Subscribe

Sign up for timely perspectives delivered to your inbox.

Amid the wild swings in the bond market and the RBA’s new stance, Jay Sivapalan, Head of Australian Fixed Interest at Janus Henderson, provides his perspective on the threats and opportunities.

The race that stops a nation didn’t stop our fixed interest team’s active bond trading and portfolio management right across Melbourne Cup day and long into the night as the Australian bond market continued its wild swings.

Inflation fears resulting from COVID-related supply issues have led markets to ignore the Reserve Bank of Australia’s (RBA) forward guidance, bringing forward monetary policy tightening expectations to mid-2022 and factoring in both rising inflation and a strong economic rebound in 2022.

Yields have risen sharply across the government yield curve, with the largest moves at the shorter end of the curve, suggesting cash rates rising in the near-term.

While the RBA stayed the course by keeping cash rates at 0.10%, it has responded by changing its stance on yield curve control. Through its pandemic response, monetary policy support from the RBA included a commitment to cash rates remaining at 0.10% until 2024, but this is now no longer the case.

The Reserve Bank of New Zealand is already fending off 4.9% inflation, while other major economies are also recording rising inflation, this is clearly worrying investors about what might be ahead for Australia, contributing to the market’s response to the latest CPI figures released on 27 October.

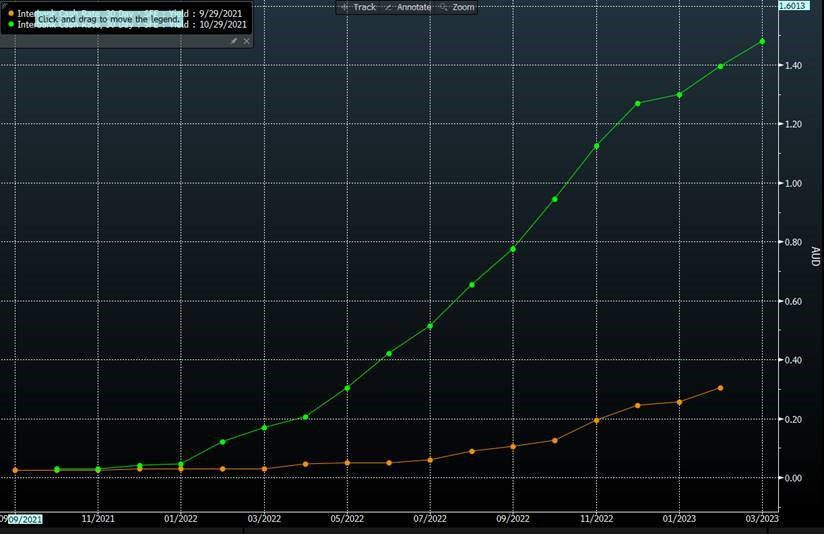

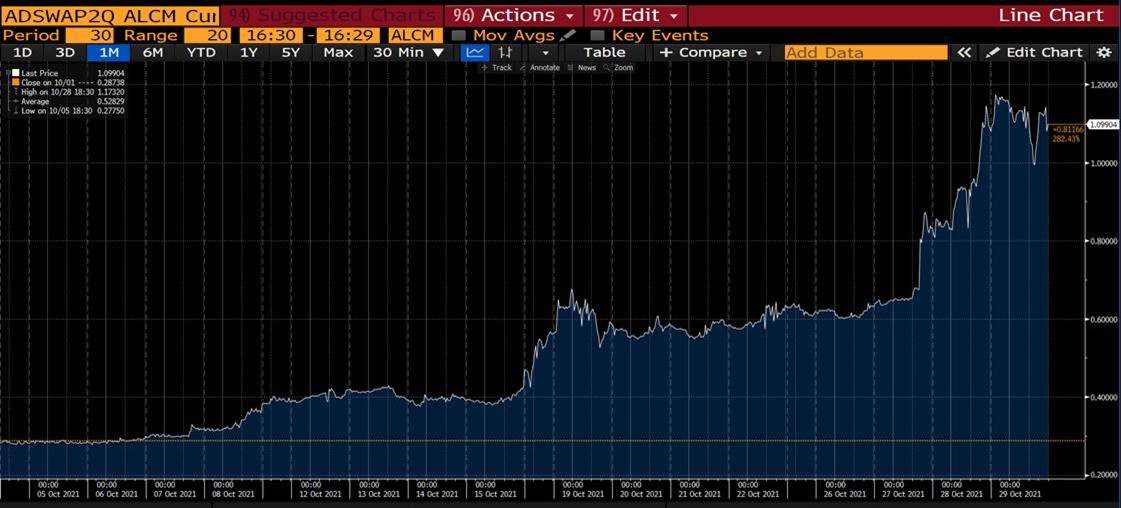

Chart 1: Cash rate expectations (%):

The Australian bond market (as defined by the Bloomberg AusBond Composite 0+ Yr Index), fell by 3.55% over October, mirroring February’s falls, resulting in the second biggest bond market sell-off in nearly four decades. Over the past year to the end of October, the bond market is down 5.30%.

Markets have baked in an aggressive monetary policy tightening profile over the next two to three years and noting that the cash rate before the pandemic was 1%-1.5%, we assessed this as an overshoot representing good value, essentially enabling investors to ‘lock in’ higher yields.

It is hard to predict exactly when markets will re-assess and even more difficult predicting turning points in markets. What is clear, however, is that attempting to pursue active strategies after the market has turned is too late and ineffective.

In both periods of market turmoil and in periods of market stability, our approach to investing places a strong emphasis on preserving our investors’ capital. As such, while October left bond investors with few places to hide, the impact to the returns of the Janus Henderson Tactical Income Fund in these conditions was materially less than that of the Australian bond market1 and the fund’s benchmark2. This was principally due to active interest rate management.

Through the pandemic period, we have been guided by our investing ‘North stars’, which provide us with perspective in periods of market volatility. These are:

Specifically, through the recent bond market turbulence:

1. Bloomberg AusBond Composite 0+ Yr Index.