Knowledge. Shared Blog

August 2020

First In, First Out of COVID: How Has China Fared?

-

May Ling Wee, CFA

May Ling Wee, CFA

China Equities | Portfolio Manager

May Ling Wee, China equities portfolio manager, discusses the main highlights for investors in China stocks over the first half of the year and the outlook for the rest of 2020.

Key Takeaways

- China’s economic recovery has been faster than expected, driven by the industrial and construction sectors, but consumption and private sector investment remain weak.

- Chinese equities have outperformed developed markets over the first half (excluding the Nasdaq), and investor sentiment has been bullish on a recovery in economic growth and corporate earnings in the second half of the year.

- While there may be less value in growth stocks now, a correction could provide attractive opportunities to invest in quality growth stocks in the coming months.

The first half of 2020 was an eventful period for China equity investors. The severity of COVID-19 and the policy response to limit population movement in China to contain the virus surprised the market. By March, mobility restrictions were eased, economic activity resumed and a rebound in industrial activity swiftly followed as factories caught up on orders missed during the lockdown and construction activity restarted. China sought to initiate a “slow bull market.” This was supported by encouraging high-frequency data evidencing China’s early recovery, which led to strength in domestic equities since April.

At the time of this writing (August 12), margin financing (borrowing money to buy securities for retail investors) has increased rapidly and new fund launches have been heavily subscribed by domestic investors. Against this backdrop, China-U.S. relations have deteriorated. Rivalries have mounted as the two countries trade accusations around COVID and wrangle over the political backdrop in Hong Kong.

Growing Pains: The Trade-Technology War

Technology leadership has been at the epicenter of the trade-technology war between the U.S. and China. While U.S. sanctions were first levied on China’s technology hardware companies, including Huawei, they soon broadened to include Internet and software companies. The latest move by the U.S. has been to ban U.S. businesses from using video app TikTok and Tencent’s ubiquitous WeChat messaging app. Two Internet worlds are in co-existence, one led by the U.S. and the other by China. TikTok and WeChat serve as examples that the global ambitions of China’s leading technology companies can potentially be reined in by the U.S., and that sanctions can be imposed on Chinese companies on the grounds of “national security.”

