Subscribe

Sign up for timely perspectives delivered to your inbox.

Global Head of Asset Allocation Ash Alankar explains why markets are putting themselves in peril by minimizing the tail risk of runaway inflation and need for higher interest rates.

The Federal Reserve (Fed) has thus far lived up to its word by aggressively raising interest rates, and markets have noticed – but perhaps not in the manner many would have expected. Since June, the S&P 500® Index has climbed 17% and the yield on the 10-year U.S. Treasury note has fallen roughly 60 basis points (bps) to 2.87%. Even the upward march of the 2-year note’s yield, which tends to reflect the market’s shorter-term expectations for the federal funds rate, has stalled. These developments indicate that investors believe the U.S. central bank has a decent shot at sticking a soft landing. We think that confidence is misplaced.

Reinforcing the market’s positive assessment are prices in forward-looking futures and options markets. These are instruments that investors could use to mitigate against downside risk. At present they are flashing green. We find this concerning given the breadth of risks facing the global economy and financial markets. Foremost, there is inflation, which is at generational highs. Not to be overlooked are the war in Ukraine, rolling COVID-19 related lockdowns in China and continued labor shortages.

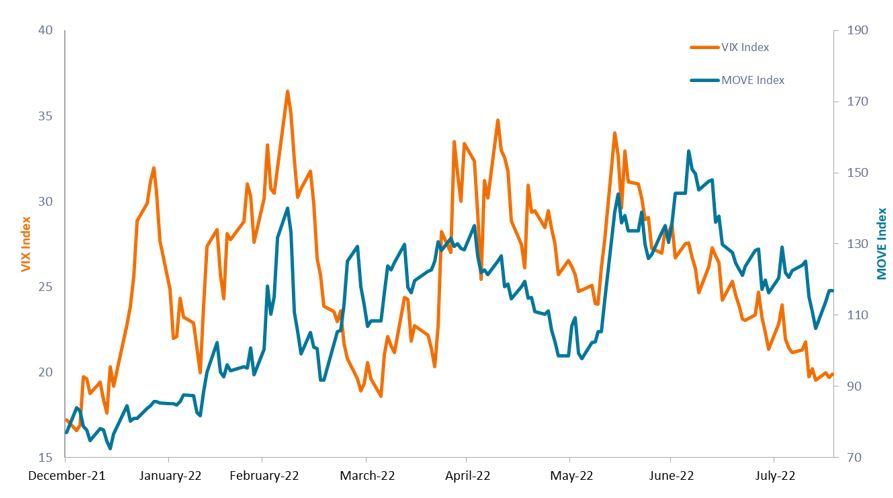

Year-to-date equities and bond market volatility

Over the past two months, options markets reflect investors’ view that downside risk to both equities and bonds is subsiding.

Source: Bloomberg, as of 18 August 2022.

As seen above, the volatility implied in the Cboe VIX Index and the ICE Bank of America MOVE Index signals that investors see diminishing downside risk to both U.S. equities and Treasuries. The VIX has already dipped beneath its 5-year average and the MOVE is nearly 25% beneath its June peak. History tells us that when complacency is high, the likelihood of tail-risks increases as investors view the economy through rose-colored glasses. As we’ve often stated, tail-risks are the outlier moves that tend to hold great sway over long-term investment performance; they are not to be ignored. And given the aforementioned risks, at present, there is plenty to keep one’s eye on.

After having been asleep at the wheel for much of 2021 as inflation accelerated, the Fed got serious earlier this year, initiating a succession of rate hikes that now add up to 225 bps. The futures market expects an additional 100 bps of increases by the end of 2022. Given inflation’s ferocity, this aggressiveness is welcome, but it’s too early to take a victory lap. Monetary policy tends to have a lagging effect, and this bout of inflation has both demand-side and supply-side sources, with the latter being less responsive to rate hikes. Furthermore, many market participants were not even alive the last time U.S. inflation was this rampant, meaning there is the risk they are underestimating the challenge faced by the Fed.

