Subscribe

Sign up for timely perspectives delivered to your inbox.

The market / policy response to the coronavirus shock is expected here to result in a strong pick-up in global narrow money growth, signalling a robust rebound in economic activity in H2 2020 and 2021 assuming Chinese-style virus containment and a gradual loosening of control measures. It may also contribute to a trend increase in broad money growth – this would be consistent with cycle analysis suggesting a medium-term rise in inflation.

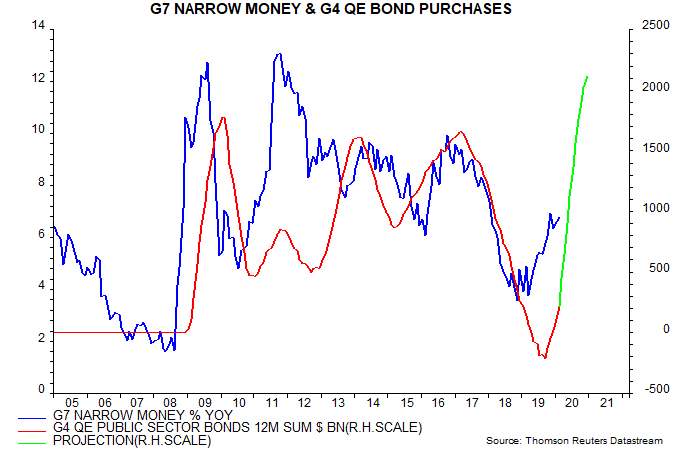

Monetary and fiscal policy measures announced in recent days arguably represent larger-scale stimulus than delivered during the GFC. Interest rate cuts have been smaller but the QE response has been much bigger and faster – see first chart. More importantly, banks are being incentivised / compelled to expand their balance sheets – in contrast to the misguided emphasis on boosting capital ratios during the GFC. The rise in fiscal deficits, meanwhile, is likely to exceed the increase then and may need to be financed by even more QE.

Posts here years ago argued that QE would deliver a smaller boost to broad money growth than claimed by its “monetarist” advocates because of offsetting behaviour by banks under pressure to limit balance sheet expansion. A key offsetting mechanism was that banks sold government bonds as their reserves at the central bank increased – such sales effectively “sterilised” the impact of QE on broad money holdings of households and firms.

The past monetary impotence of QE is illustrated by Japanese experience – the largest bond-buying programme globally in terms of share of GDP failed to shift annual M3 growth out of a 2.0-3.5% range.

With the balance sheet constraint on banks relaxed, however, QE may now have a more powerful impact on broad money. The combination of QE and large-scale fiscal expansion, moreover, implies a direct injection of monetary demand whereas QE alone has an uncertain indirect effect.

Why would a rise in broad money growth carry more significance for medium-term inflation prospects than a narrow money pick-up? For short-term forecasting (six to 12 months ahead) of economic turning points, (real) narrow money gives more reliable signals than broad money. The velocity of narrow money, however, is more variable than that of broad money over the medium term, resulting in a looser relationship between narrow money and trends in nominal GDP and inflation.

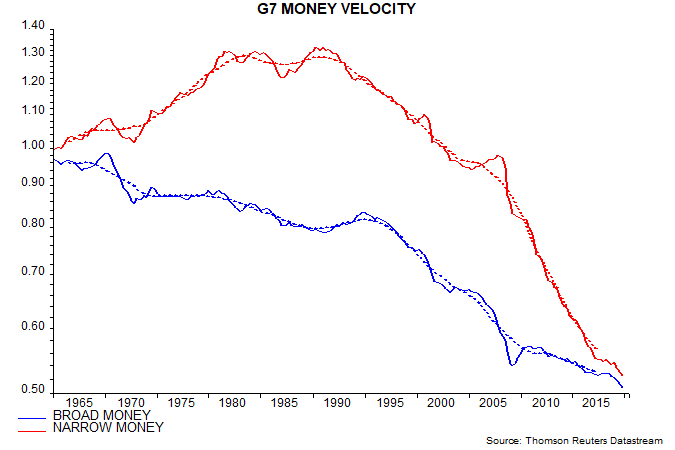

This is illustrated by the second chart, showing G7 narrow and broad money velocity on a quarterly basis and as five-year centred moving averages. Broad money velocity has trended lower since the 1960s, albeit with occasional interruptions in the decline. Narrow money velocity, by contrast, rose between the 1960s and 1980s but fell from the 1990s, with the decline accelerating since the GFC.

The difference in velocity behaviour mainly reflects the greater sensitivity of narrow money demand to interest rate changes. Rising / high rates in the 1970s / 1980s encouraged money-holders to switch out of currency and demand deposits into interest-bearing time deposits and notice accounts, included only in broad money. The shift reversed with the decline in rates from the 1990s, accelerating after the GFC as the interest pick-up for holding money in non-narrow form fell towards zero.

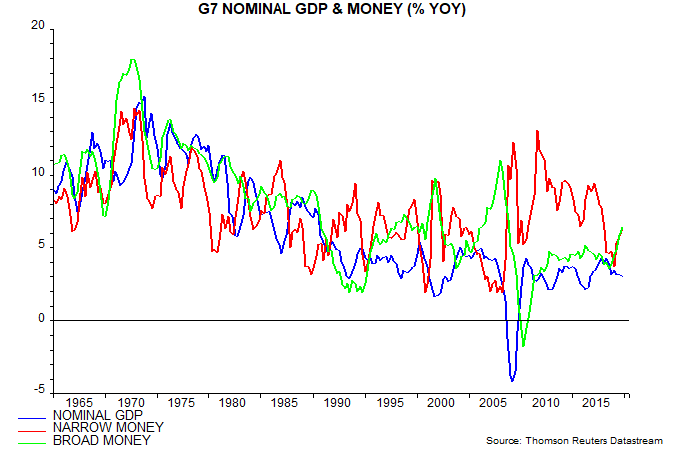

The third chart, showing annual rates of change of nominal GDP and narrow / broad money, illustrates the earlier point that narrow money is better at signalling peaks and troughs in GDP momentum. Broad money trends, however, are a better guide to the medium-term level of nominal GDP growth and, by extension, inflation. Broad money growth displayed a clearer downward trend during the disinflationary 1980s and 1990s and moderate, stable expansion in the 2010s signalled that inflation would remain subdued.

Broad money growth rose during 2019, hinting that medium-term inflation prospects were shifting before the coronavirus shock. A joint surge in narrow and broad money growth would be reminiscent of the early 1970s, ahead of a major upswing in global inflation to a peak in 1975. The judgement here is that this marked the last peak of the approximately 54-year Kondratieff long inflation cycle, which is scheduled to reach another top around 2029.