Subscribe

Sign up for timely perspectives delivered to your inbox.

Members of Janus Henderson’s global fixed income teams recently met to discuss the outlook for bond markets. While markets remain immune to the economic impact of COVID-19 so far, does the stability depend on the Fed’s support for survival?

The US economy has decisively rebounded from the lows reached in March and April, but momentum has waned in both the economy and the financial markets as rising cases of COVID-19 have forced some regions to once again restrict activity. High-frequency data from credit cards1. suggest there has been only a modest slowing in consumption in recent weeks and the housing market remains buoyant2., but initial jobless claims posted their first rise in late July since March2. raising concerns about the employment outlook. We think economic growth is likely to remain modest, balanced between pent-up demand and partial closures over the next few quarters, but positive nonetheless.

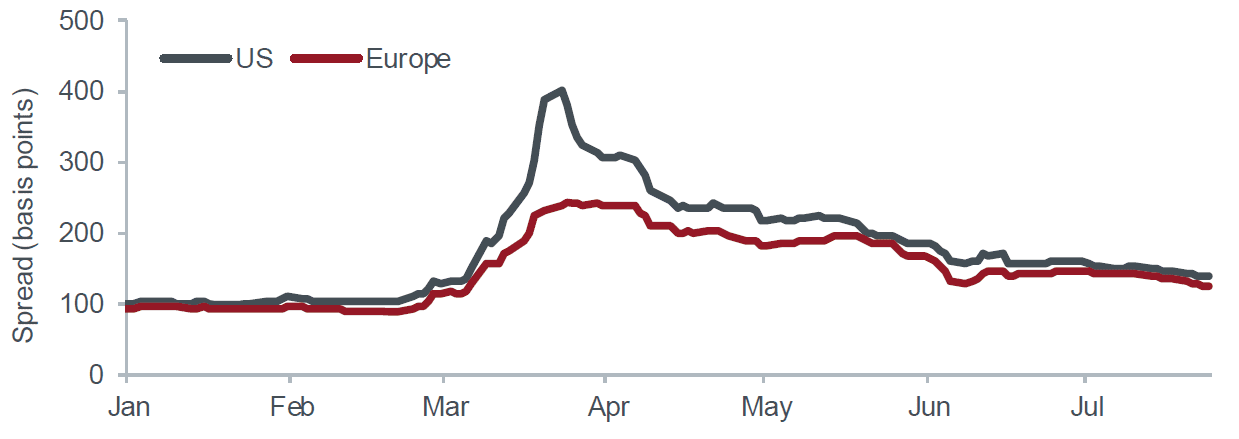

Investment grade spreads

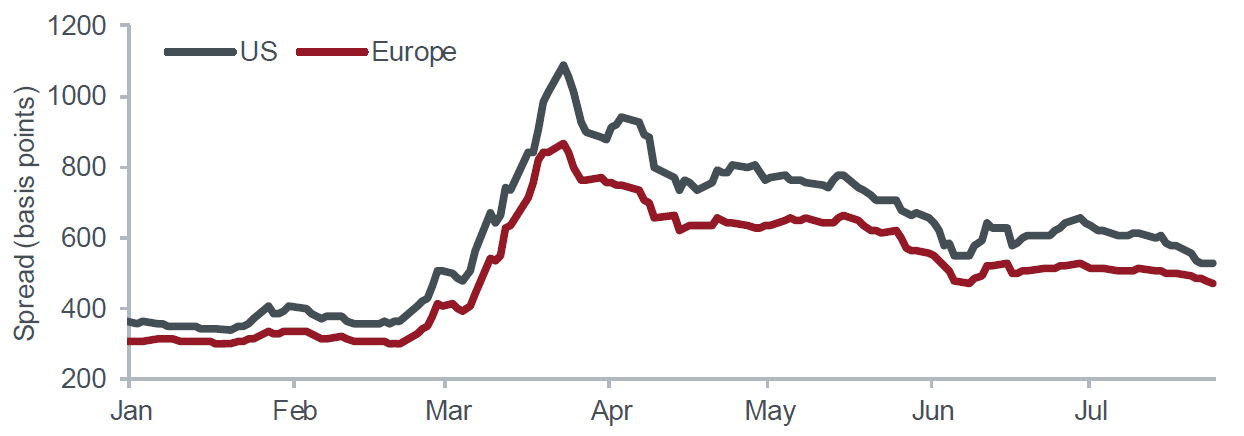

High yield spreads

Source: Bloomberg, Investment grade: ICE BofA US Corporate Index, ICE BofA Euro Corporate Index; High yield: ICE BofA US High Yield Index, ICE BofA Euro High Yield Index, Govt OAS (option adjusted spreads), 1 January 2020 to 24 July 2020

