Subscribe

Sign up for timely perspectives delivered to your inbox.

There is no contradiction between unprecedented GDP falls and optimism about equity market earnings.

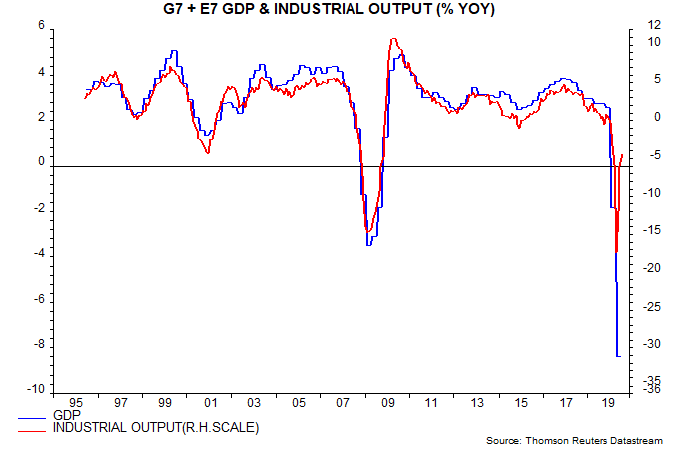

Global GDP and industrial output have been tightly correlated historically but with industrial output displaying three times the volatility of GDP – compare the left- and right-hand scales in the first chart.

This relationship has broken down in 2020 because covid health restrictions have undermined the usual relative resilience of services activity, which dominates GDP. The “beta” of industrial output to GDP has been much smaller than in previous recessions.

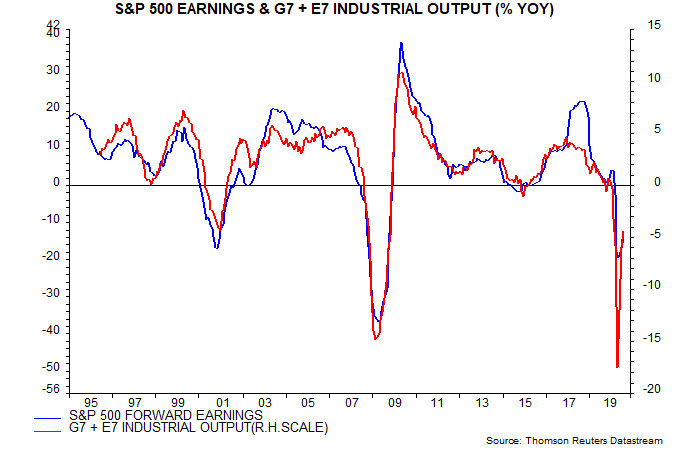

This is important for investors because equity market earnings have a large industrial element and hence a stronger correlation with industrial output than GDP.

The second chart shows the relationship of S&P 500 12-month forward earnings and global industrial output. Forward earnings overshot the historical relationship in 2018 because of corporate tax cuts. They fell by less than suggested by output during the covid shock but 12-month rates of change bottomed around the same time (April for output, May for earnings) and are currently consistent.

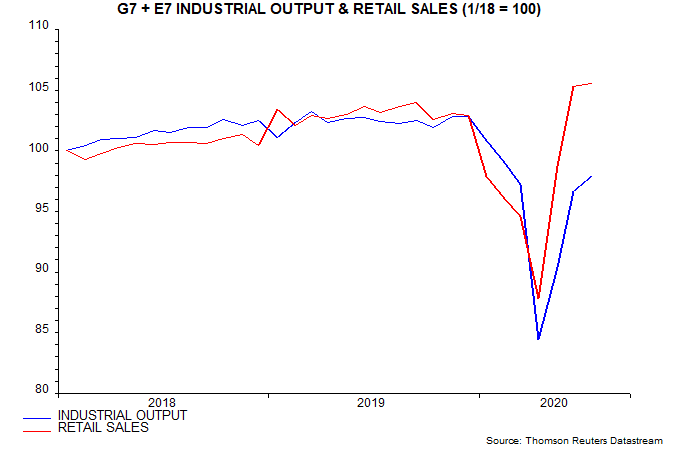

A further reason for the relative resilience of industrial output is that services activity restrictions have caused consumers to divert spending towards goods. Global retail sales appear to have risen further above their pre-covid peak in July, based on partial data – third chart.

The unexpected strength of goods demand coupled with production restrictions have resulted in an involuntary drawdown of inventories, which firms will attempt to reverse during H2 – an additional reason for expecting a V-shaped industrial recovery to continue to unfold.

Such a scenario implies a bullish earnings outlook – claims that forward earnings are already overoptimistic appear wide of the mark.

Positive earnings developments, however, could be neutralised or outweighed by a rise in real discount rates as the “excess” money backdrop becomes less favourable. The gap between six-month rates of change of global real narrow money and industrial output remained wide in July but could close by October – see previous post.