Subscribe

Sign up for timely perspectives delivered to your inbox.

Jay Sivapalan, Head of Australian Fixed Interest at Janus Henderson Investors, brings the team’s investment philosophy to life, describing how they capitalise on market inefficiencies.

The Janus Henderson Australian Fixed Interest team’s investment philosophy is underpinned by the view that markets are inefficient at times and prices will periodically move way from levels that reflect fundamentals or ‘fair value’ levels in our vernacular. Known as ‘market overshoots’, these periods represent opportunities for active managers to add value to clients’ portfolios over time.

Market overshoots can be driven by behavioural factors such as sentiment, fear and greed, through supply/demand dynamics and unconventional central bank policy actions, like quantitative easing, can also play a role.

Key inefficiencies we seek to exploit in these situations are short-termism and the timing and amplitude of monetary policy changes. Given the difficulty of forecasting economic conditions beyond 12 months, the market generally places too great an emphasis on current economic conditions in valuing long-term bond rates. Additionally, as financial markets constantly seek to re-price the short end of the yield curve in anticipation of changes in monetary policy, this leads to regular overshoots where either the market overestimates the timing and magnitude of the move or merely extrapolates the existing trend.

Having developed our disciplined investment process over many years and market cycles, having the experience and skill to identify these opportunities and to wait for markets to unwind has proven to be a profitable approach. Looking specifically at 2019, a number of overshoots appeared within our investment universe and many of the investment strategies executed have begun to deliver for our investors.

In rates markets, the biggest current opportunity we see going into 2020 is the mispricing of expected inflation over the next decade or two.

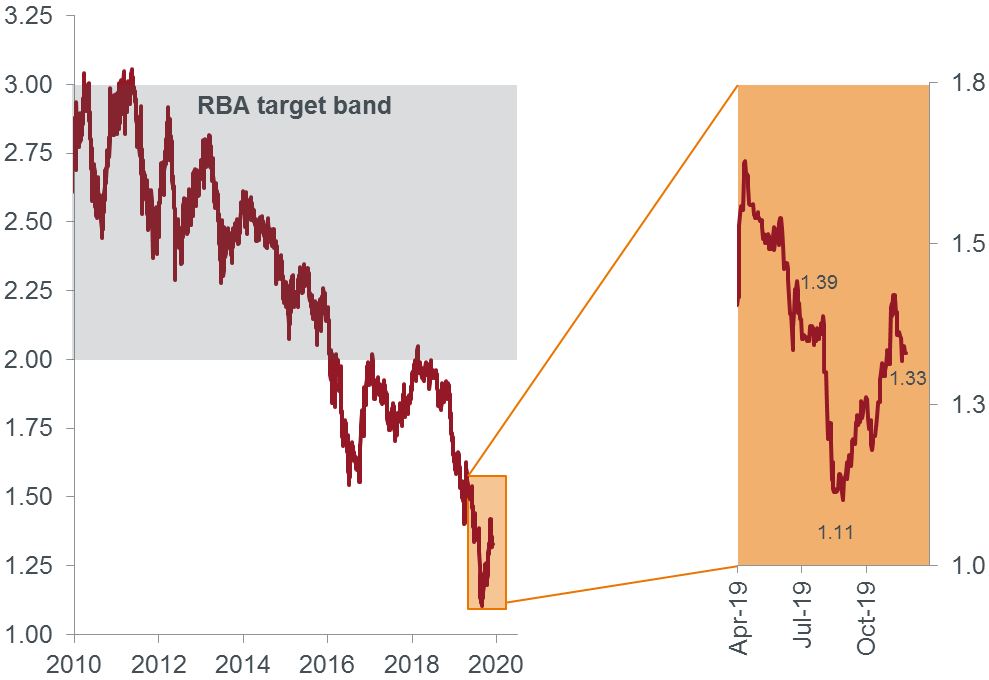

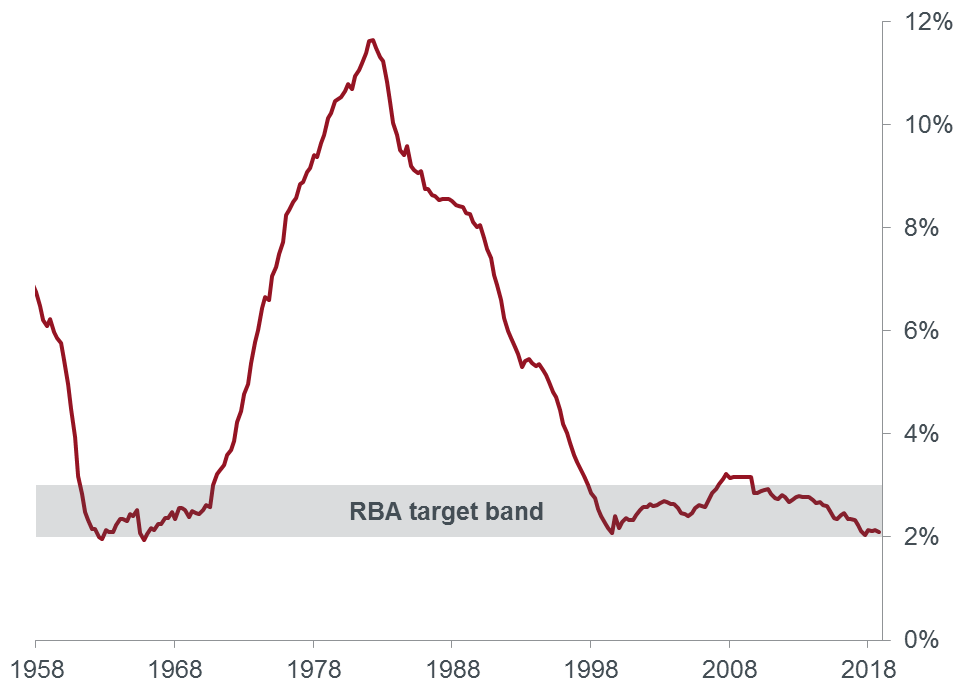

As shown in Chart 1, ten year breakeven inflation rates (the average expected headline inflation over the next decade) fell as low as 1.11% against a Reserve Bank of Australia (RBA) target of 2-3% and recent consumer price index (CPI) prints of around 1.5%. Against this, actual rolling 10 year inflation over the past 70 years in Australia has rarely gone below about 2% as shown in Chart 2.

Chart 1: Breakeven inflation rate

Source: Bloomberg, Australian Bureau of Statistics, Australian Breakeven Inflation Rate to 26 November 2019.

Chart 2: 10 year headline inflation

Source: Bloomberg, Australian Bureau of Statistics, Australian Headline Inflation Rate to 26 November 2019.

This is a classic example of markets taking short-term factors (recent low inflation and sluggish growth) and incorrectly using it to value long-term assets (suggesting current low inflation levels will persist for a decade at even lower levels). In this scenario, markets have discounted any positive impact from easier monetary policy or the prospect of conventional or unconventional fiscal easing. Australia has a floating exchange rate that is variable over time. Expectations for low inflation over a decade implicitly assume a steady to higher currency, a strong assumption given historical experience.

Our valuation and investment processes identified inflation linked bonds as attractively priced, enabling us to add relatively cheap inflation protection to our portfolios. Within all of our mainstream strategies – the Janus Henderson Tactical Income, Australian Fixed Interest and Cash Enhanced funds – we have made allocations to inflation linked bonds which have more recently outperformed nominal government bonds by a solid margin and have been positively contributing to investment performance.