Subscribe

Sign up for timely perspectives delivered to your inbox.

Jay Sivapalan, Head of Australian Fixed Interest at Janus Henderson Investors, explains how the team are positioning for the economic recovery and how Biden’s win and promising COVID-19 vaccine developments are presenting new opportunities.

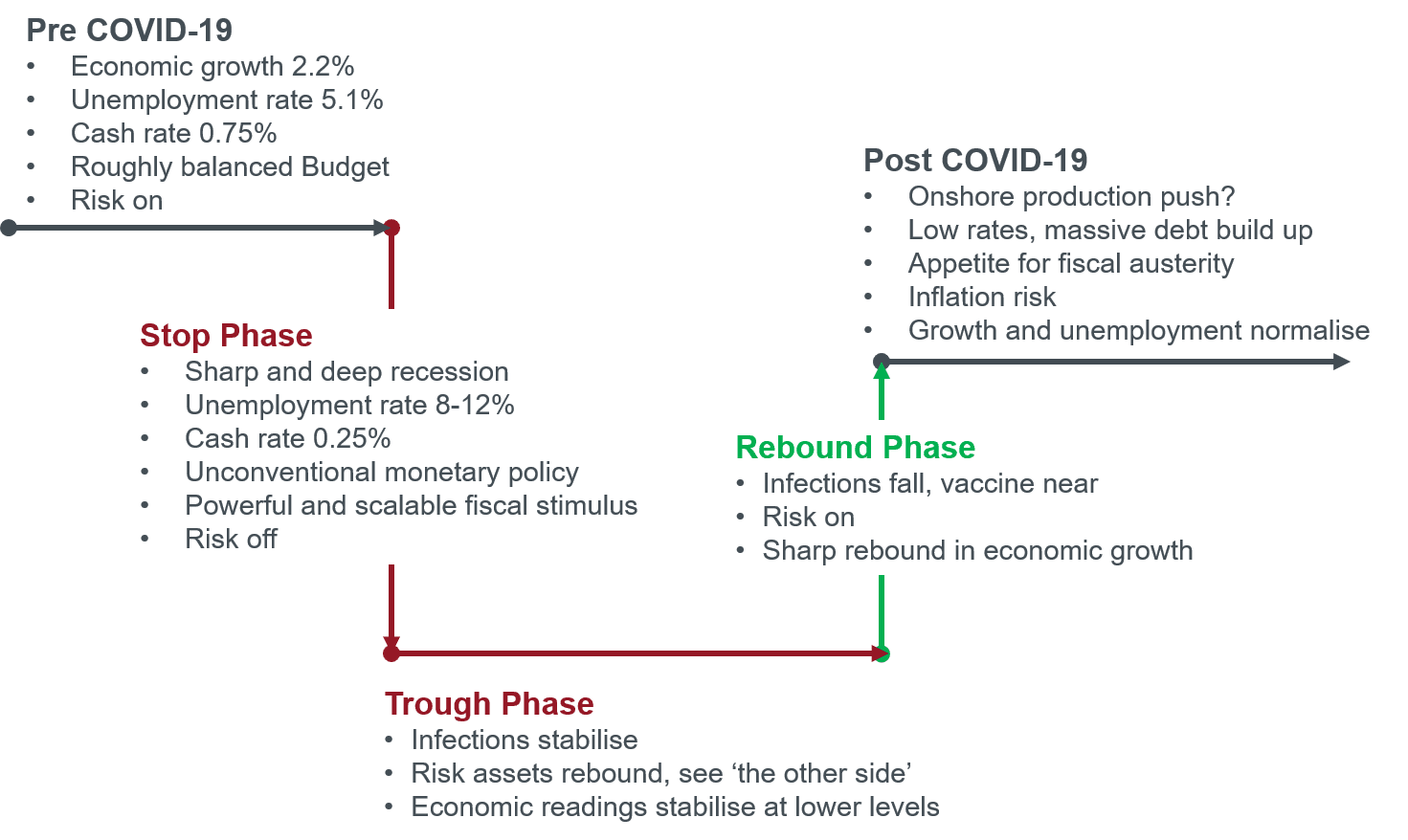

Breaking down crises into phases, there are essentially three to consider – the economic downturn, the recession phase and the economic recovery. In March the crisis kicked off as an economic ‘stop’ as travel restrictions, lockdowns and social distancing measures were introduced. This then led to the phase we currently find ourselves in – Australia’s first recession in three decades.