An Unbalanced Recovery

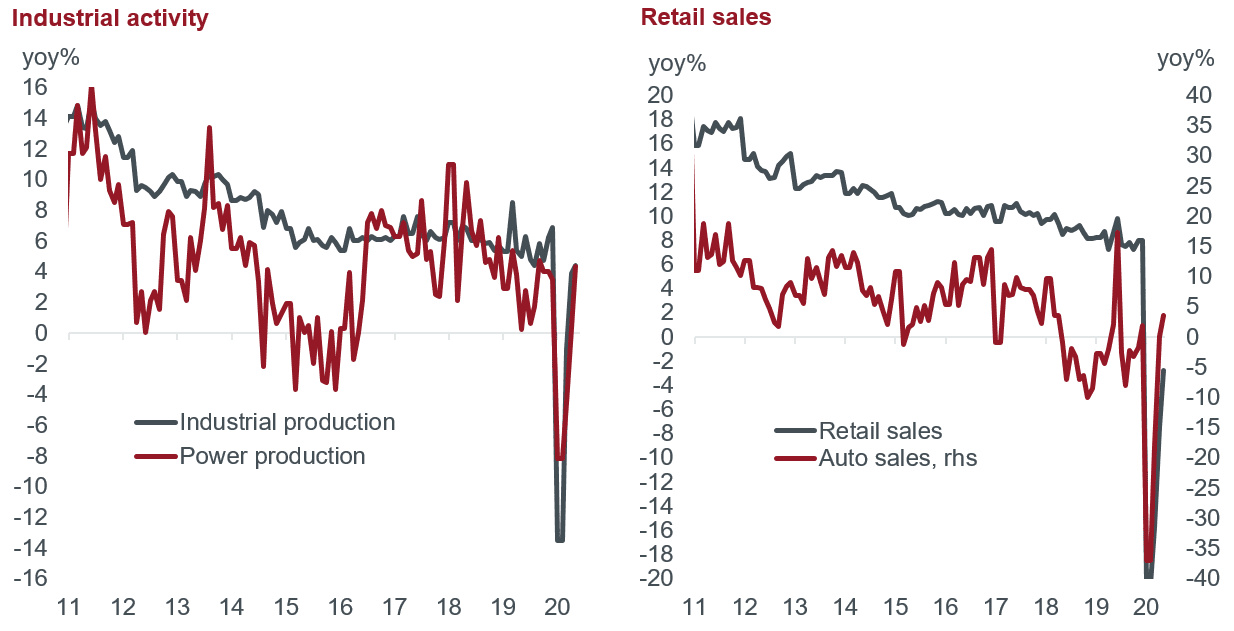

China’s progress in terms of economic recovery has been faster than expected since the easing of citizen mobility and the resumption of economic activity. Gross domestic product (GDP) growth for the second quarter of 2020 (2Q) was positive, both on a year-over-year and quarter-over-quarter basis, suggesting that the economy in 2Q was already growing above its pre-COVID level last year. However, the recovery has been uneven. The industrial and construction sectors have led this recovery, driven by infrastructure projects and factories catching up on lost production. China being ”first in and first out” of the COVID crisis benefited its manufacturing sector. Conversely, consumption and private sector investment have still not recovered to pre-COVID levels. Social distancing, the fear of infection and lower confidence in personal income have kept the consumer at home and spending less. Meanwhile, private businesses face demand uncertainty and the question of whether supply chains should be brought closer to home due to externalities such as a pandemic.

Industrial Activity Is Recovering Ahead of Consumer Activity

[caption id=”attachment_314107″ align=”alignnone” width=”1234″] Source: China National Bureau of Statistics, Wind, Macquarie, as of 10 July 2020. Note: Automobiles are less than 30% of retail sales.[/caption]

Source: China National Bureau of Statistics, Wind, Macquarie, as of 10 July 2020. Note: Automobiles are less than 30% of retail sales.[/caption]

Market Review: First Half 2020

The coronavirus caused significant disruption to business and consumer activity in China as well as to global supply chains, resulting in headwinds for revenues and profits. Chinese equities sold off when the outbreak evolved into a global pandemic. From their March lows, Chinese equities have performed strongly as macroeconomic indicators in 2Q showed a better-than-expected pickup in activity following February’s shutdown. Investor sentiment has been bullish on a recovery in economic growth and corporate earnings in the second half of the year. The offshore market (MSCI China Index) and onshore market (CSI300 Index) are up 12.8% and 13.9% year-to-date in U.S. dollars, respectively*. In fact, Chinese equities have outperformed most developed markets over the same period, with the exception of the Nasdaq.

Portfolio Implications

COVID-19 was challenging for many Chinese businesses. Physical/offline sales channels became ineffective and the fear of infection kept China’s consumers at home. That said, companies that performed well were quick to adapt to the new environment by focusing on online channels. Among the winners were those in areas such as e-commerce, online entertainment and home appliances, which outperformed offline alternatives by a wide margin.

In the consumer sector, companies selling higher-valued goods perceived as premium products outperformed peers selling into the mass consumer segment. This was evident in the sales of premium autos, baijiu (a popular liquor) and luxury goods. Similar to what we have seen globally, the higher-income consumer appears to have been better insulated from the impacts of the COVID-19 crisis.

Cautiously Optimistic on the Prospects for the Remainder of the Year

China has fared relatively well in terms of trade as its factories restarted before others. Consumers and businesses are adapting to a post-COVID world. In our view, barring a widespread second wave in China and with higher levels of savings made by consumers in the first half of the year, we could see improving consumption demand in the second half of the year, as long as confidence in China’s recovery is sustained.

While we expect the Chinese economy to strengthen, the political backdrop looks set to worsen, especially heading into the U.S. presidential election in November. The possibility of further disruptions to Chinese businesses cannot be ruled out.

Market strength and sentiment have led to re-ratings for many growth shares in China’s domestic stock markets, leaving less value in the growth segment of the market. However, the domestic Chinese asset class is naturally more volatile, being primarily driven by retail investors, and we believe a correction could provide attractive opportunities to invest in quality domestic growth stocks in the coming months.

Abandon Your Doubts,

Not Your Goals

Learn More*Source: Bloomberg, Index price returns 1 January 2020 to 12 August 2020. Past performance is not a guide to future performance.

Knowledge. Shared

Blog

Back to all Blog Posts

Subscribe for relevant insights delivered straight to your inbox

I want to subscribe