Knowledge. Shared Blog

June 2020

Beyond the Nadir: What’s Next for Fixed Income

Jason England

Jason England

Portfolio Manager Daniel Siluk

Daniel Siluk

Portfolio Manager Nick Maroutsos

Nick Maroutsos

Co-Head of Global Bonds | Portfolio Manager

Just over two months have passed since global markets dramatically sold off as the COVID-19 pandemic unfolded. There is much talk of the “new normal” in every aspect of our lives, but what does this mean for fixed income? In the following Q&A, Portfolio Managers Nick Maroutsos, Dan Siluk and Jason England answer some of the key questions.

Key Takeaways

- The last few weeks have seen a marked improvement in liquidity, with traders/brokers being more active and prepared to make a two-way market.

- The widening in credit spreads makes credit more attractive from a forward-returns perspective, and Federal Reserve purchasing offers implicit support to sub-five-year investment-grade bonds.

- We believe investors should consider shorter-dated bonds. In the event of a spread-widening episode, these bonds tend to carry lower duration risk and roll back to par value more quickly.

Are global fixed income markets back to “normal”?

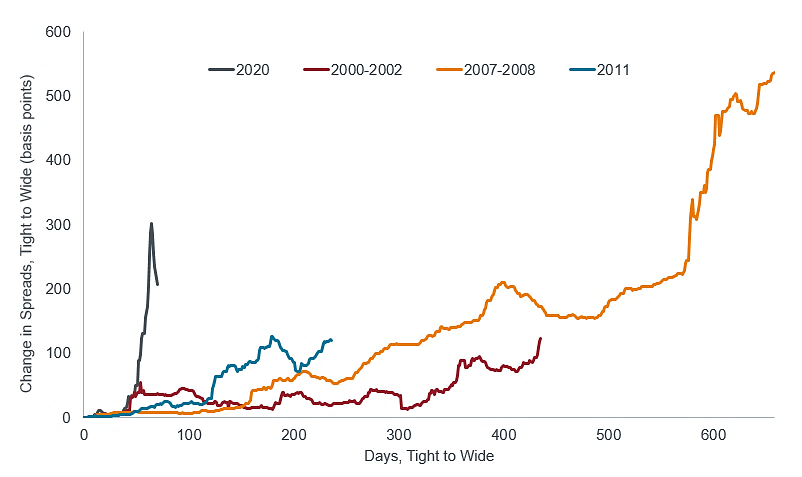

No. But significant improvement has taken place over the past month or more. Bid/ask spreads1 on bonds have started to narrow, and while some sectors are moving closer to more normal levels, challenges remain in certain areas. While “unprecedented” has been a word used extensively over these past several weeks, it is entirely apt in describing the change we saw in credit spreads. The chart below highlights this well compared to prior widening periods.

Rapid Pace of Credit Sell-off (U.S. Investment-Grade Credit Spreads)

[caption id=”attachment_296728″ align=”alignnone” width=”802″] Source: Deutsche Bank, ICE BofA US Corporate Index, government option-adjusted spreads. Data as of 31 March 2020. Option-adjusted spread measures the spread between a fixed income security rate and the risk-free rate of return, which is adjusted to take into account an embedded option. The ICE BofA US Corporate Index represents U.S. dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market.[/caption]

Source: Deutsche Bank, ICE BofA US Corporate Index, government option-adjusted spreads. Data as of 31 March 2020. Option-adjusted spread measures the spread between a fixed income security rate and the risk-free rate of return, which is adjusted to take into account an embedded option. The ICE BofA US Corporate Index represents U.S. dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market.[/caption]

The chart shows U.S. investment-grade credit spreads. The key message conveyed is just how rapidly the sell-off impacted credit spreads. In only a handful of days, spreads rose by more than 300 basis points. In prior widening periods – for example, the Global Financial Crisis – the expansion of spreads was much slower, providing market participants time to increase portfolio defensiveness. Time was a luxury no one had this time around.

What about fixed income market liquidity?

Over recent weeks we have seen marked improvement in liquidity across some investment-grade sectors. A combination of strong central bank action, led by the Federal Reserve (Fed), has improved liquidity, and we have started to see significant improvement in two-way trading and brokers/market-makers being more active. Corporates across most sectors have also started to trade more actively, particularly in the new issue market. In Australia, mortgage-backed securities have historically been less liquid than corporate bonds. However, recent Australian Office of Financial Management actions have provided positive assistance to this segment of the market.

With global government bond yields remaining low and talk of more countries moving to negative interest rates, it has been said that investment-grade credit is the new sovereign. Is this true?

Well yes … and no, depending on how sovereign assets are used in a portfolio. As a hedge to risk assets, we believe that sovereign allocations still offer greater resilience than credit in the event of a risk-off event, so here sovereigns appear superior. However, the dramatic widening of credit spreads in the March-April period had the effect of pushing corporate bond yields higher in relative or absolute terms. This makes credit relatively more attractive from a forward-returns perspective. Put simply, investors can get paid more now to own credit bonds than they did a few months ago.

Furthermore, the Fed’s recent corporate bond programs have served as a backstop to the investment-grade space. While not explicitly backing corporates, providing buying support on assets with five years maturity or less gives investors implicit support.

But is it riskier to own credit today than a few months ago?

Technically – if the market is accepted as an efficient pricer of risk – then one has to say yes. For companies issuing bond debt today compared to a few months back, these firms typically have to pay a higher interest coupon to bond holders. So that means that the market is effectively pricing in a higher degree of risk, right? At a broad market (index) level, it is hard to say otherwise.

Uncertainty over future earnings for companies in so many sectors and industries will undoubtedly lead to problems for some – not just affecting their ability to service debt but also meaning further hits for their equity holders. And sovereign issuers, whose own debt levels are skyrocketing with successive aid and intervention packages aimed at propping up troubled economies, are by no means immune.

So, it has become more important to be selective. To that end, we think investors should avoid so-called BEACH names – booking agencies, energy, airlines and autos, cruise lines, and hospitality (entertainment, hotels, tourism) – given these businesses have higher betas and are likely more negatively impacted by COVID-19. Instead, we’d suggest looking for issuers that have more robust financial structures and greater resilience. We also think maintaining a shorter maturity profile is key in today’s environment, when the bar for central banks to hike interest rates is so high. In addition, shorter-dated bonds should ultimately bounce back to their par value far quicker than, say, a seven-year or 10-year bond, (provided there is no default) in the event of another market sell-off.

Abandon Your Doubts,

Not Your Goals

1Bid/ask spread is the difference between the highest price that a buyer is willing to pay for an asset and the lowest price a seller is willing to accept.

Knowledge. Shared

Blog

Back to all Blog Posts

Subscribe for relevant insights delivered straight to your inbox