July 2022 Specialty Equities

Global property: durable cash flows more important than ever Copy

Tim Gibson

Tim Gibson

Co-Head of Global Property Equities | Portfolio Manager Greg Kuhl, CFA

Greg Kuhl, CFA

Portfolio Manager Guy Barnard, CFA

Guy Barnard, CFA

Co-Head of Global Property Equities | Portfolio Manager

![]()

Portfolio Managers Guy Barnard, Tim Gibson and Greg Kuhl highlight the importance of pricing power as a key differentiator among property companies amid an uncertain backdrop.

KEY TAKEAWAYS

- Real estate differs from many other investments as the majority of income is derived from contractual leases, providing a high degree of certainty.

- In markets where demand outstrips supply, landlords are more likely to be able to benefit from full occupancy and command higher rents on expiring leases – this is known as ‘pricing power.’

- We believe that durable pricing power is a key differentiator, particularly in times of macroeconomic uncertainty.

KEY TAKEAWAYS

- Real estate differs from many other investments as the majority of income is derived from contractual leases, providing a high degree of certainty.

- In markets where demand outstrips supply, landlords are more likely to be able to benefit from full occupancy and command higher rents on expiring leases – this is known as ‘pricing power.’

- We believe that durable pricing power is a key differentiator, particularly in times of macroeconomic uncertainty.

The value of any income-producing asset, be it an apartment building, a cancer drug, a video streaming service, or the coupon payments from a corporate bond, can be estimated as the present value of a future stream of cash flows the asset is expected to produce. The concept of ‘present value’ math is fundamental to finance and investing.

The importance of present value

There are two key inputs used in estimating the present value of a cash flow stream: the ‘discount rate’ and the estimated future cash flows from the asset.

Without getting overly technical, the discount rate is a rate of the risk-appropriate annual return that is expected from an investment. Discount rates are usually built up from a ‘risk-free’ rate, for example, the prevailing yield on a 10-year US Treasury Bond. Investors should be compensated if an investment has more uncertain future cash flows compared to a US Treasury Bond. This means the additional risk taken in the hope of additional return warrants a higher discount rate when calculating present value.

In financial modelling, future cash flows are divided by an appropriate discount rate to estimate their present value. To account for compounding returns, future cash flows need to be discounted annually, so a cash flow 10 years in the future is worth less in present value today than the same cash flow one year in the future. Following this logic, we can begin to understand how higher interest rates should, in theory, lead to a lower present value for all financial assets. In practice, there are a multitude of factors that can influence the return on an investment. One important factor is interest rates; the sudden rise in interest rates this year (where we saw the US 10-Year Treasury yield double from 1.5% to circa 3.0% at the start of 2022 through to end May) significantly impacted both economies and markets as borrowing became more expensive for individuals and businesses. This impact is reflected in the negative year-to-date returns produced by both equity and fixed income markets globally.

