Subscribe

Sign up for timely perspectives delivered to your inbox.

Chinese money growth picked up further in March, supporting expectations of a strong economic bounceback during H2 2020.

As always, narrow and broad money trends are best assessed by focusing on true M1 and non-financial M2 respectively. The headline M1 measure is deficient because it excludes household demand deposits, while M2 can be distorted by large swings in money holdings of financial institutions. The additional details needed to calculate March values of the preferred measures were released today.

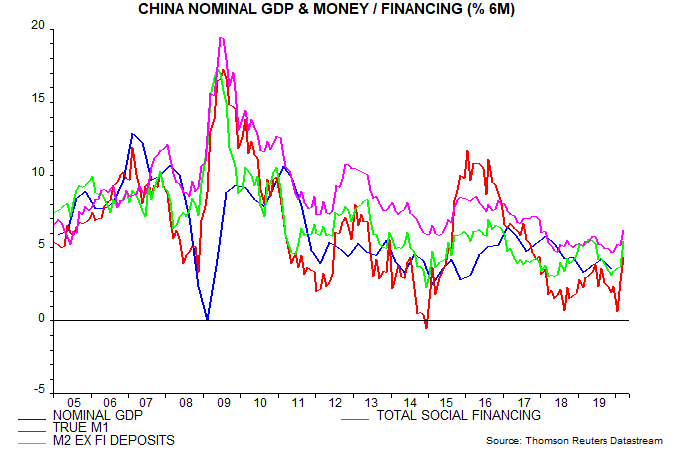

Six-month growth of true M1 rose to 4.4% in March, or 8.9% annualised, the fastest since 2017 – see first chart. Non-financial M2 growth increased to 11.2% annualised. Monetary acceleration has been driven by a pick-up in credit expansion, with the monthly flow of social financing reaching a record in yuan value terms last month.

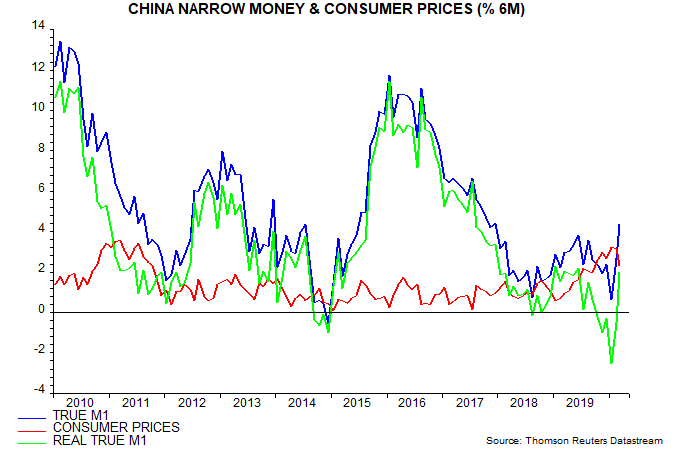

Real money growth has been further boosted by a fall in six-month consumer price inflation, with a further significant decline likely as food prices normalise and the collapse in the oil price feeds through – second chart.

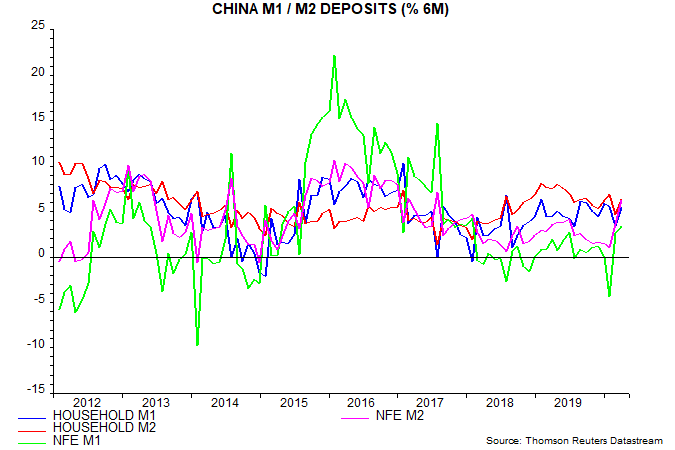

The sectoral breakdown shows that narrow / broad money acceleration reflects a strong recovery in deposit growth of non-financial enterprises, with household deposit growth stable at a normal level by historical standards – third chart. This is encouraging, indicating that policy initiatives to support firms are working, in turn suggesting reduced risk of failures / permanent job losses and improving prospects for business spending.