Subscribe

Sign up for timely perspectives delivered to your inbox.

Portfolio Manager Stephen Payne considers the factors that could turn UK bonds and equities from long-term unloved to a strategic choice for investors.

In what may be a masterclass in understatement, it has been a very tough year to date for risk assets in the UK. The falls seen in gilt markets are unprecedented, sterling weakness has garnered consistent headlines, and weakness in the stock market has been significant. Recent sentiment has seen further deterioration. Investors’ confidence was rattled by the scale and focus of the government’s planned tax cuts announced in Chancellor Kwarteng’s mini budget on 23 September.

The rise in government borrowing costs precipitated fears of a potential crisis for the liability-driven investment (LDI) market, with significant consequences for UK pension schemes. The Bank of England intervened with an emergency bond-buying programme to prevent a ‘material risk’ to the financial stability of the UK, as concerns grew that some pension schemes might be forced to sell assets to raise collateral.

Markets now have a feel of capitulation about them. While the past few weeks have been painful, the important point to keep in mind is that it is behind us. Negative investor sentiment reflects this rear-view mirror perspective, whereas that period of market weakness provides a much better starting point for returns going forward.

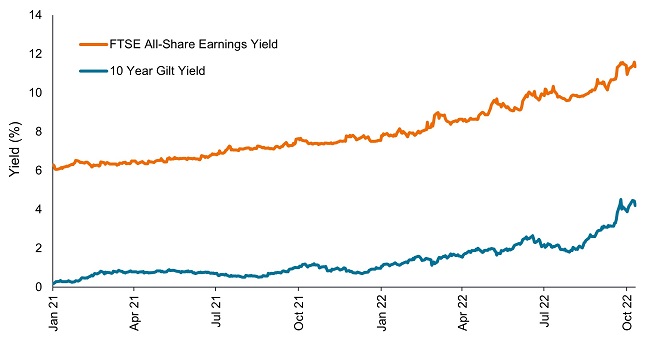

Before the start of 2022, the single biggest problem for markets, in terms of return prospects, was that bond yields were unsustainably low. This restricted the yield and hence limited the potential returns on offer from bonds. At the same time, it inflated equity valuations. The government bond yield or “risk-free rate” is the key determinant of the discount rate applied to future cash flows to calculate the equity valuation of a business. The profile of bond yields has changed dramatically. Yields on 10-year gilts are over 4% at the time of writing, whereas they began the year just under 1% (Exhibit 1). Credit spreads have also widened, and high-quality investment grade corporate bonds are now available offering yields above 6%. With such relative riches on offer, the prospect for fixed income returns going forward has drastically improved.

Source: Refinitiv Datastream, 14 October 2020 to 14 October 2022. Past performance does not predict future returns. Yields may vary over time and are not guaranteed.

This adjustment in bond yields is also a boon for future potential equity returns. The UK equity market has de-rated much more than most, with a PE ratio of 9x earnings well below the 30-year average of 13.5x earnings. The dividend yield on offer has risen, with the potential for additional dividend growth to boost total return. Within the UK equity market, mid- and small-cap stocks have particularly suffered this year – the FTSE 250 Mid-Cap Index is down 29% year to date, to 12 October 2022. As always, the price you pay is the ultimate determinant of returns over the long term. As doom and gloom pervades, we would argue that now could be the time to be excited, with what may prove to be some outstanding opportunities for astute investors.

While we are not blind to the worries that blight global sentiment, our view is that the current profile of the UK market encourages a more optimistic view of long-term prospects. In the US, the Federal Reserve’s (Fed’s) hawkish rhetoric is focused on the lagging indicator for inflation, the labour market. US consumer inflation expectations are moderating, and oil and other commodity prices have fallen. Inflation indications, such as the consumer price index (CPI), are expected to fall in the coming months – could a Fed pivot be on the cards?

This view may seem a little too optimistic. But while a recession looks likely, we think that much of the risk is already in the price. Many investors are anchored to their experience of the last two recessions, the global financial crisis (GFC) and COVID – two extraordinary events where the economic contraction far exceeded any normal recession.

We have experienced various downturns over the years, and to see a recession discounted so quickly in share prices is, to us, unprecedented. Normally the nadir is reached well into the earnings forecast downgrade cycle; this time we are there with the downgrades only just beginning. This could make for an uncomfortable few months as any downgrades come through, but we would argue that market weakness could offer judicious entry points to capture the recovery upside. It is important to be selective, being wary of structural changes and the burden of too much debt. However, with credit spreads approaching levels seen in previous recessions, and many cyclical names looking heavily discounted, this could be an opportunity to put money to work across both equities and bonds.

Sign up for timely perspectives delivered to your inbox.