Subscribe

Sign up for timely perspectives delivered to your inbox.

Fixed income portfolio managers Jennifer James and Tom Ross consider how efforts to rebalance the economy in China are having far-reaching implications.

Trying to describe China’s economy in recent decades has always been a lesson in economic gymnastics. From a more traditional communist command economy through to a capitalist hybrid model, China is now undergoing another reinvention as it seeks to share prosperity more equitably. It has even coined a name for it: “common prosperity”

China’s economy has grown at a blistering pace in the last few decades, enabling it to climb up the rankings of per capita GDP and proudly assert earlier this year that it had eliminated extreme poverty within the country. The economic ascendancy has been unequal, however, with urban areas outpacing rural communities and a new billionaire class forming as the country both expanded its industry and embraced consumerism. Last year alone, the number of USD billionaires in China rose by 238 to 626 according to the 2021 Forbes List. The Gini coefficient – a measure of income inequality in a country – had been falling for several years prior to 2015 but more recently has been climbing. The latest figure for 2019 was 0.465 – a figure above 0.4 is indicative of a high level of income inequality (Source: CEIC, National Bureau of Statistics, September 2021).

For China, inequality comes with additional consequences. Its political system relies on stability so there is a desire to ensure the majority of people feel they have a stake in the system. China is intent on undergoing social engineering through policy tools. Few countries can do this effectively and even fewer have such firm ambition.

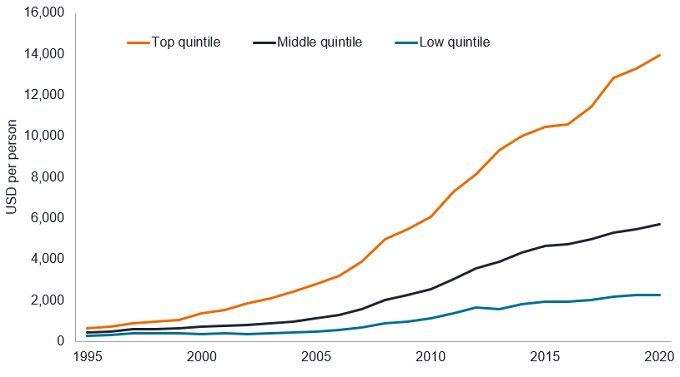

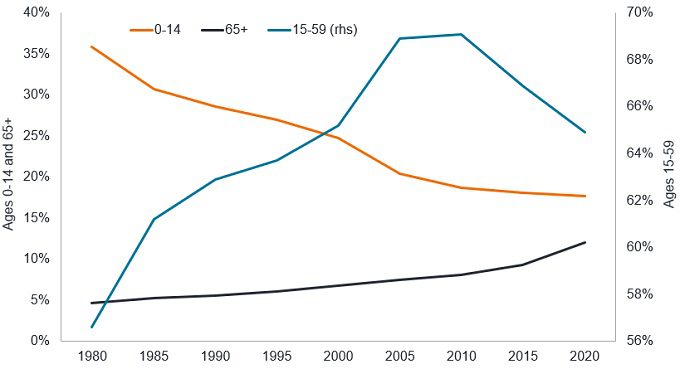

Figure 1a highlights the speed at which the wealthiest cohort have begun to move away from the middle and lower income cohorts. Common prosperity seeks to enlarge the middle class at the expense of the ultra-wealthy. The aim is social harmony. A second derivative of this would be to increase China’s birth rate (happier and economically stable people are more likely to have children). A major concern for authorities is the growing dependency ratio as the proportion of people aged 65 and over steadily increases while the population of working age shrinks as a share of the overall population (Figure 1b).

Figure 1a: Urban disposable income in China by quintile

Source: Morgan Stanley, CEIC, Wind, mean quintile urban disposable income, USD, 1995 to 2020. A quintile represents one fifth of the population.

Figure 1b: China’s population structure by age group

Source: United Nations Population Division, World Population Prospects 2019, percentage of total population by broad age group, both sexes (per 100% of total population).

The policy tools to achieve these social goals have so far targeted specific sectors that the government views as being either monopolistic (eg, technology) or those creating barriers for social upward mobility (eg, private educational tutoring, expensive healthcare and expensive property).

Methods have been blunt, often with little warning. As such, markets have not reacted well. To be fair, China has a habit of permitting rapid growth in industries, only to introduce tight regulation once an industry is firmly embedded. Examples include the imposition of safety standards on dairy products in the late noughties and a crackdown on luxury entertainment and gifts in recent years to tackle corruption. The regulatory reset currently taking place covers a much broader range of industries, from gaming to semiconductors, education to property.

Currently, it is the property sector that is absorbing the most headlines, with the fallout from China Evergrande, the huge Chinese property developer, making waves. China has struggled to curb soaring property prices, not least because developers want higher prices to boost profits and local governments rely heavily on land sales for the bulk of their revenues, in some cases over 90%. In fact, land transfer revenues grew from CNY 50.7bn in 1998 to CNY 8.4 trillion in 2020, representing 8.3% of total GDP (China Banking News, 15 June 2021).

