Subscribe

Sign up for timely perspectives delivered to your inbox.

Converging trends are creating the perfect storm for further disruption in the technology sector. Richard Clode, Global Technology Portfolio Manager, comments on the opportunities that may lie ahead and how to avoid the potential pitfalls that the associated hype may bring.

Technology is never a quiet sector and this year is no exception with crescendos of noise around regulation and protectionism in particular. Technology stocks have continued to outperform the broader equity market and Apple and Amazon hit the headlines in recent weeks as the first publicly-listed US companies to reach $1 trillion in market value. But what is the outlook for the technology sector from here?

Technology disruption is accelerating. A powerful convergence of technology trends is occurring. Half the world is now online and mobile, meaning more consumers are accessible, while rapid advances in digital payments have enabled the monetisation of online services. In many emerging markets, consumers are learning to pay with their smartphones before they even have a credit card and China is fast becoming a cashless society.

[caption id=”attachment_67241″ align=”alignright” width=”300″] iStock[/caption]

iStock[/caption]

Leveraging these important foundations are the new trends of the cloud and artificial intelligence. The cloud democratises technology by collapsing the cost of computing and enabling anyone to access cloud services anywhere, at any time and at very low cost. The likes of Amazon and Alibaba are fostering the next generation of technology companies built entirely in the cloud, such as Netflix and Spotify. Artificial intelligence has also finally reached an inflection point. The rapid deflation of computing power – driven by Moore’s Law* and the cloud – allows for deep learning and neural networks on a scale that was impossible only a few years ago. The cost of the analysis of data is declining dramatically and, as a result, we are witnessing breakthroughs in areas like image and natural language processing, for example Amazon Alexa.

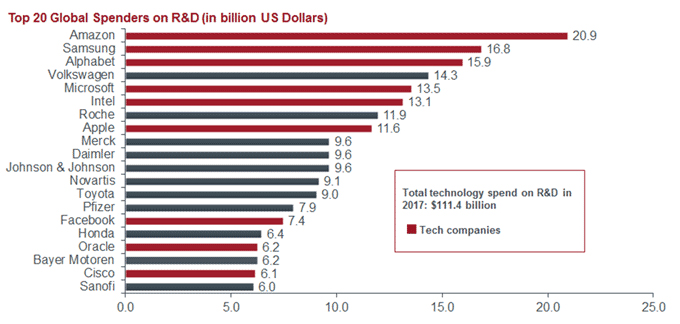

In contrast to the past, these technologies are rapidly evolving into commercial products as they can be disseminated faster than ever before given the groundwork laid by global internet penetration, the cloud and payment digitisation. This creates a virtuous circle for technology companies that can monetise new technologies at a similarly accelerated pace, which enables profits to be reinvested in rapidly evolving innovation. Of the top 20 global spenders on research and development (R&D), nine are technology companies, including the top three, as shown in the chart below. Those nine technology companies alone spend $111bn on research and development a year, funded by the vast profits they generate from their ongoing innovation, creating technology products and services that consumers want to buy.

Source: Janus Henderson Investors, Bloomberg, as at 31 December 2017[/caption]

Source: Janus Henderson Investors, Bloomberg, as at 31 December 2017[/caption]

This technology convergence and sheer scale of innovation will result in an accelerating and broadening disruption of more industries. We are already seeing a huge amount of disruption in the automotive industry as electric vehicles, ride hailing and autonomous driving take off. For a century, automotive companies have built their franchises on designing internal combustion engines and operating massively complicated production plants. They are now having to adapt to a not too distant future of much more simplified cars built around electric motors and a battery, as well as having to learn to programme algorithms to drive the car and designing apps to hail a ride. Automotive companies will need to become technology companies to compete with new disruptive entrants like Tesla, Uber and Waymo. The world’s first commercial autonomous robotaxi platform is expected to be launched by Alphabet’s autonomous driving division in the US, Waymo, later this year.

One of the world’s more highly valued unicorns** is Ant Financial, Alibaba’s online financial services affiliate. Ant recently raised $14bn at a $150bn valuation making it one of the most highly valued financial services companies in the world, overtaking even Goldman Sachs and BlackRock. Ant Financial was able to entice global investors at that valuation because the company had already disrupted the Chinese financial industry and – via its investment in Paytm – is well on the way to repeating this in India. The thought of 2.5 billion people accessing financial services via their smartphones, disintermediating physical banks, is a frightening prospect.

Exciting disruptive technology will inevitably lead to hype. How should investors aim to protect themselves? It is reassuring that while there are some very expensive technology companies, the sector is bifurcated, containing some of the cheapest stocks in the market as well. Consequently, the technology sector in aggregate only trades at a modest premium to the overall market so good opportunities at attractive valuations are still plentiful. Avoiding overhyped areas of technology is the key to sustainable, less volatile returns and Janus Henderson’s Global Technology franchise is built on a long-standing investment process of ‘navigating the hype cycle’. This involves identifying and understanding where an emerging technology is on the hype cycle (phases of hype, adoption, maturity and social application).

What are the other risks? With a highly sophisticated global supply chain, the technology industry is exposed to recent trade tensions but the symbiotic nature of technology trade patterns makes it a hard industry to target. iPhones are: ‘Designed by Apple in California. Assembled in China.’ A similar paradox is evident in regulation; consumers want more personalised services but, at the same time, more data privacy. Google has seen an increase of more than 900% in the past two years in search queries containing ‘near me’. The recent implementation of the General Data Protection Regulation (GDPR) in the European Union is evidence that a middle ground can be found.

With European markets structurally underweight technology, investors are betting on the disrupted: we believe that investing in technology is investing in the disruptors.

*Moore’s Law predicts that the number of transistors that can fit onto a chip (integrated circuit) will roughly double every two years, therefore decreasing the relative cost.

**A unicorn, in investment terms, is a startup company with a valuation of more than $1 billion.