Back in March, Investment Strategist, Frank Uhlenbruch, published an article (read it here) which clearly broke the crisis into these phases. The chart in his article is worth revisiting as we are now past the ‘stop’ and moving from ‘trough’ to ‘rebound’ stage. Our focus now is how we position for the reflation trade in the recovery while being mindful that we are still in a recession.

Chart 1: The Australian economy’s U-shaped outlook

Source: Janus Henderson Investors, Australian Bureau of Statistics.

We are looking at the opportunities arising from a period of economic recovery, while taking a sector-by-sector view, remaining cognizant that some sectors will be impaired and should therefore be avoided. As active managers, we are afforded this flexibility and we can navigate the path to recovery as nimbly as we navigated through this crisis and into the recession. Looking at three sectors as an example, below we provide our views and the key questions we are seeking to answer.

Rather than looking at the banking sector as a single unit, we believe there is some merit in being selective when it comes to scale. For example, are the Big Four banks more able to fund the technological change, regulatory change and rising compliance costs in the sector, compared with the smaller regional bank names?

In the case of supermarkets, a key question has been whether COVID-19 has provided a short-term boost to sales which will unwind as lockdown restrictions lift, or are some behavioural and economic factors more permanent? For example, has the way we shop changed permanently, meaning more online shopping with home deliveries and smaller top-up shops in physical stores? And, how would supermarkets need to pivot their businesses to support this behaviour change, with new distribution centres and logistics to support a sudden, rather than gradual, shift to e-commerce?

The same situation – of bricks versus clicks – may also be playing out in the retail sector more broadly, with retail property trusts facing an uncertain future. Again, will a transition to online shopping remain, or will mix of online and offline be the way forward, meaning potential for smaller physical stores and therefore lower rental income for retail estate investment trusts (REITs)?

The above are just three sector examples, but the implications across industry are significant.

At a macro level, with the Reserve Bank of Australia (RBA) cutting cash rates to 0.1% and providing guidance that rates will stay at these levels for the next three years, this has signalled that reduced borrowing costs will be available for an extended period of time in a bid to stimulate investment and economic activity.

Beyond this, the RBA has also committed to buying Australian and State government bonds to push bond yields lower and to keep the recovery going, while governments have committed to ongoing support measures and fiscal stimulus.

In a supportive environment like this, equity markets will near certainly be ‘off to the races’ and credit markets will likely also perform well, particularly if there’s a vaccine around the corner. This was evident following the recent news about success rates of a number of the COVID-19 vaccine clinical trials, restoring some confidence in a return to more normal conditions in the near future.

While this is an environment where good quality credit can perform well, poorer quality credit (which we avoid) can perform even better; essentially playing catch up. With our ‘quality before price’ investment philosophy and focus on security selection, we seek sustainable sources of return which are more stable in volatile markets. While this can mean losses can be limited in a downturn, it can also result in comparably smaller returns in ‘risk-on’ periods.

While we see the period ahead as promising from an economic recovery point of view, the path ahead is uncertain and there are no guarantees that subsequent lockdowns won’t happen again. The recent lockdown situation in South Australia is testament to how quickly situations can change, and this is likely to be the case until vaccines can be rolled out nationally.

Our portfolios are constructed to be ‘all weather’ solutions and should markets suffer another event as witnessed in March, we are able to limit losses while actively shifting to capitalise on any opportunities that present themselves.

For our Tactical Income Fund and Tactical Income Active ETF (the Funds) in particular, the Biden victory in the US presidential election and the positive news surrounding COVID-19 vaccine trials, have meant that bond yields have started to lift. This has resulted in recent bond market returns being firmly in negative return territory. That said, 10-year Australian Government bond yields moving toward 1% is approaching attractive valuations in our view and the Funds’ duration has increased to two years, at the time of writing, as we position ourselves to take advantage of this scenario.

As every investment textbook will attest, timing the market is difficult if not impossible, but actively positioning the Funds to respond to changing market conditions is precisely what the Tactical Income Fund is designed to do. While this means there could be an opportunity cost for moving too early, we believe this to be a prudent approach to take in order to secure a superior, lower-risk source of return in the prevailing low rate environment.