Subscribe

Sign up for timely perspectives delivered to your inbox.

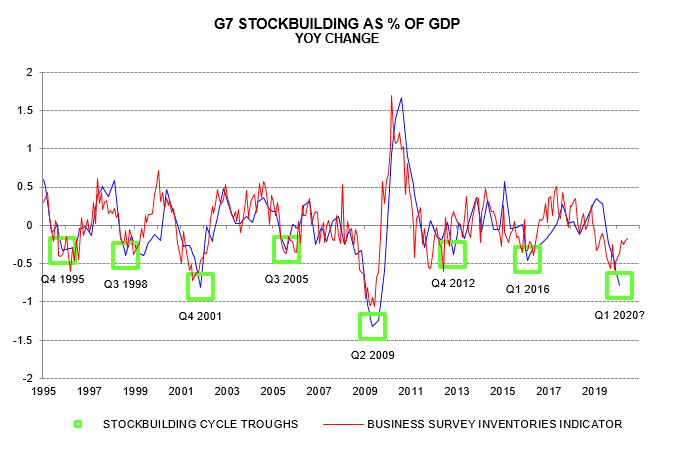

The global stockbuilding (inventory) cycle is judged here to have bottomed in H1 2020, probably Q1. The cycle acted as a drag on global economic momentum in 2018-19 but is now scheduled to provide a tailwind at least through end-2021.

Reasons for believing that Q1 marked the trough include:

1. A low was due – the cycle has averaged 3.5 years and last reached a trough in early 2016. A weakness of the analysis is that it excludes China, the largest industrial economy. Chinese industrial output has rebounded more strongly than retail sales, raising the possibility that stock levels have increased significantly, in turn suggesting that an inventory correction in China could offset a recovery in the G7 cycle.

A weakness of the analysis is that it excludes China, the largest industrial economy. Chinese industrial output has rebounded more strongly than retail sales, raising the possibility that stock levels have increased significantly, in turn suggesting that an inventory correction in China could offset a recovery in the G7 cycle.

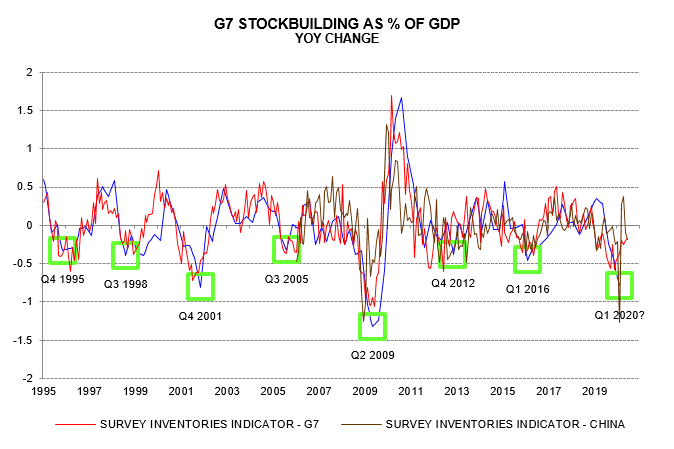

China does not release quarterly national accounts inventories data but a business survey indicator can be constructed along the same lines as for the G7. This indicator has reached peaks and troughs around the same time as the G7 indicator, consistent with the stockbuilding cycle being global – second chart.

The Chinese indicator reached a low in February – further evidence that the global cycle troughed in Q1. It spiked higher in March / April, probably reflecting the production side of the economy reopening ahead of demand, but returned to negative territory in May / June.

The Chinese indicator reached a low in February – further evidence that the global cycle troughed in Q1. It spiked higher in March / April, probably reflecting the production side of the economy reopening ahead of demand, but returned to negative territory in May / June.

The indicator, therefore, does not support claims of a significant inventory overhang. G7 and Chinese stockbuilding cycles appear aligned and should have reinforcing effects on global economic momentum in H2 2020 and 2021.