Subscribe

Sign up for timely perspectives delivered to your inbox.

The Portfolio Construction and Strategy Team explain why investors should consider a dedicated allocation to healthcare, which has historically captured less downside during market sell-offs.

Given the market volatility of 2022 and a slowing world economy, it is understandable that investors might want to tread carefully. Yet, such periods can uncover attractive investment opportunities, including assets with both defensive characteristics and growth potential. From a portfolio construction point of view, this translates into investments that can provide uncorrelated returns and help protect against drawdowns.

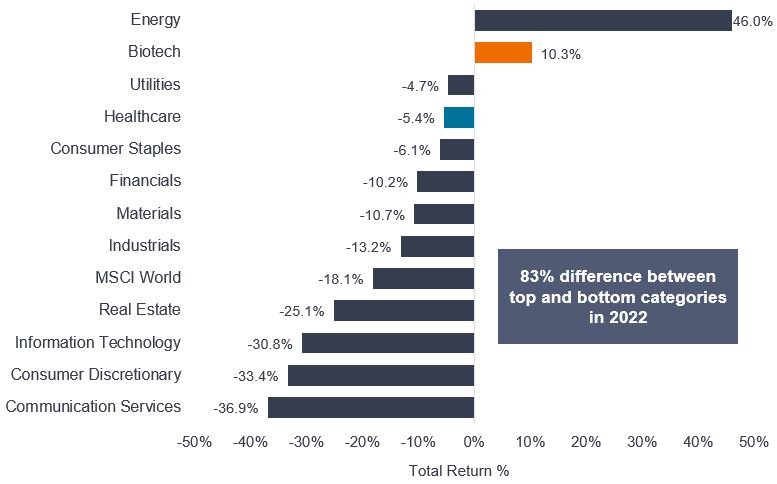

To that end, we believe investors could benefit from an allocation to healthcare. The sector has historically captured less downside during market sell-offs, and also benefits from structural tailwinds such as aging populations and rapid innovation. In 2022, for example, most global equity sectors experienced material losses (see Exhibit 1), yet healthcare broadly and the biotech subsector specifically were more insulated from the pain.

The question from a portfolio construction perspective is, why was that the case, and can we expect similar characteristics going forward?

Source: Morningstar, global equity sectors and subsectors based on MSCI World Index, as at 31 December 2022. Past performance does not predict future returns.

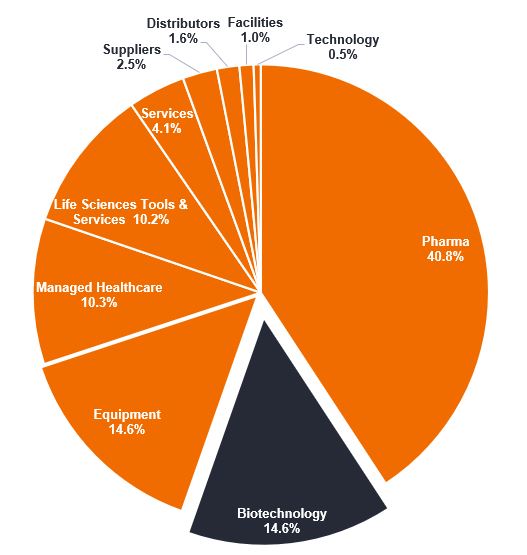

Healthcare has traditionally been an effective portfolio buffer during periods of volatility due to steady consumer demand for hospitals, medicines, and medical devices irrespective of market conditions. This is true for approximately 85% of the sector, which is made up of pharmaceuticals, medical devices, and health care services, all of which reflect the “defensive” characteristic we mentioned earlier.

The remaining 15% of the sector is made up of biotechnology firms. This subsector includes innovative – and inherently volatile – small- and mid-cap firms that offer greater growth potential, as well as large-cap firms that reflect more defensive qualities and tend to behave similarly to traditional pharmaceutical companies.

Source: MSCI, composition of the MSCI World Health Care Index as at 31 December 2022.

