Subscribe

Sign up for timely perspectives delivered to your inbox.

Jay Sivapalan, Head of Australian Fixed Interest at Janus Henderson, discusses the credit market and how the team are actively managing the portfolios ahead of a looming de-leveraging cycle.

There’s no doubt that there has been a significant hit to the earnings of corporates around the globe and it is surprising that it isn’t more visible in risk assets like share markets. Against a backdrop of ultra-low defaults in recent years, we expect to see a pickup in defaults from larger firms all the way down to small-to-medium enterprises, but resulting in a default cycle that is quite a bit shallower than experienced through the Global Financial Crisis (GFC) and other crises.

Government intervention has played, and will continue to play, a large role in helping companies to survive, and in the US the Federal Reserve’s actions have had a profound impact on all credit markets around the world. This has resulted in open markets, making access to debt funding very easy at the moment.

To put this in context, in April there was over US$300 billion dollars of corporate bond issuance in the US, which is the largest month on record. Names like Boeing, Vail Ski Resort, Carnival Cruise Line and number of theme parks were among the companies to have accessed debt markets.

For investment grade companies seeking money, they are going to be able to fund it and most are now able to borrow at cheaper rates than they were 12 months ago. Firms with a reason to exist, with intact business models that just need time to get to the other side of this crisis are likely to be able to fund themselves.

Adding further support to businesses is the highly pragmatic approach being taken by the banking system, providing some waivers or leeway for companies not meeting their near-term obligations, instead letting them meet their obligations over the longer-term. In particular, some flexibility around financial covenants.

Where it’s going to hit hardest are the highly leveraged, cyclical businesses, especially those in industries affected by COVID-19 mobility restrictions. In Australia, Virgin Australia is probably the most prominent example that comes to mind in that context and we anticipate that there will be others.

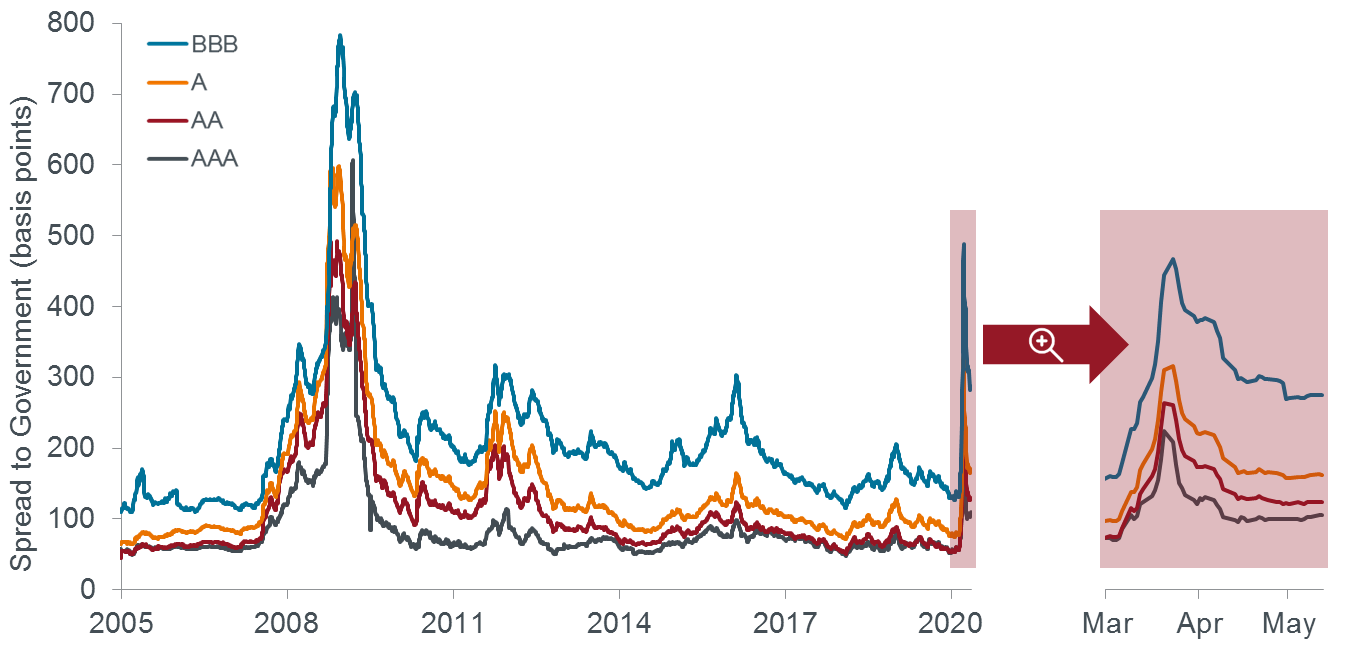

On Chart 1 below, we see credit spreads over time; you can see how sharp the spike in credit spreads was, so obviously this was bad for credit assets. But equally, on the other side of the spike, you can see the early stages of recovery as a result of some of the measures mentioned earlier.

Chart 1: US corporate credit spread by credit rating band

Source: ICE BofAML Indices (US Corporate Master Index), as at 12 May 2020.

The shaded bar alludes to a deep, sharp recession which is typically when credit spreads start performing well. We believe the peak in credit spreads is actually now behind us, though we acknowledge there will be some volatility and risk-off periods ahead.

We have been investing very actively through this crisis and portfolio turnover across some of our Australian Fixed Interest strategies has been 5-7 times higher than experienced in normal market conditions.

We have purchased around $2 billion of assets over this period across a number of sectors including companies like Macquarie Bank, Coles, Toyota, Woolworths and Bank of America just to name a few. With most of these purchases in March itself.

Research and careful security selection is a vital part of our investment process and we have actively engaged with management of these debt issuers to gain a deep understanding of their challenges and plans in order to form a strong investment thesis.

Over the course of our research, we have identified a trend that points to a looming de-leveraging cycle. If this is the case, this represents a once-in-a-decade event for credit markets. It could provide the potential for us to set our portfolios up for a multi-year outperformance – very fertile ground active managers.