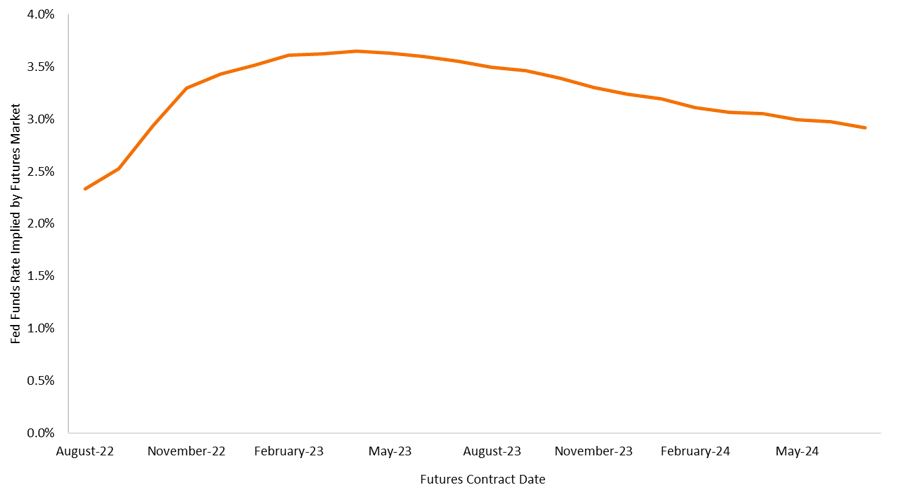

Futures-implied federal funds rate

The futures market sees the Fed pausing rate hikes by next spring and even reducing them during the summer.

Source: Bloomberg, as of 18 August 2022.

Futures contracts that reflect market expectations for the trajectory of the federal funds rate see the Fed pausing by May 2023 and policy actually beginning to ease two months later. Should that scenario transpire, we believe that the Fed would be in peril of repeating its mistakes of the 1970s and 1980s by prematurely declaring victory over inflation. Both Fed Chairs Arthur Burns and eventual inflation hero Paul Volcker learned this lesson the hard way as blinking at early signs of economic softness before the battle had been won resulted in inflation reemerging and becoming more imbedded in consumer expectations. This vacillation almost guaranteed higher doses of growth-sapping hawkishness down the road.

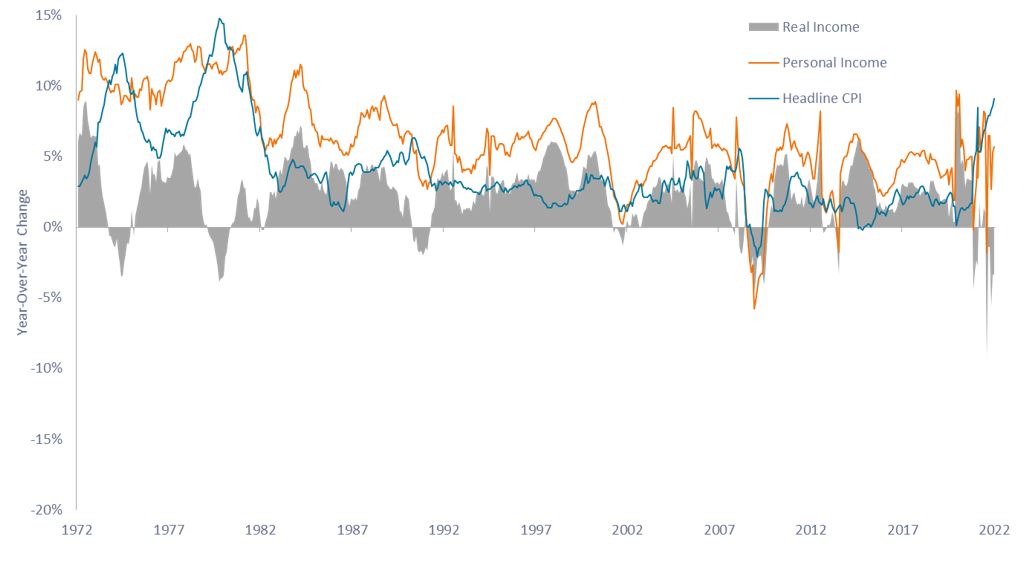

Our fears that taming inflation will be a much taller task than many anticipate is premised on the glaring gap between nominal wage growth and inflation.