Since late June, markets have proved resilient to bad news. As cases of COVID-19 grew in regions across the US, credit markets slowed their rapid pace of recovery but did not widen. And more recently, weak earnings figures have been met with an acceptance that economic lockdowns were always going to result in temporarily poor outturns. Near term credit metrics have deteriorated as higher debt levels meet lower earnings but expectations are that they should recover from a 2020 low point.

However, markets have been encouraged by the message being sent by the world’s central banks. US Federal Reserve (Fed) Chairman Powell has been clear, consistent and constant in his reminders to the market that the Fed will do, in his words, “whatever we can, for as long as it takes” to keep bond markets functioning and credit flowing to companies. The market has, at this point, no reason to doubt him, and thus no reason to price fears of another liquidity collapse. Liquidity aside, zero percent policy rates and direct purchasing of corporate bonds by the Fed provide confidence that solid companies needing credit to weather the current recession will be able to fund themselves at reasonable rates. Put simply, if the worst is over, there is little reason to think spreads are likely to go significantly wider. And there is room for spreads, particularly in the high yield market and lower-credit quality structured securities, to tighten further.

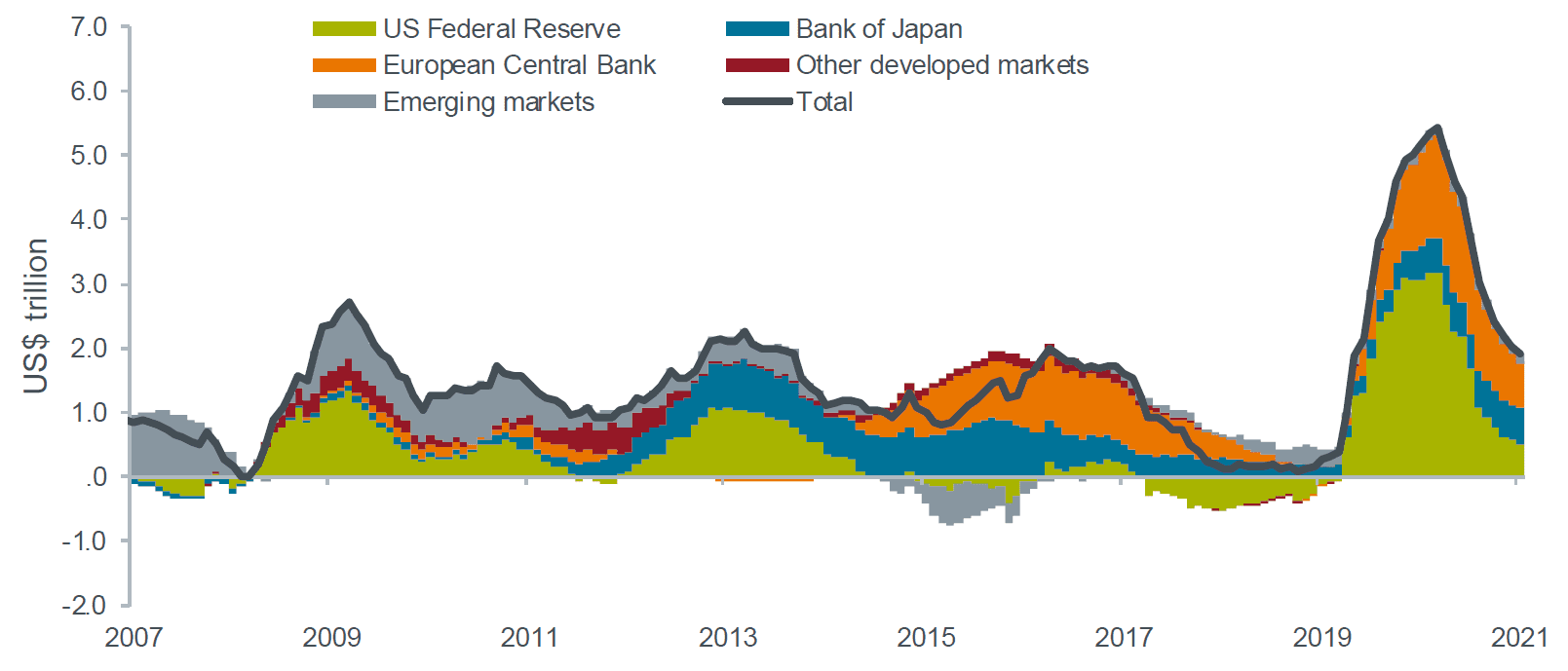

The aggressive actions taken by global central banks since the crisis began have pushed their balance sheets to historic levels and, particularly in the US, caused money supply to surge. Where does that money go?

Because the rise is historic, it is difficult to model based on past experience. However, we believe inflation is an unlikely result in the current climate and, similarly, the real economy will be slow to absorb the liquidity as capital expenditures and hiring are likely to remain subdued. That leaves the financial markets. As a matter of financial dynamics, the money does have to go somewhere and buying more financial assets is both quick and easy. By lowering policy rates to zero, the Fed has made it clear it does not want the money to flow to government securities. Given the Fed’s explicit support for investment-grade and, to an extent, high yield corporate bonds, it is an obvious choice for liquidity to flow into credit markets. Investors seem to agree: all 13 weeks of the second quarter of 2020 saw net inflows for US investment grade corporate bond funds, and 12 out of the 13 weeks had inflows for European investment grade corporate bond funds.3.

Source: Citigroup, as at 30 June 2020. Data for 2020 and 2021 are estimated.

