-

John Jordan

John Jordan

Portfolio Manager | Research Analyst

-

Daniel Lyons, PhD, CFA

Daniel Lyons, PhD, CFA

Portfolio Manager | Research Analyst

FEATURED FUNDS

JRAIX

Research Fund

By investing in the best ideas from each global research team, this U.S. large-cap growth fund seeks long-term growth of capital with volatility similar to its peers.

View ProductJWWFX

Global Research Fund

A large-cap growth portfolio that leverages the best ideas and expertise of our global research sector team.

View Product

JNRFX

Research Fund

By investing in the best ideas from each global research team, this U.S. large-cap growth fund seeks long-term growth of capital with volatility similar to its peers.

View ProductJANWX

Global Research Fund

A large-cap growth portfolio that leverages the best ideas and expertise of our global research sector team.

View Product