Subscribe

Sign up for timely perspectives delivered to your inbox.

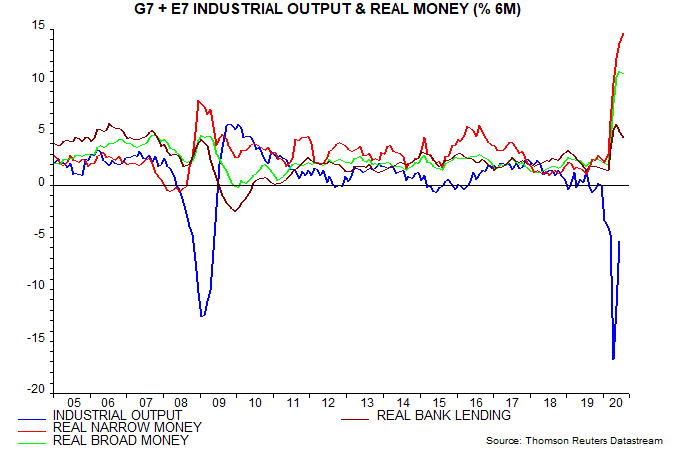

Monetary data for July are available for countries covering two-thirds of the global (i.e. G7 plus E7) aggregates calculated here. Six-month growth of real (i.e. CPI-adjusted) narrow money is estimated to have risen to another record last month, while real broad money growth stabilised and growth of real bank lending to the private sector slipped for a second month – see first chart.

Six-month real money growth is almost certainly peaking, implying a possible peak in six-month industrial output momentum around April 2021, allowing for an average nine-month lead.

The monetarist view is that the surge in money measures since early 2020 will be reflected in a significant rise in inflation in 2021-22. This does not, as is sometimes asserted, assume that the velocity of circulation reverts to its pre-crisis level, only that the trend rate of decline in recent decades does not accelerate.

Previous posts argued that the main driver of this trend velocity decline has been a rising wealth to income ratio – rising wealth boosts the portfolio demand for money. The trend fall in real yields has probably also been a factor. Investors believing that the trends in the wealth to income ratio and / or real yields are overextended and likely to reverse should anticipate a slower trend decline in velocity, i.e. more inflation per unit of money growth.

The monetarist jury is out on the issue of whether the expected 2021-22 inflation rise will be temporary or mark a shift to a permanently higher level. A return of broad money growth to its post-GFC average would support the former scenario. The bias here is to expect money growth to remain higher than in recent decades, because fiscal deficits are likely to remain large and require ongoing “monetary financing” to prevent market dislocation.

The legendary market analyst Russell Napier argues that broad money growth and inflation will remain high because of government intervention in the commercial banking system to compel sustained rapid expansion of credit to favoured companies and projects. The recent use of subsidies and guarantees to boost lending, according to Mr Napier, is transformational and implies that politicians have wrested control of the money supply from central banks. They will use this power in a dash for growth and in order to create inflation to reduce real debt burdens.

This scenario could play out over the medium term but the recent monetary boost from bank lending is likely to fade in H2 2020.

Broad money growth is significantly higher than lending growth currently, i.e. monetary deficit financing has been the more important driver of broad money acceleration.

Lending growth, as noted, appears to have peaked. The recent slowdown mainly reflects US developments: the stock of US commercial bank loans and leases contracted in June and July.

The earlier pick-up in global / US lending growth was partly accounted for by loans advanced under the US Paycheck Protection Program (PPP), most of which are likely to be cancelled / forgiven in H2 2020 / early 2021. This will depress the lending numbers although broad money will be unaffected because of a simultaneous transfer of cash from the Treasury to banks (i.e. more monetary deficit financing).

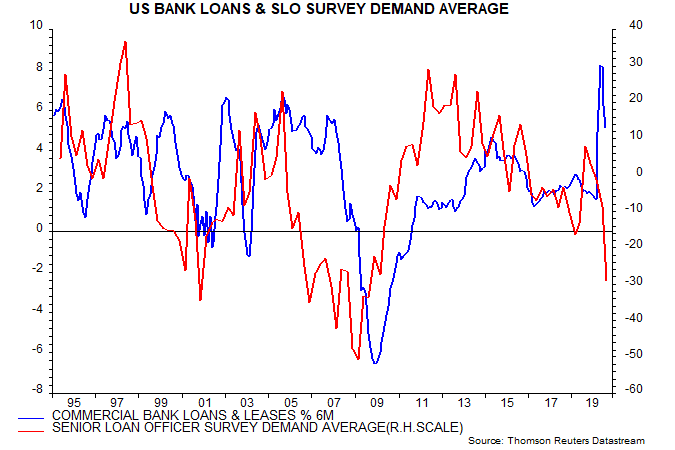

Aside from the PPP effect, US bank credit demand appears weak. An average of demand balances across loan categories in the July Fed senior loan officer survey fell to its lowest level since 2009, suggesting a further lending slowdown – second chart.