Commodities have faced a protracted period of uncertainty since the global financial crisis. But with multiple structural tailwinds and the risk of inflation making headlines, portfolio managers Mathew Kaleel, Andrew Kaleel and Maya Perone ask: is it time to reconsider their use as a valuable portfolio diversifier?

Key Takeaways

- A more persistent inflationary regime would be structurally detrimental to traditional equity/bond portfolios, eating into corporate margins and impacting nominal bond yields.

- An allocation to commodities may help to mitigate the impact of any inflationary trends or spikes, particularly in an environment where there are both supply constraints and persistent and robust demand.

- Despite calls of a new commodity ‘super cycle’, we would at this point characterise recent commodity price changes as a reversion to what we would consider fair value, relative to global equities.

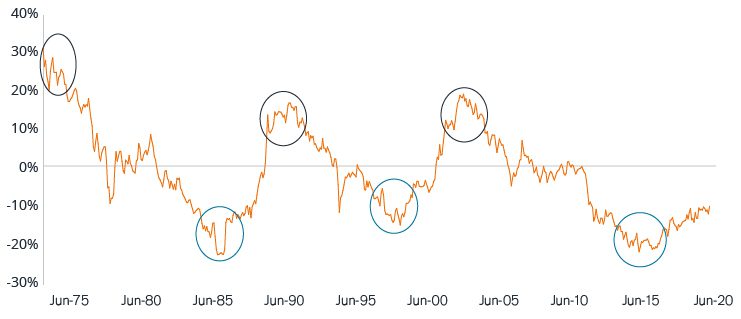

Observation 1: Commodities in a cyclical perspective

Commodities have well-defined cycles over time, and this is particularly evident when looking at the returns of commodities relative to other growth assets. The measure that we use to highlight the cyclical nature of commodity markets is by comparing rolling five-year annualised returns of global stocks and commodities (Exhibit 1). The series has historically fluctuated between periods of over and undervaluation of commodities as an asset class relative to global equities. This is best explained by the underinvestment in commodity markets that establishes a cyclical low during downturns, and eventual oversupply at the end of a cycle.

Exhibit 1: Commodities (BCOM) versus MSCI World Index

Source: Janus Henderson Investors, Morningstar, 1 January 1975 to 31 December 2020, showing rolling five-year annualised excess returns for commodities versus the MSCI World Index.

Note: Stocks are represented by the MSCI World Net Total Return USD Index, Commodities are represented by the GSCI from January 1975 to December 1990 and the BCOM Commodity Index from January 1991. Past performance is not a guide to future performance.

While we have seen a pickup in the calls of a new commodity ‘super cycle’ in the first half of 2021, we would instead characterise the recent increase in commodity markets as a longer-term reversion to what we would consider ‘fair value’ relative to global equities. Whether this is the start of a super cycle or not is less relevant than the simple fact that, should history be any guide, this current cycle of commodities outperforming global stocks may persist for several years. This, in our view, provides an attractive option for investors seeking to diversify portfolios and protect against an outbreak of commodity price inflation.

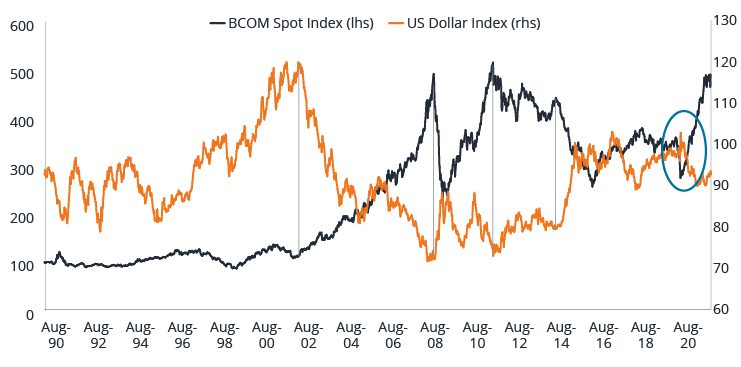

Observation 2: The relationship between the US dollar and commodities

A second consideration when looking at the future path of commodity markets is longer-term cycles in the US dollar, in which all major commodities are still traded. This relationship is a direct one; spot prices for commodities tend to rise in periods of relative weakness in the US dollar as those commodities are cheaper in local currency terms. This long-term inverse relationship is highlighted in Exhibit 2, with the most recent base in commodity markets occurring in March 2020. From that base, commodity markets have rallied in conjunction with a correction in the US dollar.

Exhibit 2: The US Dollar/Commodity cycle

Source: Janus Henderson, Bloomberg as at 31 December 2020.

Note: The Bloomberg Commodity Spot Index (BCOMSP – shown on the left-hand axis) tracks prices of futures contracts on physical commodities on the commodity markets. ICE’s US Dollar Index (shown on the right-hand axis) measures the value of the United States dollar relative to a basket of foreign currencies (the euro, Japanese yen, sterling, Canadian dollar, Swedish krona and Swiss franc). Past performance is not a guide to future performance.

As with commodity markets, cycles in the US dollar tend to take a number of years to play out; if the absolute base for commodity markets in this cycle was March 2020, a persistent weakening of the US dollar would provide a broadly positive tailwind for commodity markets.

