Subscribe

Sign up for timely perspectives delivered to your inbox.

Property Equities Portfolio Managers Guy Barnard, Tim Gibson and Greg Kuhl discuss the impact of rising inflation and interest rate expectations on listed real estate.

Inflation remains the topic du jour, and probably for good reason. Having been in a downward trend since 1980, falling from 15% to around 2% in the last decade based on Organization for Economic Co-operation and Development (OECD) data, it is now on the rise.

What does this mean for property equities, and what are the implications from rising bond yields?

Bank of America (BofA) recently stated that they “believe a turning point for both inflation and interest rates has arrived and the 40-year bull market in bonds is over.”1 The investment bank’s view is based on the unprecedented supportive government policy measures worldwide that will likely lead to inflationary pressures.

This is quite a headline-grabbing statement, and while only time will tell if it is correct, we have seen a recent pickup in inflation expectations and interest rates/10-year U.S. Treasury (bond) yields.

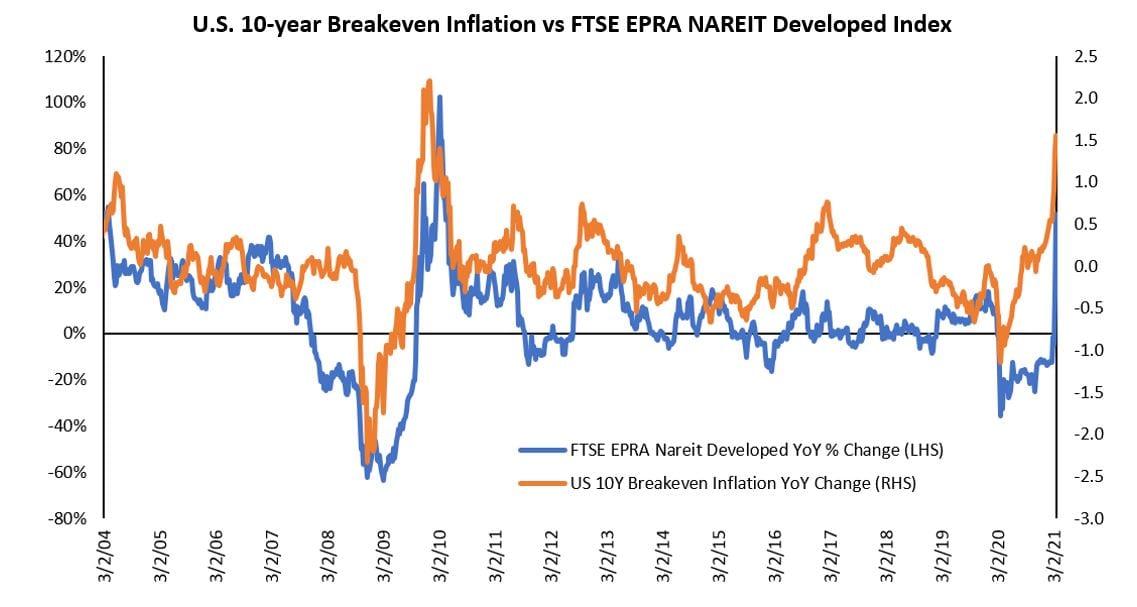

Thankfully, the relationship between inflation expectations and real estate equities is a little clearer with, historically, a positive correlation existing (i.e., as inflation expectations have risen, so too have real estate equities). This relationship has persisted over the longer term, highlighting the potential for real estate equities to benefit from rising inflation expectations (Figure 1).

