Subscribe

Sign up for timely perspectives delivered to your inbox.

The financial impacts of rising prices can cause investors to make irrational decisions. Retirement Director Ben Rizzuto outlines different approaches financial professionals can take to help clients manage their emotional reactions to inflation and understand the importance of staying invested.

Inflation affects us in many ways. The main way we feel it is on a day-to-day basis when we go to the supermarket or gas station. Gas prices here in the United States have increased 32% since February 23 – the day before Russia invaded Ukraine1 – and the price of food and groceries is up nearly 9% year over year as of March.2 This is painful for consumers and investors, who are in effect losing money due to inflation.

It’s important for financial professionals to understand that these losses can cause clients to make emotional (and often bad) decisions. For example, it could lead investors to sell their “risky” assets and put those proceeds into cash. This defies logic, as the rational thing to do when prices are rising is to seek investments that have the potential to grow at rate that can outpace inflation. While that may be the case, we also know that humans don’t always behave rationally.

We have seen this irrationality play out around the world as investors have increased the amount of money they have in cash, money market funds or liquidity stocks.

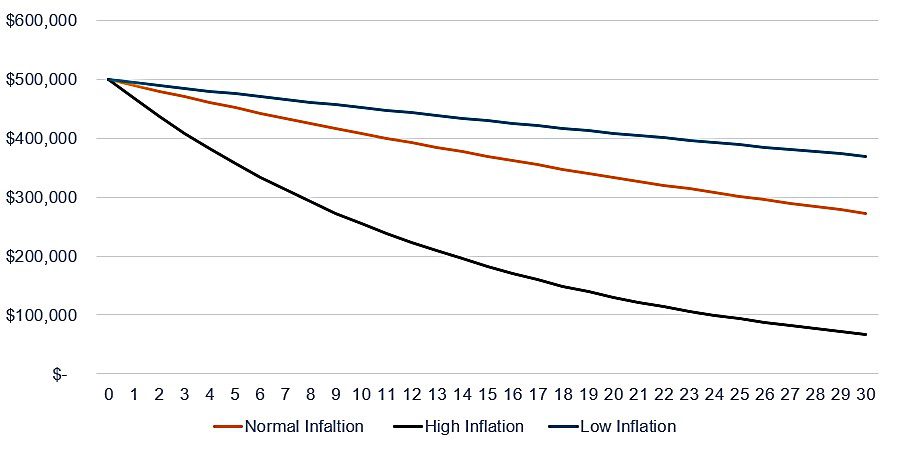

So how can we help our clients understand that they must stay invested in order to continue building toward their future savings goals? One approach is to illustrate the point using data such as the chart below, which shows how savings can be eroded by inflation over time. The data is calculated using the “Rule of 72,” which is used to determine how long an investment will take to double given a fixed annual rate of interest. By dividing 72 by the annual rate of return, investors can obtain a rough estimate of how many years it will take for the initial investment to duplicate itself (or, in a high inflation scenario, be cut in half).

Source: Janus Henderson. Normal Inflation = 2.0%, High Inflation = 6.5%, Low Inflation = 0.5%

Source: Janus Henderson. Normal Inflation = 2.0%, High Inflation = 6.5%, Low Inflation = 0.5%

That’s why I think it’s important to help clients think about the impact of inflation in different ways. That could mean asking to your client to think of themselves as a business and reminding them that running a profitable business means saving and growing your overall net worth at a pace that exceeds your input costs. Over time, if you have to pay more for the materials used to make your products, then you will eventually need to increase the price of your product. Your client can apply this same basic thinking to their personal finances, but in this case, the product is their investments and savings, and the input cost is inflation. The higher inflation goes, the more they need to save and the more those savings need to grow.

Reminding clients that many people are conservative, risk averse and hold assets in cash – and backing it up with research – will help them feel heard. And if they understand their emotions are shared by others, the hope is that they will say, “If that’s the case, what should I do next?”

From there, we can follow some simple but important financial planning steps:

Set goals. Simply making sure clients think fully and deeply about – and then write down – their goals can help decrease stress.

Create a plan. The importance of this step in helping clients cope with stress can also be backed up by research: 75% of investors who do not have a plan report experiencing high levels of negative stress.5 Not only does creating a plan help set a course, but it also allows you to review the client’s goals based on future changes in the market, expenses, health, taxes – and yes, inflation. Plus, going through this process can help clients reduce negative stress. And with lower negative stress, they will be more likely to stick to the plan.

Don’t discount the importance of liquidity. Research has found that liquid wealth or cash has a higher correlation to perceived wellbeing than total investments, spending income or indebtedness.6 Even when interest rates are low, cash plays an important role in asset allocation during changing market and economic conditions, including what we’re going through right now. Using a bucketing approach, for example, allows us to keep the majority of assets invested in the market but also have a small portion of cash on hand. That small portion of cash helps clients meet expenses, but more importantly it can provide an emotional check against bad decisions.

Start small. Remember, we’re dealing with investors who may be risk averse, stressed out and emotional based on what’s going on in the markets. Because of that, I think discussing a dollar-cost averaging approach may be a helpful tactic for investors, both young and old.

People may be hesitant to invest in general, and the idea of investing $10,000 or more all at once may be incredibly scary. Dollar cost averaging allows investors to start small but have less money at risk, which can help lessen those feelings of loss aversion. One of the other reasons I like this type of arrangement is that it helps individuals create a financial habit. What’s more, that financial habit of consistently investing a certain every month can help smooth out the impact of volatility over time and potentially outpace inflation.

The financial impact of inflation provides us with a view of how the loss of money can affect investors emotionally. It also provides us with an opportunity to let our clients be heard and to remind them that long-term financial goals are best pursued through long-term planning – not short-term emotions.

1“US gas prices jump to record high $4.67 a gallon.” CNN, June 1, 2022.

2 “Rising inflation has made it more expensive to eat at home-here’s how much grocery prices have increased.” CNBC, April 12, 2022.

3 “Inflation and Individual Investors’ Behavior: Evidence from the German Hyperinflation.” Fabio Braggion, Tilburg School of Economics and Management, February 2022.

4 “Study: The War on Stress.” Financial Planning Association, Investopedia, and Janus Henderson, 2019.

5 Ibid.

6 “How your bank balance buys happiness: The importance of ‘cash on hand’ to life satisfaction.” Ruberton, P. M., Gladstone, J., & Lyubomirsky, S. Emotion, 2016.

Volatility measures risk using the dispersion of returns for a given investment.

Sign up for timely perspectives delivered to your inbox.