Subscribe

Sign up for timely perspectives delivered to your inbox.

Following the biggest market sell-off since the Global Financial Crisis in 2008 and volatility not seen since the 1987 crash, we turn to our investment teams for their take on the situation and how they are investing through this evolving crisis.

With the global economy already suffering COVID-19 induced lethargy, the rapid escalation of the virus into a pandemic, along with a supply side oil shock, has shaken markets violently. Together, these factors have delivered a significant shock to all major asset classes.

For three perspectives on this quickly evolving situation, we asked our investment professionals with specialist commodities and energy credentials from the Janus Henderson Diversified Alternatives, Global Natural Resources and Australia Fixed Interest teams for their views on how they are navigating this market event.

Mathew Kaleel, Portfolio Manager

Mathew Kaleel is a Portfolio Manager, Diversified Alternatives at Janus Henderson Investors, a position he has held since 2018. He joined Henderson in 2013 as part of the acquisition of H3 Global Advisors, where he was co-head of global commodities and managed futures. Mathew started at H3 Global Advisors in 1996 and was instrumental in establishing the firm. While there, he managed mandates and proprietary capital on behalf of multiple domestic and international banks, family offices, fund of funds, and pension fund clients. He began his career with Infinity Constructions, working in the project management and quantity surveying departments.

Mathew earned a bachelor’s degree in economics with a focus on accounting and commercial law from Sydney University. Additionally, he received a bachelor of building (project management) degree from the University of Technology in Sydney, graduating with honours. He was named the S&P Emerging Manager of the Year in 2008. He has 25 years of financial industry experience.

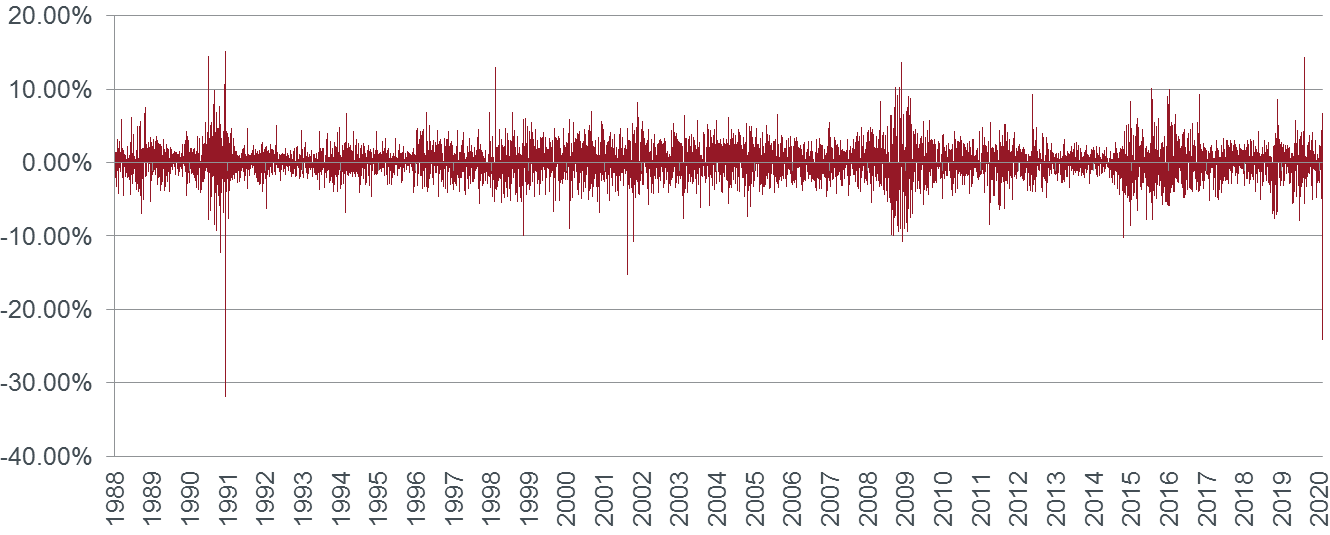

In this rapidly developing market event we are seeing dual shocks play out. While COVID-19 is having a dampening effect on the global economy, disrupting global supply chains and demand, the ‘OPEC+’ (OPEC and Russia) agreement has broken down, with Russia walking away from the agreement and Saudi Arabia announcing its intention to oversupply the market. The collapse in the oil order saw oil reprice approximately 25% in 24 hours, the largest single daily price move since the first Gulf War in 1991.

Chart 1: Nymex Crude Oil Price Change (%)

Source: Bloomberg. As at 10 March 2020.

Oil forward curves are quite effective in absorbing this information, as shown in the chart below. The forward curves for oil at the time of writing (in grey) and the same forward curve from one month ago (in red) show that where the floor in oil prices was pricing at $50 at the front end (i.e. spot oil), this is now effectively a ceiling on prices.

Chart 2: Nymex Oil Forward Curves (US$)

Source: Bloomberg. As at 10 March 2020.

Markets have very quickly priced a lower-for-longer regime for oil prices where potential demand reductions (based upon COVID-19-induced demand shut downs) and the potential for an increase in production drops the price along the whole curve.

With lower prices, higher inventories, and a lack of catalysts for the next 12 months for increased demand, only one thing is certain – volatility will remain elevated and the market will trade towards a price resistance level of US$45-50/bbl. This is in stark contrast to the situation only a month ago where there was confidence that the major players would be disciplined in supporting oil prices above US$50/barrel.

