Subscribe

Sign up for timely perspectives delivered to your inbox.

Jay Sivapalan, Head of Australian Fixed Interest, describes how the Janus Henderson Australian Fixed Interest Team are closely monitoring and responding to the Coronavirus’ impact on the market and how active management can preserve capital and identify opportunities in periods of market dislocation.

One need look no further than your local supermarket to see that fear around the spread of Coronavirus and its potential disruption to global supply chains is beginning to pervade markets and the wider population. Non-perishable pantry items, paracetamol, sanitizer and toilet paper have been stripped from the shelves as panic set in. While the supermarket hysteria may turn out to be a short-term phenomenon, the impact of this outbreak on global markets and its severity remains to be seen.

With such dramatic developments unfolding, the Janus Henderson Australian Fixed Interest Team (the Team) has been closely monitoring the situation and its impact, while actively managing our strategies’ portfolios.

Our strategies went into the current market dislocation in a defensive manner and have therefore weathered markets reasonably well. While so far the market reaction has been sharp in certain pockets, in other areas it has been virtually uninterrupted.

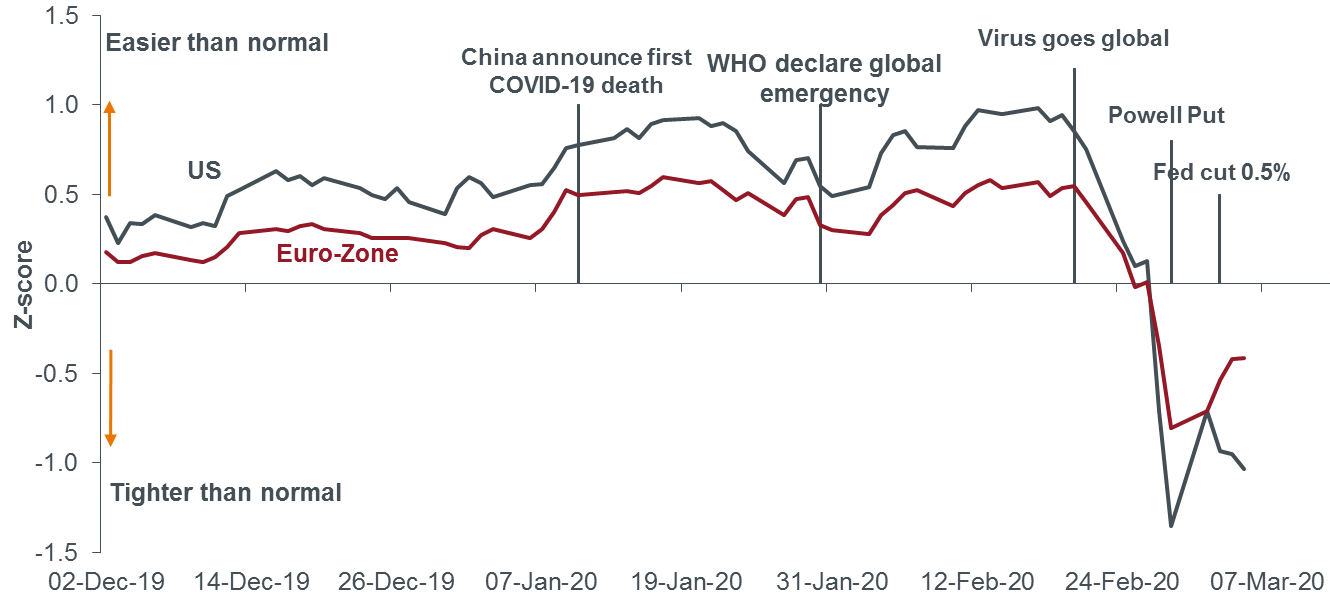

In order to contain the economic impact, on 3 March, the Reserve Bank of Australia (RBA) cut the cash rate by 25 basis points (bps), to an all-time low of 0.50%, while, the US Federal Reserve (Fed) made an emergency rate cut of 50bps. Central banks have recognised the tightening financial conditions, committing to provide whatever support is necessary to arrest the deterioration in conditions.

Chart 1: Financial conditions indices for the US and Euro-zone

Financial conditions implode as virus breaks out, central banks get involved

Source: Bloomberg Financial Conditions Indices for the US and Euro-zone, daily to 5 March 2020.

While acknowledging that it is a rapidly evolving situation, requiring constant observation, the Team have been assessing the economic impact of Coronavirus to identify the market dislocations and investment opportunities for the strategies.

We recognise that market events like this can be confusing and scary for our clients and that any colour we provide could provide insight into how their money is being prudently invested through the crisis.

