Subscribe

Sign up for timely perspectives delivered to your inbox.

The Global Property Equities Team discusses why listed REITs now make a more compelling investment proposition given the reduction in leverage, while the longer-term, largely fixed-rate debt structure reduces exposure to rising rates.

The structural decline in bond yields and interest rates have undoubtedly been a tailwind for real estate investors in recent years. With rates now on the rise and credit markets experiencing turbulence, there’s a looming fear that “the music may stop” and the run of strong performance may come to an end.

REITs are priced daily by stock markets and tend to adjust quickly to uncertainty, with the result being that meaningful valuation declines have effectively been priced in already (U.S. REITs have declined 20% year to date to 28 June 2022).1 Conversely, private real estate valuations, which are by nature backward looking, are still reporting gains year to date (the largest U.S. non-traded REIT is up 6.7% this year to the end of May).2 Only time will tell if these valuations are accurate.

What is certain, however, is that the listed REIT sector is not in the same vulnerable place it was in before the GFC. Unlike many of their private sector counterparts, most REITs have not indulged in overenthusiastic borrowing over the past decade. Instead, they have maintained discipline, avoiding the trap of taking on excessive financial leverage (debt) when asset prices were appreciating. Scars from the GFC changed the way many listed REIT companies operated. Balance sheets have been fortified, meaning that if the asset class heads into a potential U.S. recession, it does so in the best financial health. With lower leverage, stronger liquidity and continuous access to capital markets, the listed real estate sector stands on a considerably firmer footing.

Balance sheets matter for any real estate investor, even more so during periods of rising uncertainty, higher borrowing costs and lower availability of capital. Operating with higher financial leverage adds financial risk into the return profile of real estate. Leverage can enhance returns on the way up, but it can also exacerbate negative returns on the way down. If real estate yields rise sharply, as is being predicted by the public markets, more highly levered vehicles are likely to experience more drastic declines in equity values versus those that have taken a more prudent approach.

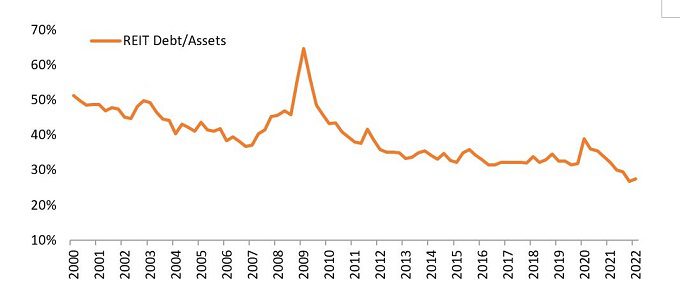

The listed REIT sector falls into the latter camp, with leverage (measured as the ratio of debt to total assets) at a more than two-decade historic low of just 28% (Figure 1). This represents an 18% decline compared to the end of 2007 and a 37% decline from the peak of the GFC. Crucially, listed REITs have successfully achieved lower leverage in this property cycle by relying more heavily on raising equity capital and joint ventures rather than debt to fund acquisition and development efforts.

Source: Nareit, Janus Henderson Investors as at 29 June 2022. US REITs debt/assets (leverage) from Q1 2000 to Q1 2022.

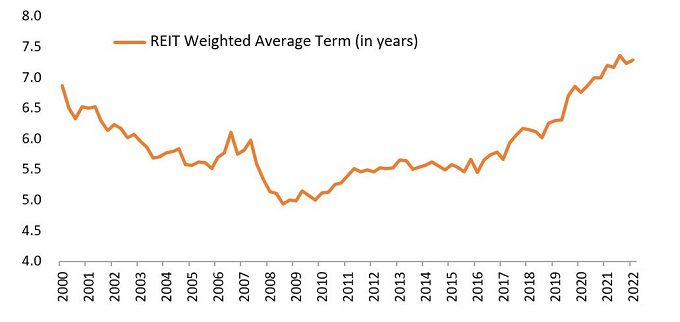

Over the last decade, it has been general practice for listed REITs to ladder their debt in a way that matches the term of their leases with tenants. This has the effect of spreading the refinancing risk over several years. The weighted average maturity of debt of U.S. REITs today is approximately 7.3 years, versus just 5.3 years at the end of 2007 (Figure 2). In addition, many REITs have been benefiting from fixing a large proportion of their debt at the more attractive funding rates of recent years, with a typical range between 75% to 95% fixed-rate debt today.3 According to Morgan Stanley Research, in fact, only around 11% of total U.S. REIT debt is maturing in 2022-23, at an average rate of 3.3%. Refinancing into a higher rate environment assuming a rate of 5.5% would only be a roughly 2.0% headwind to REIT cash flows.

With long-term and largely fixed financing in place, the reduced exposure to rising interest rates means there is likely to be less impact on REIT earnings in the short term. Healthy balance sheets, coupled with revenue growth driven by a robust supply and demand fundamental backdrop, should support rising dividends for shareholders in the coming years.

Source: NAREIT, Janus Henderson Investors as at 29 June 2022. Weighted average term to maturity (years) Q1 2000 to Q1 2022.

Continuous access to permanent capital afforded by the public equity and debt markets is a significant advantage to listed REITs in economic downturns. A key characteristic of the asset class is that the vast majority of listed REITs have investment grade credit ratings. In 2019, 68 U.S. REITs had an investment-grade rating, versus just 44 in 2006 as reported by the National Association of Real Estate Investment Trusts (Nareit). This provides listed REITs with significantly more flexibility compared to private managers, which are almost exclusively reliant on mortgages that are tied to a specific property or properties.

With an investment-grade stamp that reflects stronger balance sheets, many listed REITs are likely to have the flexibility to invest, ramp up external growth activity and take advantage of any potential distress in the private markets.

Balance sheet quality ultimately matters most when macro risks are highest. While investors who follow listed REITs daily are aware of the strides the industry has made, generalist investors or those more familiar with private real estate often assume listed REITs are much more levered than they really are. Many still view the industry through a pre-2008 lens. Based on the data we can see today, however, those concerns seem rather misplaced.

Listed REITs, non-traded REITs and private real estate funds all own commercial real estate assets that are broadly comparable. The fact that listed REITs have posted a year-to-date decline of 20% while the largest non-traded REIT is reporting a positive return of 6.7% mentioned earlier means one of two things: either private vehicles, with their higher leverage, are facing large asset value write-downs and even larger equity value losses, or listed REITs have diverged from private valuations for a non-fundamental reason and should eventually return to the parity at which they have historically traded. In either case, we believe listed REITs, with their lower financial leverage and currently attractive valuations, are looking compelling relative to their non-traded peers.

1 Source: Bloomberg, FTSE Nareit Equity REITs Index USD (FNRE), year-to-date returns to 28 June 2022.

2 Source: largest US non-traded REIT factcard as at 31 May 2022.

3 Source: S&P Global Market Intelligence as at 30 June 2022.

REITs or Real Estate Investment Trusts invest in real estate, through direct ownership of property assets, property shares or mortgages. As they are listed on a stock exchange, REITs are usually highly liquid and trade like shares.

Real estate securities, including Real Estate Investment Trusts (REITs) may be subject to additional risks, including interest rate, management, tax, economic, environmental and concentration risks.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity, and differing financial and information reporting standards, all of which are magnified in emerging markets.

FTSE Nareit Equity REITs Index contains all equity REITs not designated as timber REITs or infrastructure REITs. The FTSE Nareit U.S. Real Estate Index Series is designed to present investors with a comprehensive family of REIT performance indexes that spans the commercial real estate space across the US economy.

Sign up for timely perspectives delivered to your inbox.