Value can be added in the energy (and broader commodity) space in a number of ways in the current environment, either via more dynamic positioning along the oil forward curve, or where possible, the ability to be over or underweight specific commodities. This includes either being long and short across a commodity forward curve, or being long one commodity and short another.

While energy markets are in a new phase of uncertainty and volatility, this reinforces the need for active, responsive portfolio management in order to navigate through this regime.

Daniel Sullivan Head of Global Natural Resources

Daniel Sullivan is Head of Global Natural Resources and a Portfolio Manager at Janus Henderson Investors, a position he has held since 2019. Previously, he was a portfolio manager and senior resource analyst at 90 West, which Henderson acquired in 2015. Earlier, he worked as an analyst and a portfolio manager at Goldman Sachs, Deutsche Asset Management, Zurich Scudder Investments, and AMP Investments.

Daniel received a bachelor of mining engineering degree (Hons) from the University of Sydney and a graduate diploma of applied finance and investment from the Securities Institute of Australia. He has 31 years of financial industry experience.

Saudi Arabia have very aggressively changed policy, opting for a price war, which raises huge questions about the recent IPO of Saudi Aramco. While this type of total breakdown was discussed within the Global Natural Resources Team, it was considered unlikely given Saudi Arabia is cited as needing an oil price of US$80/bbl to balance its budget.

A knock-on from this event will be weakness for many nations heavily reliant on oil production, along with the possibility of unrest. Meanwhile, consumers globally will have access to cheaper fuels.

With the market already oversupplied and artificially supported by OPEC+, this dual shock of COVID-19 driven demand erosion and unrestrained OPEC+ supply increases has materially altered the oil market. If Saudi Arabia sticks to this strategy, we would expect oil to move even lower from here. To regain market share and pricing power they need to see high cost producers driven out of the market. It is likely that funding and growth of oil shale, oil sands and expensive deepwater projects will be severely impacted. Many energy equities will struggle to remain viable and this will lead to bankruptcies, dividend cuts and production cuts.

We have been neutral to negative on the prospects for oil for a while and have a large underweight position (-13%) to traditional oil & gas. Our total weighting is 17%, so we still have holdings in many other different sub-industries in the portfolio, with gold (about 15% of the portfolio) in particular doing well recently. Whilst cheaper oil may slow some switching to renewables, there is also a case that renewables stable rates of return will become more attractive to energy investors than a struggling traditional oil & gas sector with limited commodity price upside.

Ashley Kopczynski – Associate Portfolio Manager – Credit & ESG

Ashley Kopczynski is an Associate Portfolio Manager – Credit & ESG on the Australian Fixed Interest Team at Janus Henderson Investors, a position he has held since 2019. Before this, he was senior credit analyst. Ashley joined Henderson as a credit analyst in 2015 following Henderson’s acquisition of Perennial Fixed Interest. While at Perennial, he was a credit analyst on the fixed interest team since mid-2008 and a quantitative analyst prior to that. Before joining Perennial in 2007, he spent five years in the corporate superannuation industry at Plum Financial Services, where he was most recently a business development analyst.

Ashley completed undergraduate studies in psychology and business law at Swinburne University of Technology. He earned a graduate diploma in applied finance and investment at Financial Services Institute of Australasia (FINSIA). He holds the Chartered Financial Analyst designation and is a member of the Melbourne CFA society. He has 19 years of financial industry experience.

Despite the prevailing low level of government bond yields, the type of risk-off events we’ve seen in equity and commodity markets often result in increased demand for safe haven assets, such as long duration government bonds as well as strong investment grade corporate bonds.

Diversification becomes your friend during shocks of this nature. If we look at the debt side of companies operating in the oil & gas sector, when we see volatility in bond pricing and weakness in credit spreads of those companies, it reinforces our ‘quality before price’ approach to credit investing and recognition of asymmetric risk. Fortunately our exposure to oil markets across our strategies is minimal – from a fixed income perspective, we don’t see much benefit in lending to single commodity companies as they don’t have the diverse cash flows or strong market positions we seek. It also highlights how ESG risk integration can minimise the risks of adverse outcomes for investors by sharpening our focus on companies that operate in stable regulatory environments with predictable actions by governments.

At times like these, markets can throw the baby out with the bathwater, indiscriminately selling securities in companies, regardless of quality and strength. We are looking to add high quality credit to our portfolios, which we consider are companies that continue to operate with strong market positions with high barriers to entry. These are companies that have demonstrated the ability to survive the sorts of economic and market shocks we are experiencing at the moment.

Credit market “shocks” often occur in combination with a lack of liquidity in the corporate bond market leading to wider than usual bid/offer spreads. This can create opportunities for investors who are able to deploy cash and take advantage of this market dynamic.

As an active funds manager, our investment teams have the ability to manage their portfolios through periods of market volatility and uncertainty. With strong investment talent across all major markets and the experience of investing through multiple market cycles, our teams take a long-term approach, aiming to preserve capital in volatile markets, while actively identifying investment opportunities.

At Janus Henderson, we believe in the sharing of expert insight for better investment and business decisions. We call this ethos Knowledge. Shared.

Without the restriction of a house view, our teams have the freedom to generate their own approach. The combined knowledge of our teams globally is shared across the business to equip our teams with a huge breadth of perspective, helping them make the best decisions for our clients.

Our commitment to this ethos means we will make every effort to share our investment insights with you, through this market turbulence and beyond.