[caption id=”attachment_370323″ align=”alignnone” width=”1137″] Source: FactSet, Janus Henderson Investors, as at 22 March 2021. Index year-on-year (YoY) percentage change from March 2004 to March 2021, weekly data, in USD terms. Breakeven inflation is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity and is taken as a more reliable measure of inflation expectations. Past performance is not a guide to future performance.[/caption]

Source: FactSet, Janus Henderson Investors, as at 22 March 2021. Index year-on-year (YoY) percentage change from March 2004 to March 2021, weekly data, in USD terms. Breakeven inflation is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity and is taken as a more reliable measure of inflation expectations. Past performance is not a guide to future performance.[/caption]

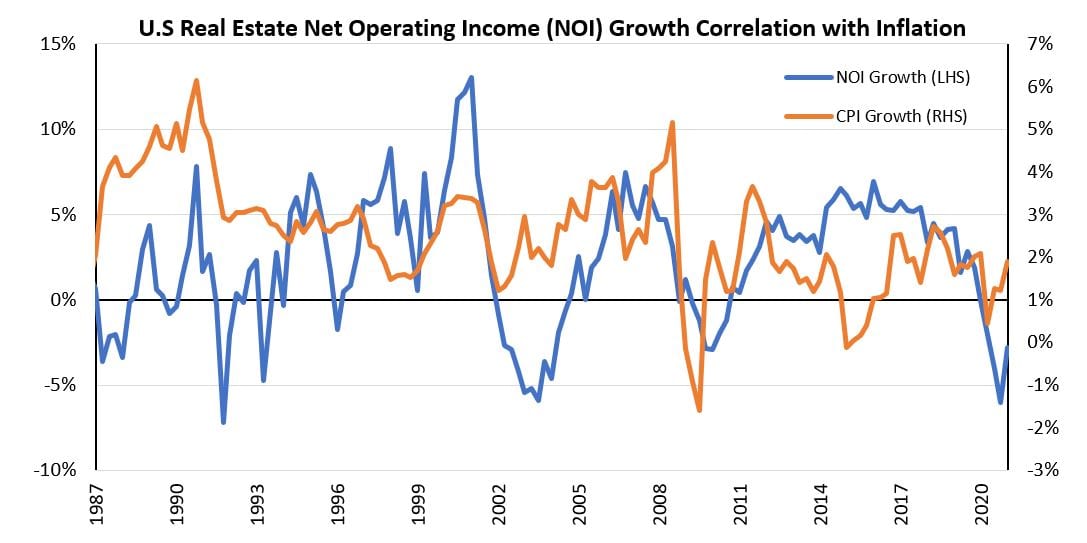

We often talk about real estate as being the “landlords of the economy” whose income streams benefit from positive economic growth. A recovering economy typically leads to rising rental income and increases the value of underlying real estate assets. Rental contracts are often linked to inflation through annual uplifts or are reset when they expire, as can be seen from Figure 2.

[caption id=”attachment_370334″ align=”alignnone” width=”1087″] Source: National Council of Real Estate Investment Fiduciaries (NCREIF), U.S. Department of Labor, CEIC, Refinitiv Datastream, UBS estimates as at Q1 2021. Net Operating Income/NOI measures an income-producing property’s profitability before costs from financing or taxes. NOI growth calculated as the sum of four quarter-on-quarter NOI growth, CPI/Consumer Price Index (inflation) calculated is the sum of four quarter-on-quarter growth.[/caption]

Source: National Council of Real Estate Investment Fiduciaries (NCREIF), U.S. Department of Labor, CEIC, Refinitiv Datastream, UBS estimates as at Q1 2021. Net Operating Income/NOI measures an income-producing property’s profitability before costs from financing or taxes. NOI growth calculated as the sum of four quarter-on-quarter NOI growth, CPI/Consumer Price Index (inflation) calculated is the sum of four quarter-on-quarter growth.[/caption]

However, there is a distinction among property sectors: When it comes to rental negotiations, rising inflation tends to have a bigger positive effect on sectors that have pricing power. The acceleration in real estate trends as a result of COVID-19 – as discussed in our recent article – has seen certain sectors negatively impacted, such as shopping centers, regional malls and hotels. However, others have been uplifted by strong secular tailwinds such as e-commerce, cloud computing and changing demographics. Industrial, logistics and real estate tech (e.g., cell towers and data centers) are among the sectors that are likely to benefit the most.

We do not know the exact direction or magnitude that inflation and yields will take, but believe it is becoming increasingly difficult to overlook an asset class that currently has an attractive valuation, offers structural and secular growth, and is capable of providing effective protection from inflation.

1BofA Global Research, The Case for Real Assets, 25 March 2021.