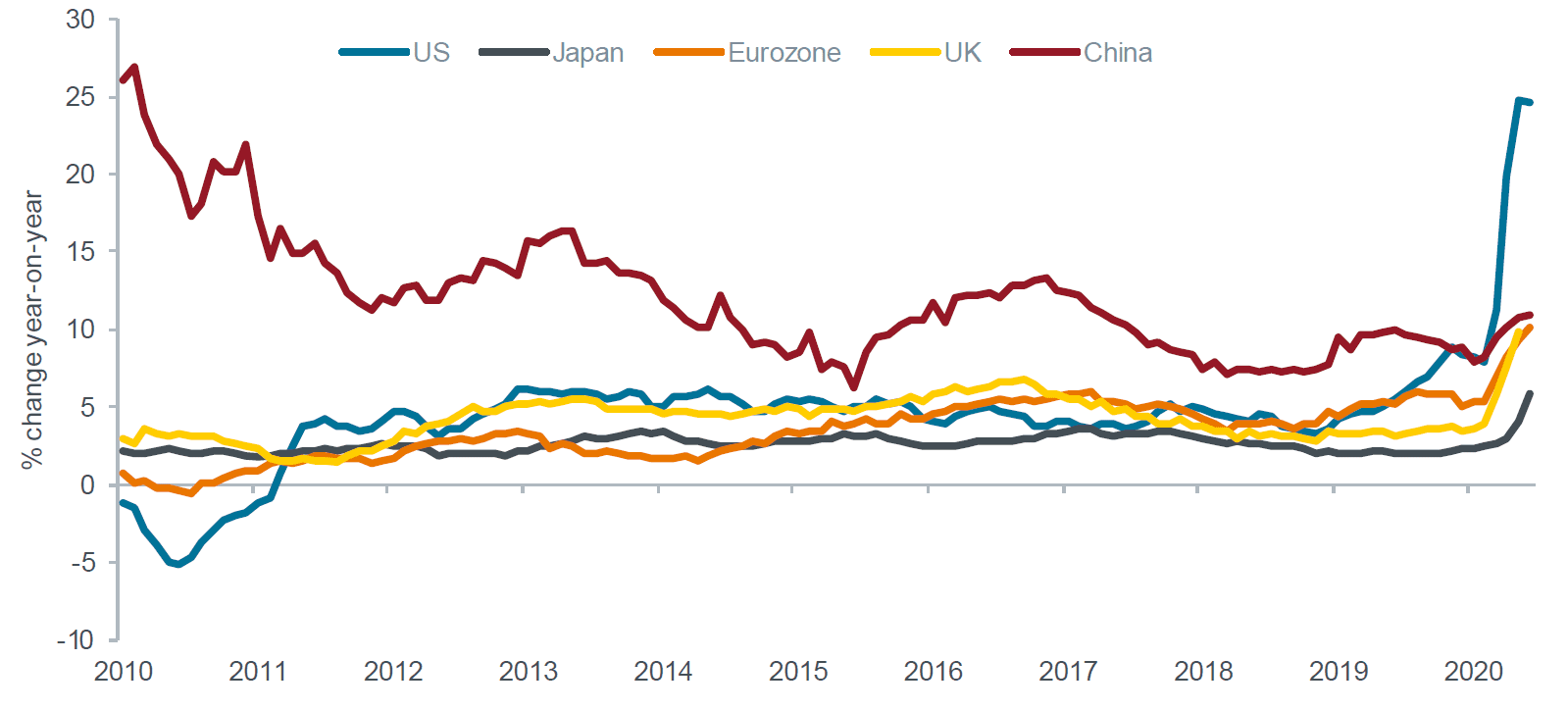

Source: Refinitiv Datastream, monthly datapoints, January 2010 to June 2020.

Financial market inflation complicates valuation. Intervention by central banks, by definition, distorts markets and historic intervention would be expected to create historic distortion. Thus, we are in an unusual, but understandable, period where price volatility and credit spreads have diverged. Current spread levels are usually accompanied by lower volatility and vice versa.

The logical conclusion is that financial markets are being inflated, at least relative to the degree of uncertainty that remains for the world’s economies. Does this mean that markets are overvalued? We don’t think so. Instead, we think credit markets have responded rationally to the restoration of liquidity and the promise of central bank support. But it is difficult to imagine a sustained rally from current levels without a drop in volatility which can be seen as a proxy for confidence, specifically confidence that economic growth will persist. In our view, the speed of the recovery matters less than the direction. As the market becomes more confident that growth will normalise at some point, we think volatility will trickle lower, and spreads will grind tighter.

Credit markets, as we said earlier, have remained relatively stubborn in response to bad news including the recent surge in cases of COVID-19 in the US. While Fed support is largely the cause of this stability, questions still exist. Can markets remain immune? Could credit spreads stay stable if economic activity dips again or if a recovery is pushed back? In our view, the short answer to both is yes. But the magnitude of any setback to growth is important. Should the economy wobble, or its strength wane, we think credit markets would by and large look the other way, though some sectors and securities may be hurt worse than others. In the event of another country-wide lockdown, however, we think aggregate spreads would widen.