Income certainty provides some comfort

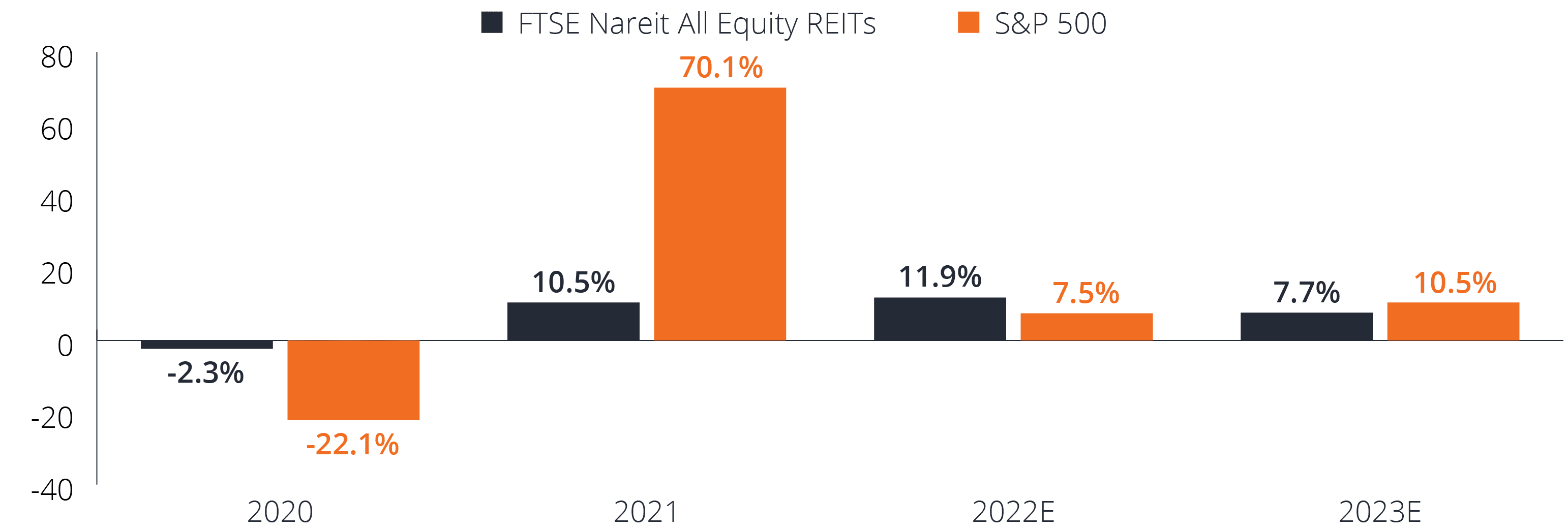

While interest rates are one of the key determinants of real estate present value, we think it is worthwhile to discuss the other main factor – estimated future cash flows. Real estate is different than many other types of investments. Because the vast majority of income is derived from contractual leases, a significant portion is therefore ‘known’ with a high degree of certainty. This is reflected in the relative consistency of US Real Estate Investment Trusts’ (REITs) earnings growth when compared with the S&P 500® Index over the last few tumultuous years, as illustrated in Figure 1.

As real estate investors, we don’t typically have to make estimates of production capacity, unit sales, or whether a competitor might come out with a new type of service/gadget that rapidly displaces demand and alters the status quo. Instead, we look to determine whether a landlord will be able to collect the rent owed, and what demand for future available space may look like.

Figure 1: REITs’ earnings growth has been more consistent compared to broader equities

Important material differences between Equities and REITs:

Important material differences between Equities and REITs:

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments. Real estate securities, including Real Estate Investment Trusts (REITs) may be subject to additional risks, including interest rate, management, tax, economic, environmental and concentration risks. Real estate securities, including Real Estate Investment Trusts (REITs), are sensitive to changes in real estate values and rental income, property taxes, interest rates, tax and regulatory requirements, supply and demand, and the management skill and creditworthiness of the company. Additionally REITs could fail to qualify for certain tax-benefits or registration exemptions which could produce adverse economic consequences.

Defining pricing power in real estate

In an environment where rates are rising and putting pressure on the value of financial assets, investors should try to avoid the ‘double whammy’ that could come from reduced estimates of future cash flows due to a slowing macro environment, in addition to higher rates. What real estate investors should, in our view, be focused on is identifying and understanding the types of properties, and the geographic markets, where the balance of supply and demand is favourable for landlords. In markets where demand outstrips supply, landlords are more likely to be able to benefit from full occupancy, command higher rents on expiring leases now and potentially into the future. We call this ‘pricing power’ and believe that the identification of landlords possessing this advantage is key to real estate investing.

Pricing power is even more crucial in times of macroeconomic uncertainty like the present. Those landlords with assets benefiting from long term-secular demand drivers and/or facing structural under-supply, such as industrial, life science real estate (lab space), specialty residential, and technology real estate sectors, are more likely to be well positioned for long-term growth.