Pressure to cool prices has come from central government, which sees high property prices as an impediment to social progress and an expense that is discouraging households from having more children.

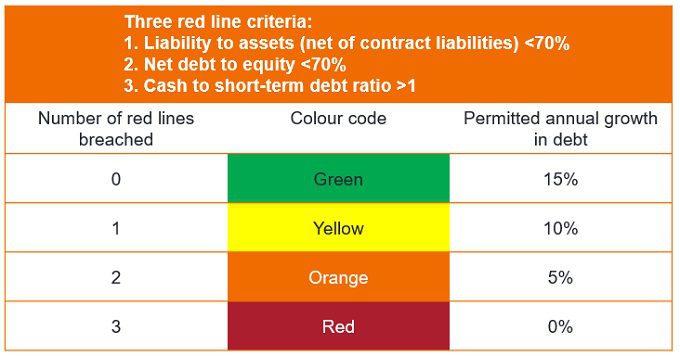

Recent efforts to cool prices began last year with the trial of the “three red lines” test. This concept demanded developers submit detailed reports of their finances to be assessed against three criteria. If one or more of these three lines is breached, then the regulator can limit the extent to which a developer can grow their debt.

Figure 2: Three red line criteria

Source: Bloomberg, press reports, September 2021

This policy is not expected to be formally implemented until June 2023, but the market has been quick to single out those companies most at risk of failing the three threshold criteria.

Evergrande is one of a number of property developers who are rapidly seeking to shore up their balance sheets. This is leading to a purge of inventories of housing and land stock, which is depressing margins. Evergrande’s issues are self-created as it could have been more proactive with its debt reduction by selling non-core assets, looking for strategic buyers and communicating better with investors. The challenge for Evergrande is its size. It is the biggest property developer in China and at the end of June 2021 had more than CNY 2.2 trillion (US$330 billion) in liabilities outstanding, which includes debt, deferred income tax and accrued trade payables (Source: Refinitiv Datastream).

Concerns that Evergrande may default on its debt has seen its bonds drop to around 25 cents in the dollar in mid-September 2021, essentially a quarter of their par value (Source: Bloomberg, 20 September 2021). The property sector relies partly on offshore funding to operate, which is why the response in the credit markets has been particularly severe.

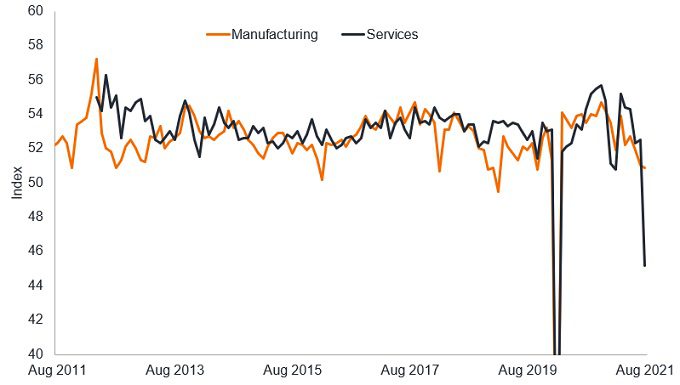

A messy restructuring would be bad for China and come at an inopportune time given that the country is already showing evidence of an economic slowdown (Figure 3).

Figure 3: China Purchasing Managers’ Indices reflect a weakening economy

Source: Refinitiv Datastream, National Bureau of Statistics of China, Purchasing Managers Index, Manufacturing Sector, Services, seasonally adjusted, August 2011 to August 2021. A reading below 50 indicates contraction.

Stalling confidence in China is leading to a tightening of liquidity conditions. The People’s Bank of China made several liquidity injections during September, including CNY120 billion (USD18.5 bn) on 22 September to help maintain liquidity in the financial system (Source: Xinhua, 22 September 2021).

For now, investors are having to gauge how much market pain the authorities in China are prepared to tolerate to achieve their goals. With China such a key player in the global economy, the risk is that fallout in its property sector spreads globally through markets.

When China coined the phrase “common prosperity” most investors assumed this meant the domestic economy; the law of unintended consequences could see it come to refer to China exporting its growth slowdown to all.

Socio-economic engineering: policies designed to deliver specific social and economic goals.

Command economy: an economy that is centrally planned by the state, the opposite of a

Capitalist economy where free enterprise and private ownership of capital drives the economy.

Dependency ratio: a demographic measure of the ratio of the number of dependents to the total working age population in a country

Monopolistic: a market dominated by one large supplier

Balance sheet: an accounting statement showing the assets, liabilities and capital of a business.

Par value: this is the price at which the bond was first issued and the amount the bond issuer agrees to repay at maturity.

Liquidity: the ease with which assets and financial instruments can be bought and sold; also describes flows of money around the financial system.

Sign up for timely perspectives delivered to your inbox.