Fortunately, there is little evidence this is likely. Instead, we think a ‘muddle-through’ scenario is by far the most likely result of the complicated formula made up of rising cases, regional shutdowns, progress on treatments, and the eventual arrival of a vaccine. We believe that at some point the US economy will normalise, and both the Fed and Congress will do what it takes to shoulder markets until that happens.

If we are correct, we would expect credit spreads to tighten in the months ahead. Markets are forward looking and if they too believe in an eventual economic normalisation, risk ought to be priced lower and spreads ought to tighten. While this could cause the dislocation between current economic data and financial market valuation to become more distorted, that would be par for the unusual course we are on.

The outlook for global economic growth depends on the growth rate of the COVID-19 virus. Should it accelerate to exponential, it is likely that a larger-scale shutdown in the impacted region will be necessary. While this is most likely to occur in the US, infections in Latin America have been climbing steadily and emerging Asia has seen a rise in new cases. However, progress in medical solutions has been rapid, with numerous vaccine candidates in trials now4.. Both the growth rate of the virus and the progress on vaccines must be monitored closely as the effects will have a wide impact.

The US, in particular, is also vulnerable to fiscal support being influenced by politics as the November election draws nearer. While we expect Congress will ultimately provide support to the unemployed and to states facing unexpected budget deficits as a result of the coronavirus, we are aware that politics does not always follow logic. As the market shares our view that fiscal support is likely, a failure to provide it would be a shock to markets, and spreads would likely widen dramatically. Meanwhile, tensions have escalated between the US and China and while we think it unlikely that there will be market-moving geopolitical events before the November election, we acknowledge the risk.

Since the money has to go somewhere, we think credit spreads should find support in this environment, even if economic growth is slow to return.”