Difference between year-over-year wage growth and inflation

The diminished purchasing power brought on by negative wage growth puts the economy at risk of a wage-price spiral as workers demand higher pay.

Source: Bloomberg, as of 18 August 2022.

Source: Bloomberg, as of 18 August 2022.

As illustrated above, only rarely in the past four decades has the gap between headline inflation and gains in personal income been so great. This represents an alarming level of negative real income growth and is perhaps the most sensitive tripwire that the Fed must account for. Faced with diminishing purchasing power, workers demand higher pay. Given the degree to which labor comprises business expenses in a service-based economy like the U.S., the presence of this gap places the economy on the dangerous path toward a wage-price spiral.

When confronting painfully negative real wage growth, only two solutions exist. One is that labor demands higher wages. Higher pay, however, leads to rising prices as companies seek to finance wage growth. Once this cycle takes hold, the wage-price spiral is in full effect. This is not the good kind of inflation indicative of a healthy economy, but rather is a nightmare scenario for central banks. The only way to stop it is to choke the economy to a standstill through drastically constrictive policy. This all but eliminates the possibility of a soft landing as breaking the spiral requires a very high escape velocity defined by draconian interest rates.

Alternatively, the Fed can live up to its rhetoric and do what it takes to tame inflation. This entails not switching course at the first signs of demand destruction. While this path increases the likelihood of recession, it would be neither as deep nor dire as what would be needed to break a wage-price spiral. A race is now occurring between how fast the Fed can deploy monetary tightening to tame inflation versus how quickly labor demands higher wages. Given it is pricing in a policy reversal in mid-2023, the market doesn’t appear to appreciate the importance that the race must be won by the Fed. If not, all that’s been done thus far to reel in inflation will have been wasted. Fed Chairman Jay Powell has reiterated that the Fed is data dependent. That not only means observing current data but also acknowledging lessons of the past, namely the risk of a premature declaration of victory over inflation. We don’t think many market participants are on the same page.

Perhaps because it’s been several decades, a complacent and perhaps unaware market is not sufficiently pricing in the tail risks of spiraling inflation, a painful recession that includes stagflation, if supply shocks persist, or an acceleration of Fed tightening. This places asset prices at risk of correction. Yet this same complacency also presents investors with a tactic that could help mitigate losses in the event of a tail risk: Accessing options markets.

Optimism has left options prices cheap, meaning the put options that confer downside protection on securities can be layered onto a portfolio with the aim of better weathering a market sell-off. Investors can also consider allocating toward more defensive equities segments and adjusting fixed income duration to mitigate the worst effects of either inflation or aggressive rate hikes. When uncertainty is high, options might mitigate downside risk, while still enabling portfolios to maintain some upside exposure. And this is important because hope – while not a strategy – could prevail with supply issues resolving themselves and idled labor being lured back into the workforce, pressuring wages downward. All of which would contribute to the Fed’s task of quelling inflation.

The market is likely finding it difficult to process that the “Fed Put” has finally run its course and that asset prices are less of a consideration in policy prescriptions. The end of that era means that investors need to take the potential for tail risks more seriously – something we believe they are not doing at present – and implement tactics themselves with the aim of protecting portfolios.

Options (calls and puts) involve risks. Option trading can be speculative in nature and carries a substantial risk of loss.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

10-Year Treasury Yield is the interest rate on U.S. Treasury bonds that will mature 10 years from the date of purchase.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

Cboe Volatility Index® or VIX® Index shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500® Index options and is a widely used measure of market risk. The VIX Index methodology is the property of Chicago Board of Options Exchange, which is not affiliated with Janus Henderson.

ICE Bank of America MOVE Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options. It is the weighted average of volatilities on Treasuries with maturities ranging from 2 years to 30 years.

Sign up for timely perspectives delivered to your inbox.