The power of durable cash flows

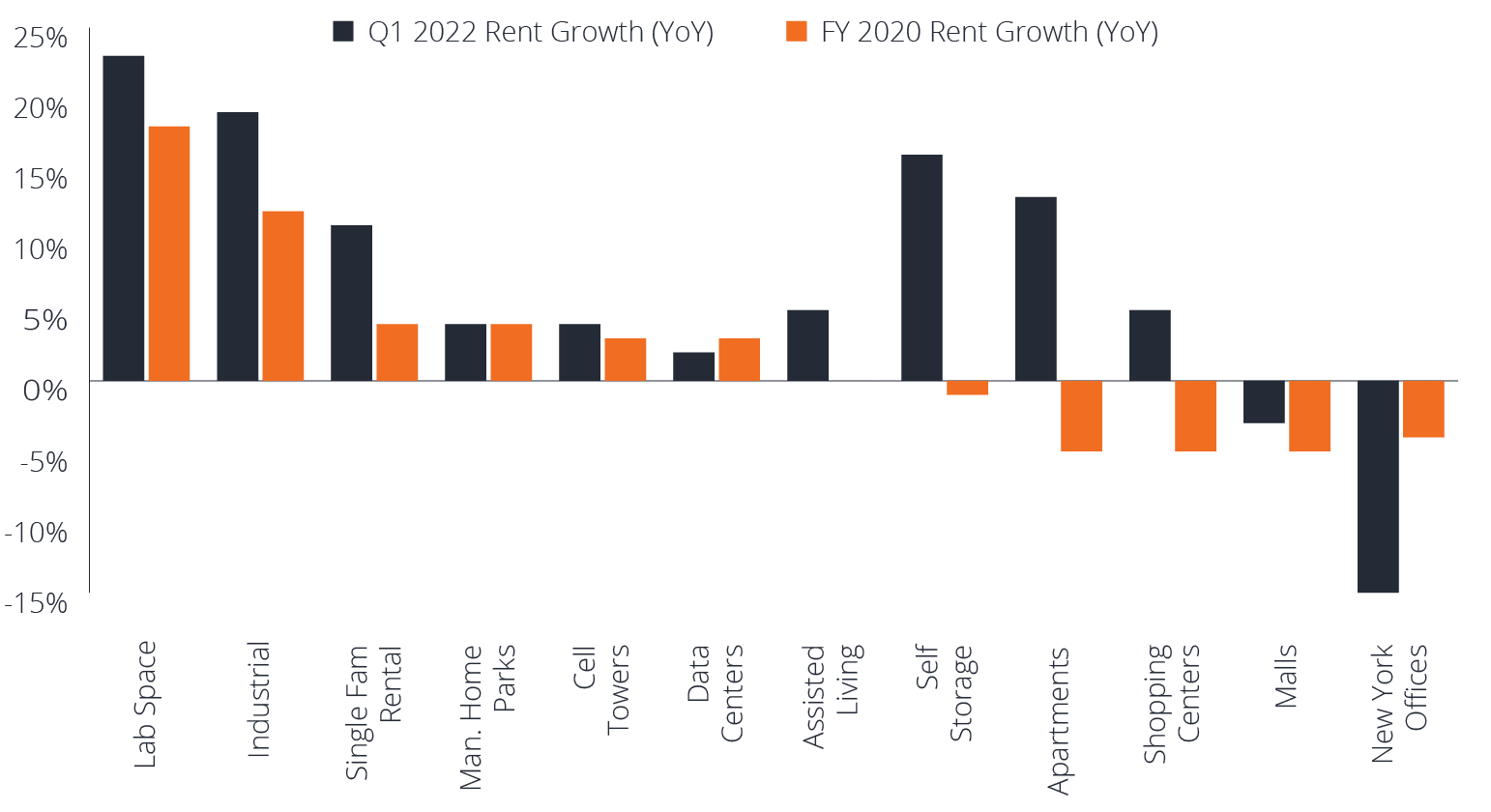

Figure 2 provides a concrete example of pricing power within real estate property types. We have shown reported rental pricing from an array of US-listed REITs representing major property types for the most recent quarter, Q1 2022, when property fundamentals could be considered almost universally strong. For comparison purposes we have also included rental pricing data for the full year 2020, a period when demand fundamentals across the broader economy were deeply challenged.

While there is no single perfect indicator, in our view the ability to maintain or increase rental pricing in the difficult environment of 2020, and also to deliver strong rent growth two years later, is indicative of sustainable pricing power.

Figure 2: Pricing power: rent growth in both weak and strong macro environments for certain property types

The volatility in financial markets seen year-to-date underscores a heightened level of uncertainty, amid a challenging backdrop of rising rates, inflationary pressures and slowing growth. Moving into the second half of the year, we believe that identifying those landlords with pricing power will be increasingly important given the continued uncertain macroeconomic backdrop. We expect those landlords that possess this advantage, operating in parts of the real estate market where inflation can more easily be passed through to tenants via higher rents, are more capable of generating positive real income.

OWN REAL ESTATE IN A

DIFFERENT WAY

Own. Innovate. Diversify

Featured Funds

JERIX

Global Real Estate Fund

JNGSX

Global Real Estate Fund