In the long term, we believe fundamentals drive market valuations and expect the global economy will see a sustained recovery. In the short term – barring a coronavirus- or politics-induced shock – fiscal policy and central bank stimulus can provide enough fuel to keep economic activity strong enough to support financial markets. Central banks generally are inclined to be slower in removing support than providing it, because they know that it is ultimately less costly to prevent a liquidity problem than to fix one. With inflation below the Fed’s target level in the US, the risk of being too generous in providing liquidity is even less. And since the money has to go somewhere, we think credit spreads should find support in this environment, even if economic growth is slow to return. Absent better-than-expected economic news, spreads might not rally significantly, but the yields offered in the meantime are, in our view, attractive.

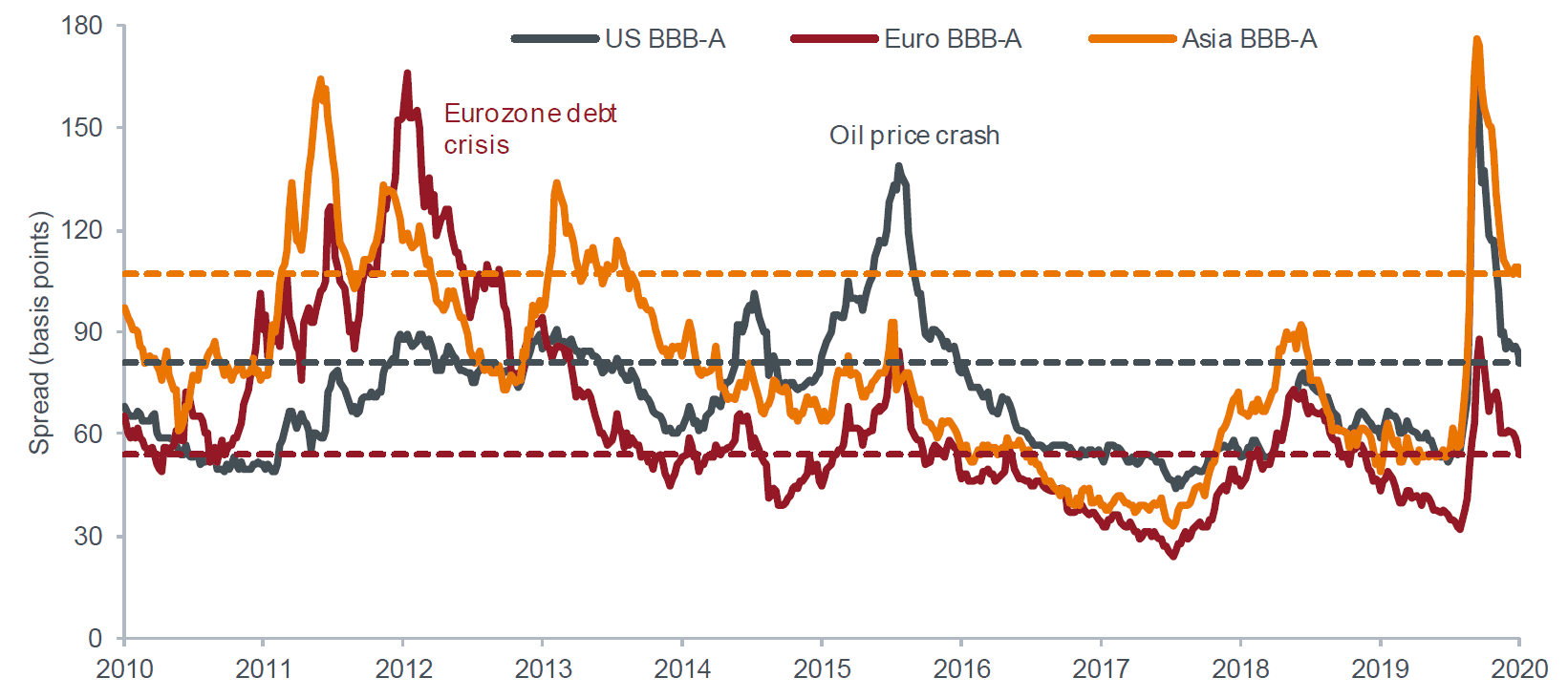

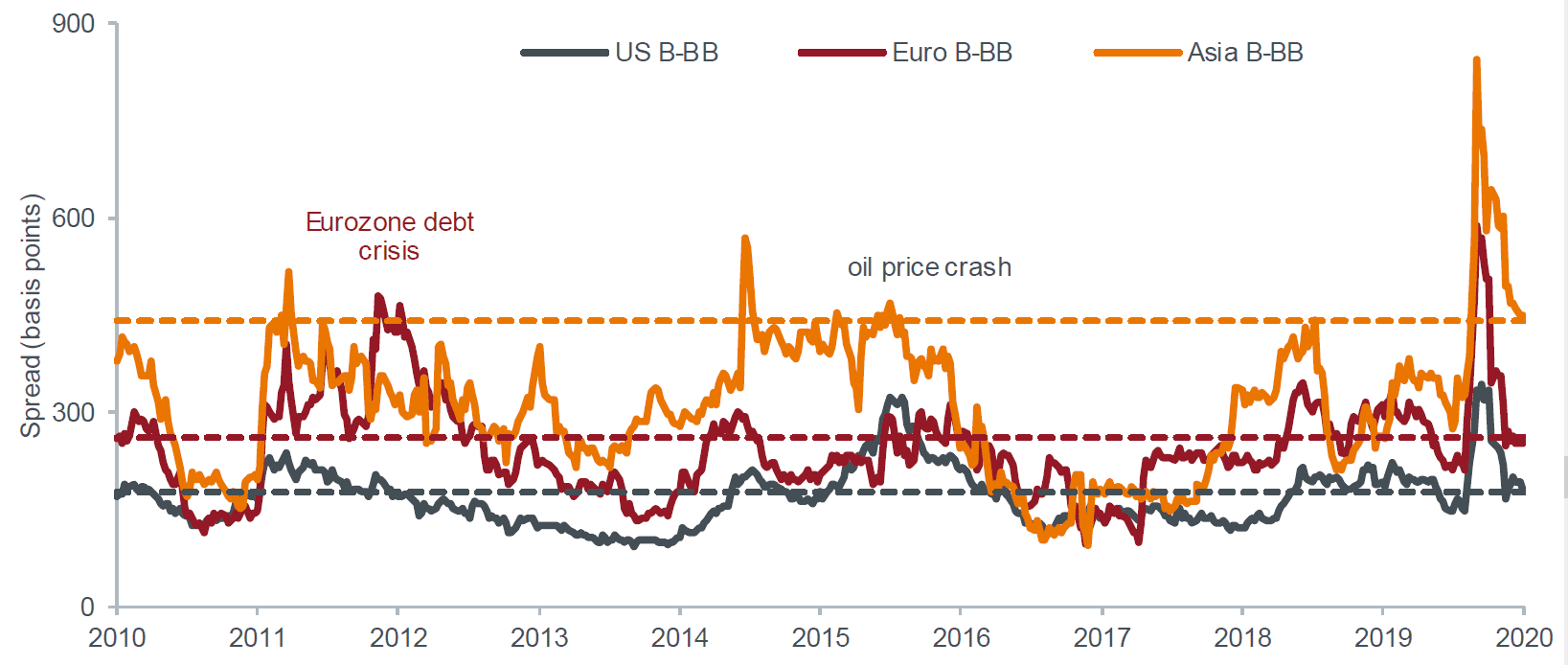