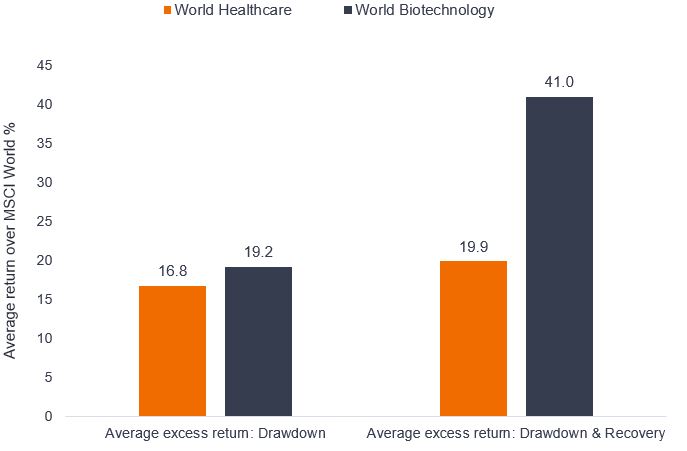

These defensive and growth characteristics are reflected in historical returns. Exhibit 3 shows the performance of the healthcare sector and biotechnology subsector relative to global equities (excess return) during the past five market drawdowns and subsequent recoveries. While we would expect healthcare to outperform across the full cycle of drawdown and recovery due to its defensive nature, biotech has ultimately shown better performance, highlighting its capacity for alpha generation.

Source: Morningstar. Global equity sectors and subsectors based on MSCI World Index. Average of downturn periods are 1/4/00 – 9/10/02, 1/11/07 – 9/3/09, 3/5/11 – 4/10/11, 13/2/20 – 23/3/20, 5/1/22 – 12/10/22. Recovery periods are based on MSCI World, for the final period 31/12/22 in the case of the recent recovery. *Last market downturn period recovery and full cycle end date is as at 12 December 2022. Past performance does not predict future returns.

It is estimated that 90% of drugs that enter human clinical trials never make it to market, and for those that do, our experience shows that consensus sales estimates for new drug launches are wrong 90% of the time.1 Therefore, expert knowledge and understanding of the scientific research, testing, and drug approval process, plus a skilful assessment of the related commercial opportunities, is critical to identifying winners that can take advantage of the speed of innovation happening in the sector.

At the same time, the market drawdown in 2022 caused a rerating of price-to-earnings ratios for healthcare stocks, with ratios dropping precipitously from recent highs. This rerating was particularly pronounced in the small- and mid-cap biotech space. In fact, roughly 200 of these companies now trade below the levels of cash on their balance sheets,2creating the opportunity for idiosyncratic events (e.g., positive clinical trial updates) to drive significant upside.

Therefore, we think an active and nimble approach is key to finding those companies that stand to benefit from the many long-term tailwinds that healthcare and biotech can provide, as well as uncovering opportunities borne out of market inefficiencies.

1 American Society for Clinical Pharmacology & Therapeutics, “Probability of Success in Drug Development,” van der Graaf, Piet H., 19 April 2022.

2 Rapport Biotech Insight & Opinion, as of 3 January 2023.

MSCI World Index℠ reflects the equity market performance of global developed markets.

MSCI World Health Care Index℠ reflects the performance of health care stocks from global developed markets.

Alpha is measure that can help determine whether an actively-managed portfolio has added value in relation to risk taken relative to a benchmark index, and is the difference between a portfolio’s return and its benchmark’s return after adjusting for the level of risk taken. Alpha generation indicates that a manager has added value.

Balance sheet is a financial statement that summarises a company’s assets, liabilities and shareholders’ equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders. It is called a balance sheet because of the accounting equation: assets = liabilities + shareholders’ equity.

Drawdown is the difference between the highest and lowest price of a portfolio or security during a specific period. It can help evaluate an investment’s possible reward to its risk.

Price-to-earnings ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

Reratings occur when investors are willing to pay a higher price for shares, usually in anticipation of higher future earnings. In terms of bonds a re-rating can be assigned when the bond issuer’s ability to service and repay its debt improves (credit quality).

Important information

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Health care industries are subject to government regulation and reimbursement rates, as well as government approval of products and services, which could have a significant effect on price and availability, and can be significantly affected by rapid obsolescence and patent expirations.

Smaller capitalization securities may be less stable and more susceptible to adverse developments, and may be more volatile and less liquid than larger capitalization securities.

Volatility measures risk using the dispersion of returns for a given investment.

Sign up for timely perspectives delivered to your inbox.