Subscribe

Sign up for timely perspectives delivered to your inbox.

The monetary backdrop for markets has become less favourable, suggesting increased volatility and greater downside risk for equities and other risk assets.

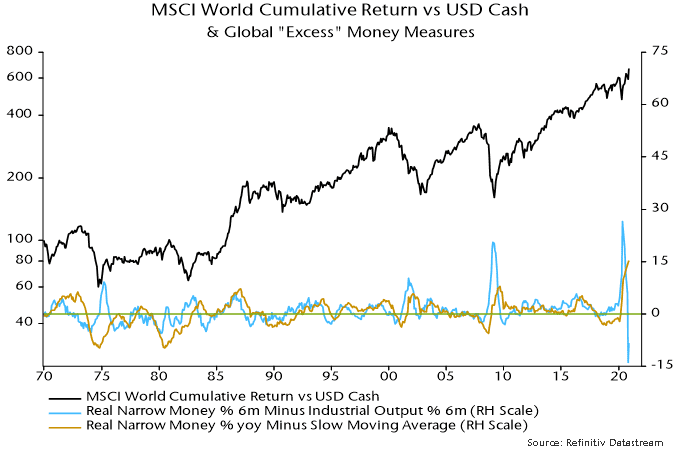

A simple “monetarist” rule for switching between global equities and US dollar cash is monitored here, based on two measures of “excess” money – the gap between six-month growth rates of real narrow money and industrial output, and the deviation of 12-month real money growth from a long-run moving average. Historically, equities outperformed cash significantly on average when the measures were positive, and underperformed when they were negative – see first chart.

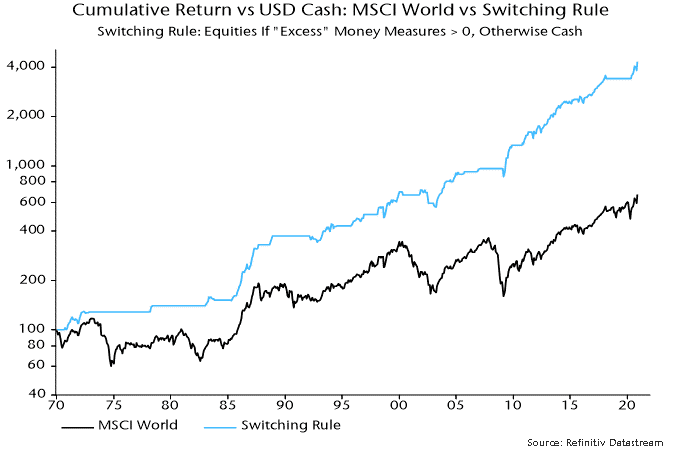

The simple rule holds equities only when both measures are positive, otherwise reverting to cash. Despite being “out of the market” for long periods, the rule would have outperformed buying and holding equities by a wide margin – second chart.

The rule allows for data publication lags and recommended cash at the start of 2020 – real narrow money growth was above (weak) industrial output growth but remained below its long-run average. The latter shortfall reversed in March, causing the rule to switch to equities at end-April.

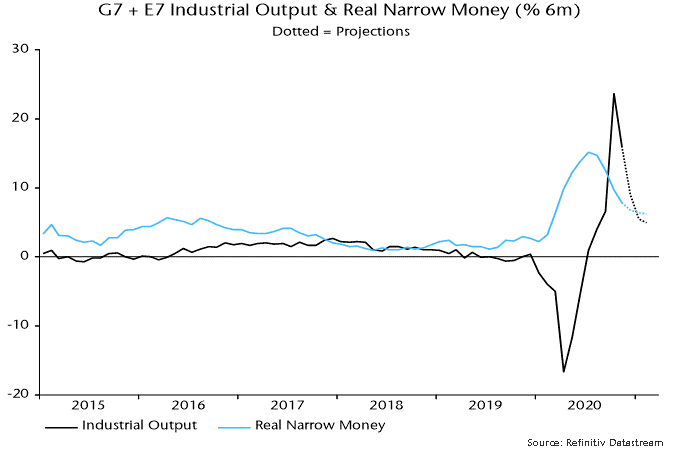

A V-shaped industrial recovery, however, was reflected in six-month output growth surging past real money growth in October, with partial data indicating that the lead was maintained in November – third chart. The first of the two measures, therefore, turned negative In October, resulting in the simple rule recommending a switch to cash at end-December.

The period in cash could be quite short. On plausible projections, included in the first chart, the six-month real money / industrial output growth gap could turn positive again in January, in which case the rule would switch back to equities at end-March.

A further caveat is that equities performed worst historically when both measures were negative. Underperformance relative to cash was modest on average when the first measure was negative but the second positive, as now.