For stronger capital returns, we think investors may have to move along the credit spectrum, where spread differentials remain elevated relative to recent years albeit lower than during some previous crisis episodes (see Figures 5 and 6). This may include taking more risk in the high yield corporate bond markets, the lower-rated segments of the structured securities market, or the emerging markets. However, while the lower credit- quality sectors offer more upside, they also offer more risk insofar as they are – broadly speaking – more susceptible to changes in economic growth, particularly within the more cyclical sectors or commodity- sensitive regions.

Source: Bloomberg, Govt OAS, ICE BofA US Corporate BBB minus ICE BofA US Corporate A, ICE BofA Euro Corporate BBB minus A, ICE BofA Asian Dollar Corporate IG BBB rated minus A rated, weekly datapoints, 23 July 2010 to 24 July 2020. Dashed lines show latest regional figure at 24 July 2020.

Source: Bloomberg, Govt OAS, ICE BofA US High Yield B minus ICE BofA US High Yield BB, ICE BofA Euro High Yield B minus BB, ICE BofA Asian Dollar Corporate HY B rated minus BB rated, weekly datapoints, 23 July 2010 to 24 July 2020. Dashed lines show latest regional figure at 24 July 2020.

1. Source: JPMorgan, Daily Consumer Spending Tracker, 26 July 2020.