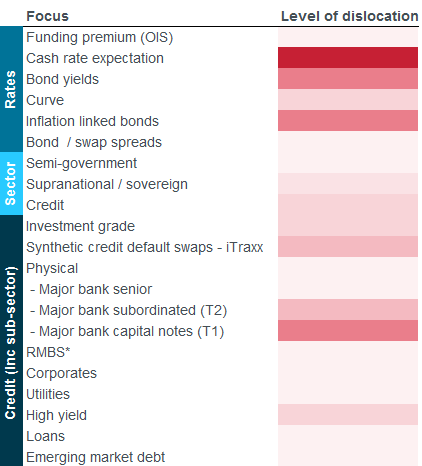

Where we see dislocations in market pricing and potential opportunities for risk-taking are shown illustratively below, with the darker shading representing greater dislocation and lighter shading representing limited or no dislocation:

Table 1: Team’s assessment of the market dislocation

Table is for illustrative purposes only, showing the Team’s assessment of the severity of the market dislocations. *Residential Mortgage Backed Securities.

Our assessment of the market so far is that the dislocation is not yet widespread (as typically characterised by indiscriminate selling) and we are very focused on early moves in portfolios. We are keeping plenty of powder dry for further dislocation, should it occur, and continue to monitor closely.

We have executed trades immediately in the area of cash and bank bill futures, duration (or interest rate risk), supranational debt, Tier 2 debt and hybrids and we have removed the credit default swap (CDS) hedge.

Tactical Income Fund

Australian Fixed Interest Fund

Diversified Credit Fund

Conservative Fixed Interest Fund

Cash Fund – Institutional

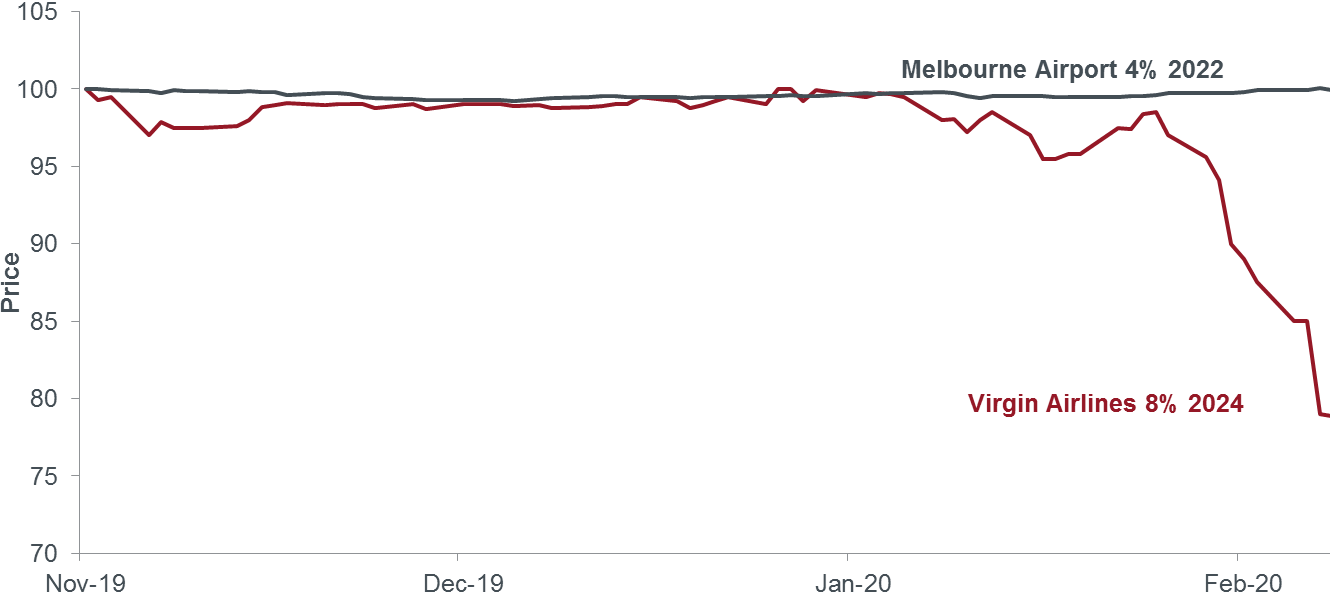

Robust security selection, a quality before price mind-set and a deep understanding of the factors driving the outlook and expectations are vitally important. Price performance over the past fortnight on shorter maturity corporate debt in the transportation sector shows how truly defensive issuers fare relative to more cyclical businesses during a crisis.

As shown in Chart 2, Virgin Australia (ASX:VAHHA) has seen its bond price fall sharply in response to the crisis relative to Melbourne Airport’s bond.

Chart 2: Bond prices Virgin Australia and Melbourne Airport

Source: Bloomberg. As at 2 March 2020. Price chart is normalised data with both bonds starting at $100 from the listing date of the Virgin bonds).

In a rapidly changing market environment, knowing when and what proportion to allocate across the spectrum of asset classes open to a fixed interest investor is not a simple process.

As active fixed interest managers the Team and I are able to tactically allocate to our portfolios, identifying opportunities to capitalise on market mis-pricings, while seeking sources of returns uncorrelated to growth assets.