Subscribe

Sign up for timely perspectives delivered to your inbox.

Adrienn Sarandi, Head of ESG Strategy & Development, and Bhaskar Sastry, ESG Content Manager, believe that biodiversity loss is a crisis that could have systemic impacts akin to climate change. Here, they outline considerations for investors seeking to address the issue in their portfolios.

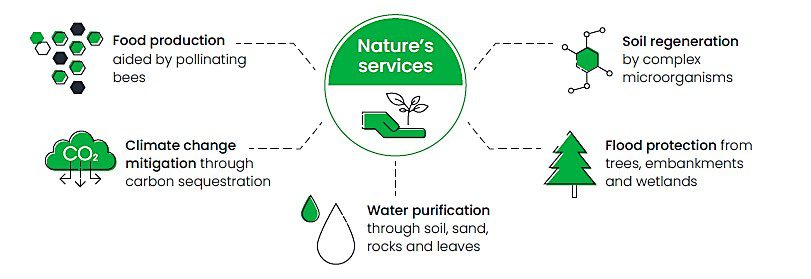

Nature’s services underpin our very survival and global economic activity, thus directly influencing wealth creation and preservation. The value of biodiversity and ecosystems to our physical and mental well-being is inestimable. Natural capital also provides critical “ecosystem services” that provide us with huge economic benefits.

Source: Janus Henderson Investors, 2022.

Source: Janus Henderson Investors, 2022.

Along with deforestation, biodiversity loss also exacerbates the systemic threat of climate change. Climate change, in turn, is acting to worsen biodiversity loss. Diverse ecosystems with healthy biodiversity are essential for climate change adaptation and mitigation, increasing resilience to future climate impacts. Biodiversity loss also increases the likelihood of the emergence of diseases that can pass from animals to humans, like COVID-19.

Global action to tackle the biodiversity crisis has been slow but will be given added impetus at the UN Biodiversity Conference (COP15) expected to take place in August 2022. COP15 will bring nations together with the aim of galvanizing efforts to protect critical habitats, improve water quality, control invasive species and safeguard connectivity. Furthermore, with the March 2022 publication of the beta Taskforce for Nature-related Financial Disclosures (TNFD) framework, which aims to align corporate reporting and investment to address nature-related risks, the next few months could be critical in terms of efforts to reduce biodiversity loss.

We believe investors must accept that biodiversity loss and ecosystem damage represent significant and financially material risks to their portfolios.

The University of Cambridge Institute for Sustainability Leadership (CISL, 2021) has divided nature-related financial risks into three categories that investors should evaluate:

Investors should identify those companies that acknowledge their impact and dependence on nature, particularly agriculture and food. Investors can also use engagement to pressure companies to align with commonly agreed upon nature-based goals and disclose nature-related risks where possible.

Depending on an investor’s desired approach, biodiversity considerations can be integrated into an overall portfolio approach. Some approaches may focus on maximizing risk-adjusted returns and assessing biodiversity from a risk management and opportunities perspective, while others may invest with the aim of achieving a positive impact alongside returns.

Implicit in all approaches is that investors should be guided by a systems-thinking mindset. The climate and biodiversity crises show that nature – on which our survival depends – works as an interconnected, dynamic system with feedback loops. The economic and societal impacts of investors’ decisions are not narrow, short-term and linear, but rather wide-ranging, long-term and highly unpredictable. We believe investors must accept this paradigm if they are to contribute to solutions around biodiversity loss and ecosystem damage.

1 The Economics of Biodiversity: The Dasgupta Review (UK Government, 2021).

2 The Global Assessment Report on Biodiversity and Ecosystem Services (Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES), 2019).

3 Living Planet Report’ (WWF, 2020).

4, 5 Nature4Climate.org (2020).

6 Nature Risk Rising: Why the Crisis Engulfing Nature Matters for Business and the Economy (WEF, 2020).

7 The Future of Nature and Business (World Economic Forum, 2020).

Environmental, Social and Governance (ESG) or sustainable investing considers factors beyond traditional financial analysis. This may limit available investments and cause performance and exposures to differ from, and potentially be more concentrated in certain areas than, the broader market.

Sign up for timely perspectives delivered to your inbox.