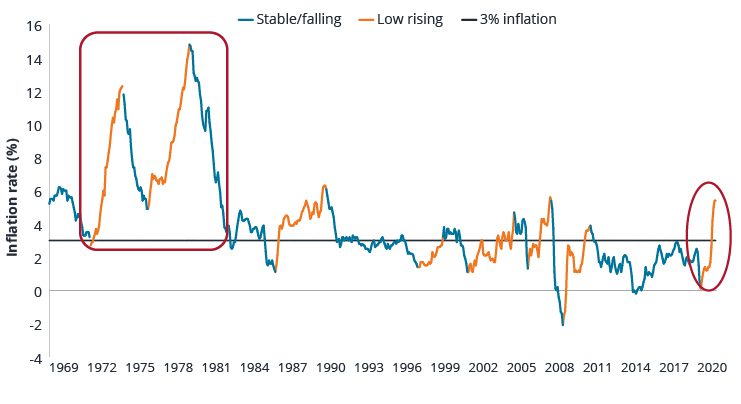

Observation 3: Inflation is only an issue if it is persistent

Commodity markets and wage prices are two of the key inputs that determine the rate of change and level of inflation. While transitory impacts can be mitigated, more persistent regimes of low/rising, or high/stable inflation are detrimental to traditional equity/bond portfolios, eating into corporate margins and impacting nominal bond yields. There has been only one meaningful period of persistently elevated inflation in the last fifty years, measured as levels above 3% year-on-year (yoy), which was in the 1970s (Exhibit 3).

Exhibit 3: US CPI urban consumers (yoy) inflation (%)

Source: Bloomberg, Janus Henderson Investors, March 1969 to July 2021. Past performance is not a guide to future performance.

Whilst not the baseline assumption, a combination of higher wages and commodity price pressures occurring simultaneously would create significant headwinds for traditional portfolios and would argue for the inclusion of commodities as both a diversifier and inflation hedge.

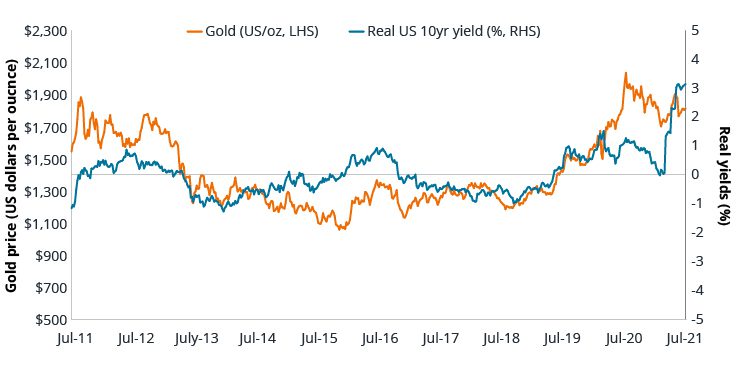

Observation 4: Gold prices are more a reflection of investors hunting real yields than inflation

Gold prices typically provide an insight into real yields and the protection of capital, which gives us a snapshot of both inflation and nominal yields (Exhibit 4). We expect gold to continue to provide synthetic portfolio insurance against an unexpected collapse in real yields, whether as a result of changes in nominal yields and/or inflation.

Exhibit 4: Gold prices vs real yields

Source: Bloomberg, Janus Henderson Investors, July 2011 to May 2021. Past performance is not a guide to future performance.

Observation 5: A structural change in oil and natural gas market dynamics

Prices for crude and refined petroleum products have rallied from the lows in March 2020; however, the potential for further price appreciation remains. The lack of recovery in US onshore oil rigs and supply discipline by OPEC+ has led to a normalisation in US petroleum inventories relative to the five-year average. The combination of ongoing supply discipline by OPEC+ and the dearth of investment going into new oil development, partly due to environmental, social & governance (ESG) considerations, could very well see a significantly tighter oil market in the months ahead and into 2022. This also has significant implications for the natural gas markets, both in the United States and globally, as a once oversupplied gas market swings into an environment of supply constraints and potentially structural deficits in inventory levels. These factors, alongside wage or food price inflation, could materially impact year-on-year inflation outcomes.

The sensitivity of commodity markets to inflation can benefit investors

Commodity prices are both a reflection and driver of changes in interest rates and inflation. Outside of the key factor of changes in wage expectations, a bullish commodity market cycle is intrinsically inflationary, particularly in environments where there are both supply constraints and persistent and robust demand. In our opinion, the current environment suggests we are potentially in such an environment. The incorporation of ESG factors into investment decisions across all industries, in combination with a push to build out a global renewable industrial complex, provides a multi-year demand push and also imposes supply constraints in energy.

Central banks have also collectively moved from a policy of inflation targeting toward one that is comfortable with higher levels of sustained inflation. In its release to the market on 17 March 2021, the US Federal Reserve articulated this objective:

…the [FOMC] Committee will aim to achieve inflation moderately above 2 per cent for some time so that inflation averages 2 per cent over time and longer‑term inflation expectations remain well anchored at 2 per cent.

This policy, echoed by other major central banks, can be understood as a desire for global central banks to achieve higher sustained levels of price inflation. While short-term rates have remained near-zero bound, the change in central bank policy has led to increases in long-term rates and inflationary expectations.

A repricing of longer-term interest rates affects portfolios sensitive to equity and bond market beta, particularly if it leads to a sustained period of higher inflationary outcomes, as was the case in the 1970s. This raises the question of how various asset classes might perform, and how investors might respond. While the commodity bear cycle that followed the Global Financial Crisis of 2007-2008 was longer than average, an allocation to commodities could represent an interesting opportunity for investors, in terms of growth potential, portfolio diversification and as a potential hedge against the effects of inflation.

View All Perspectives