Subscribe

Sign up for timely perspectives delivered to your inbox.

Co-Head of Global Bonds, Nick Maroutsos, expresses concerns that the recent rally in riskier assets does not reflect the acute stress felt by small businesses and households during this economic crisis.

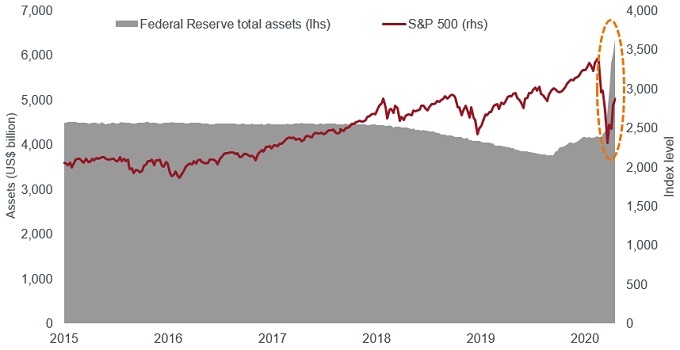

The past two months have been unprecedented, both in the degree to which the COVID-19 pandemic has slashed economic activity and in financial markets’ reaction to the crisis and the policy response it provoked. Despite the virus still spreading, testing likely inadequate and a vaccine at least months away, judging by the recovery in risk assets, one may be tempted to sound the all clear. As of 17 April 2020, US stocks were 28% above their recent lows and the premium commanded for holding investment-grade corporate bonds over the risk-free benchmark declined by 45%. We believe that much of the optimism expressed by this meteoric price appreciation is premature.

Source: Bloomberg, as at 17 April 2020.

While we believe that policy makers have made the right moves in restoring market liquidity, buttressing access to credit and – on the fiscal side – offering support to households and small businesses, US stocks sitting just 15% below their record highs and rapidly narrowing credit spreads assume that the global economy may swiftly return to the pre-COVID-19 status quo. We consider this unlikely, especially for an economy like the US whose growth is dependent upon personal consumption. And with the global economy likely staring at a synchronised recession, trade flows are likely to provide even less of a boost than usual.

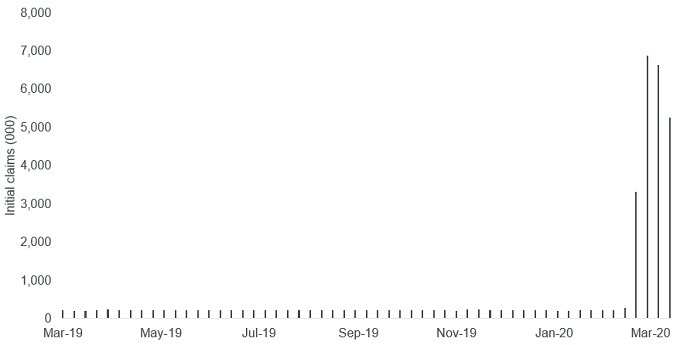

One often hears of the Wall Street versus Main Street disconnect. Lost in the argument is that the prospects of the former tends to reflect those of the latter – especially in a consumption-driven economy. It is the outlook for the real economy that concerns us. According to the US Department of Labor, over the four weeks to 11 April 2020, 22 million workers filed for initial jobless claims; this compares to a weekly average of 217,000 over the preceding year (52 weeks to 14 March 2020). Equally alarming, figures from the US Census Bureau revealed that retail sales including the hard-hit restaurant industry, fell 8.7% over the month in March – a period in which the country was only beginning to issue ‘shelter-in-place’ orders. April data are likely to be far starker.

Source: Bloomberg, US Department of Labor, 23 March 2019 to 11 April 2020.

Markets are at risk of downplaying the stress this curtailment of economic activity will place on near-term corporate earnings. Furthermore, there is a big difference in the economic hit incurred by a three-month, six-month or even nine-month lockdown. Another potential miscalculation is to underestimate the degree to which consumer behaviour will change once the worst of the storm passes. Some activity will simply transition from one medium to another. Do not be surprised if recent adopters of e-commerce are reluctant to return to the status quo of fighting for a parking spot at the grocers. Other behaviours may disappear for the foreseeable future. Despite humans’ social nature, it may take a while before people once again are comfortable in crowded restaurants, cinemas, airports and amusement parks.

The US Federal Reserve (Fed) wading into corporate credit markets – including purchasing debt from so-called fallen angels that have recently lost their investment-grade rating – may throw issuers a lifeline, but it won’t stop defaults. Some industries already face secular challenges, which have likely been exacerbated by this economic disruption. We see greater risk of defaults, however, for small businesses. With these organisations comprising close to half of the US economy and notoriously having limited liquidity, many of these businesses may not make it out the other side. Given the number of Americans employed by small businesses, a surge in their unemployment would quickly transmit pain to other parts of the economy. Accentuating the magnitude of this risk is how quickly initial funding for the Payroll Protection Program in the US ran dry. Accordingly, we expect to see additional upsizing on the already announced monetary and fiscal packages.

Fed Chairman Jerome Powell validated the maxim “don’t fight the Fed” with his recent actions. Another popular investment adage is, “buy what the Fed is buying.” Looking ahead, that appears to be a host of riskier assets. This may appear to be a win/win proposition, where corporations issue new bonds on favourable terms and investors buy securities at still wider than average spreads. One cannot presume, however, that there will not be a divergence between parts of the market the Fed is supporting and parts it is not. While bond markets have rallied on the Fed’s largesse, eventually companies will again be judged on their ability to generate sufficient cash flow to cover their liabilities and to prudently manage their balance sheets.

Source: Bloomberg, as at 17 April 2020.

One sector that faces acute challenges in maintaining financial strength is travel and tourism. We expect that the near-term stress placed on the sector from lockdowns will not entirely subside given likely changes in consumer behaviour. For that reason, we would draw attention to our recent contribution to the market lexicon: we are being wary of trips to the BEACH – Booking agencies, Energy, Airlines and Autos, Cruises and Hospitality.

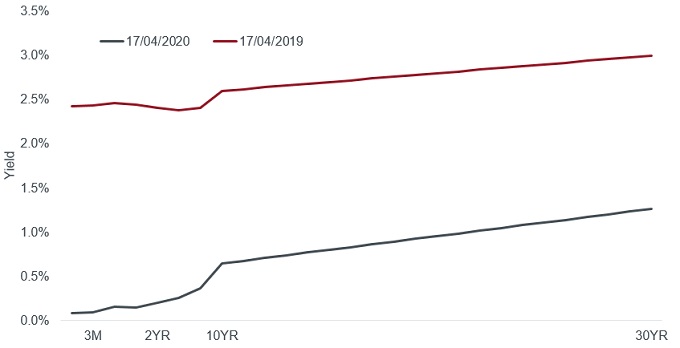

Similarly, the Fed’s activity in Treasury markets does not make these securities a sure thing. Far from it. In the past month, Fed holdings of Treasuries have risen by 45%. That – coupled with the policy rate at the zero bound and the Fed unwilling to go negative – results in very limited upside across much of the yield curve and likely a breakdown in the negative correlation between Treasuries and riskier assets. In fact, the unprecedented balance sheet expansion has injected a steepness in the yield curve that had been lacking for much of 2019. While definitely not our base-case scenario, the Fed’s commitment to hold policy rates low, along with trillions of newly minted dollars, could naturally be construed by some as inflationary. Given this risk, along with the limited upside for intermediate-dated bonds, we believe cautious investors may have little choice but to hide in the front-end of bond markets.

Source: Bloomberg, as at 17 April 2020.