Subscribe

Sign up for timely perspectives delivered to your inbox.

Global Bonds Portfolio Manager Bethany Payne reflects on the market’s sharply negative reaction to the UK government's tax-cutting mini-budget and its potential consequences.

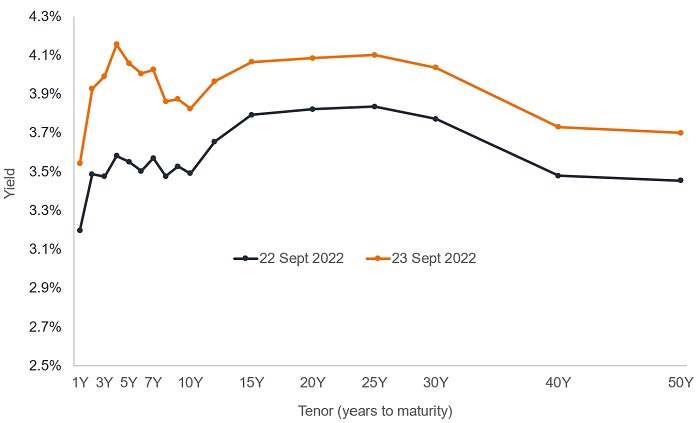

In its mini-budget announcement, the UK government was seeking to manufacture impressive growth levels, funded by heavy borrowing and tax cuts. Yet for the UK chancellor Kwasi Kwarteng, Friday 23 September may be a day he prefers to forget. It is doubtful it was the chancellor’s intention to add 50 basis points (bp) to the yield on UK 5-year government bonds, but such was the market’s fears about the scale of new gilt issuance that this was the result within an hour of him finishing delivering the mini-budget in parliament.1

Figure 1: Dramatic one day rise in UK gilt yield curve

Source: Bloomberg, GBP UK sovereign yield curve, 23 September 2022.

Wherever you looked across UK gilt markets, the story was the same. Yields rose across the board: the short end of the yield curve took the most pain but even yields on longer dated bonds rose sharply. Sterling came under similar stress, dropping from US$1.13 to US$1.09 against the US dollar, some distance from the US$1.35 it began 2022.2

While the UK government did not allow the Office for Budget Responsibility (OBR) initially to cost the fiscal event (although the OBR has been commissioned to report on 23 November 2022), the market did send their reaction loud and clear: investors have little faith in the government’s approach.

Already, over the first eight months of this year, local currency (sterling) gilt returns were bad (-19.5%), but in US dollar terms, gilts (-30.9%) have been the worst performing asset of all the major asset classes.3 With the sharp rise in gilt yields in September and a further fall in sterling the figures are likely to be worse still by the end of September.

There is a lot of funding through gilt issuance to do in the coming months and next year. This begs the question about who will sponsor gilts going forward. Relying on the kindness of strangers may only stretch so far because according to BoE data, overseas buyers deserted the UK in July, effectively reporting the largest ever monthly net sales (-£16.6 billion) by this sector, matched only by a one-off event in 2018.4

Concern around UK government borrowing was heightened earlier by its energy price cap proposals. The government expects the energy price cap to cost around £60bn for six months, but there is a catch: it involves a potentially very expensive bet on energy prices. The UK government has effectively entered into a short position in gas and electricity wholesale markets without a hedge – that is a naked short. This ties UK gilt yields to energy markets.

Moreover, the fiscal loosening within the budget runs counter to the BoE’s monetary tightening and its attempts to slow inflation.

The BoE sought to reassure markets that it preferred to assess the impact of the chancellor’s new strategy rather than engage in an emergency rate rise. It is not inconceivable, however, that we could see an inter-meeting hike from the BoE if sterling continues to depreciate, given that the next scheduled meeting for a rate hike decision is not until November. We had three dissenters wanting a 75bp hike at the September meeting the day before the mini-budget. If they had had the budget announcements to hand, it is likely, in our opinion, that they would have hiked more aggressively. We have raised our forecast for the next meeting to a 75bp hike*, with a risk to more if we see sterling continue to depreciate.

*Forecasts are estimates, may vary over time and are not guaranteed.

Added to that is growing speculation about what will happen with the BoE holdings of gilts, bought as part of its Asset Purchase Facility (APF) interventions. Rising bond yields mean that these have also lost a significant amount of value, with the loss on the long basket of gilts (those dated 15 years or more) reaching 42%.

| Maturity of APF holdings | Loss |

|---|---|

| 0-3 years | -11% |

| 3-7 years | -17% |

| 7-15 years | -24% |

| 15+ years | -42% |

| Total % | -23% |

| Total £ | -220 billion |

Source: Janus Henderson calculations, Bank of England, Bloomberg, 26 September 2022. These calculations are estimates, may vary over time with market movements and are not guaranteed.

These severe losses raise concerns for us – is there a threshold at which the BoE becomes mindful of crystallising these losses at a cost to the taxpayer?

APF losses are indemnified by the UK Treasury, i.e. any financial losses are borne by the Treasury but any gains are owed to the Treasury. Around £120bn has been transferred to the Treasury from the APF as the coupon on gilts held is higher than the Bank Rate.5

But as Bank Rate is now higher than the coupon on gilts and the bank moves to crystallise losses across their portfolio due to quantitative tightening (QT), whereby the Bank actively sells gilts from the APF, transfers will have to be made in the opposite direction – from the Treasury to the BoE. This is going to be politically unpalatable and may even trigger a need for further gilt issuance.

Could we therefore be talking about tapering (reducing) quantitative tightening (QT) relatively soon or even cancelling QT before it has properly started?

The policies announced in the mini-budget inject major discretionary fiscal stimulus into possibly the tightest UK labour market on record, with unemployment at a near fifty year low and the job vacancy rate at a record high.6 We see debt-to-gross domestic product on a rising trajectory in the medium-term. In our view, the mini-budget package represents a material increase in risks: to inflation; to Bank Rate; and to the currency.

Footnotes

1 Source: Bloomberg, intraday figures, yield on 5-year UK government bond, 23 September 2022.

2 Source: Bloomberg, GBPUSD currency exchange rate, 23 September 2022.

3 Source: Deutsche Bank, August Performance Report, iBoxx £ Gilts Index, total returns between 31 December 2021 and 31 August 2022, 1 September 2022.

4 Source: Bank of England, Bloomberg, foreign net gilt buying, 31 August 2022

5 Source: Bank of England, ‘QE at the Bank of England: a perspective on its functioning and effectiveness’, 18 May 2022.

6 Source: Refinitiv Datastream, UK labour force survey, unemployment rate; UK vacancy ratio, 31 July 1971 to 31 July 2022.

GC 0922-120635 03-31-24 TL