Subscribe

Sign up for timely perspectives delivered to your inbox.

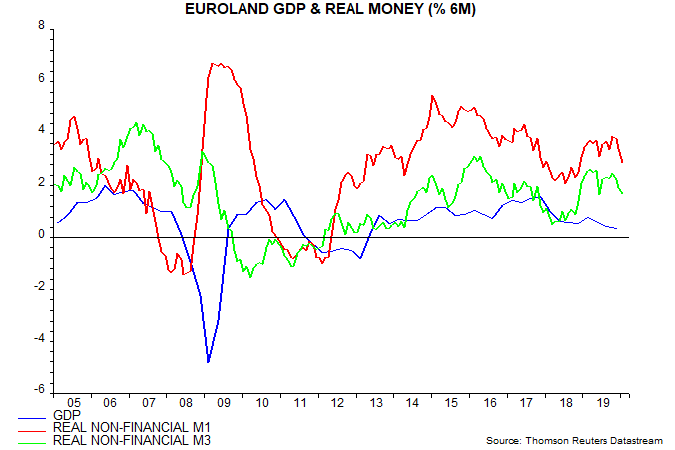

Euroland money numbers for January provide further evidence that the global monetary backdrop was deteriorating before the coronavirus shock. Six-month growth of real non-financial M1 fell to a 14-month low and has now retraced more than half of its recovery from a low in August 2018 to a peak last October – see first chart.  The recent decline mainly reflects a slowdown in nominal money, although six-month consumer price momentum has edged up since October – second chart.

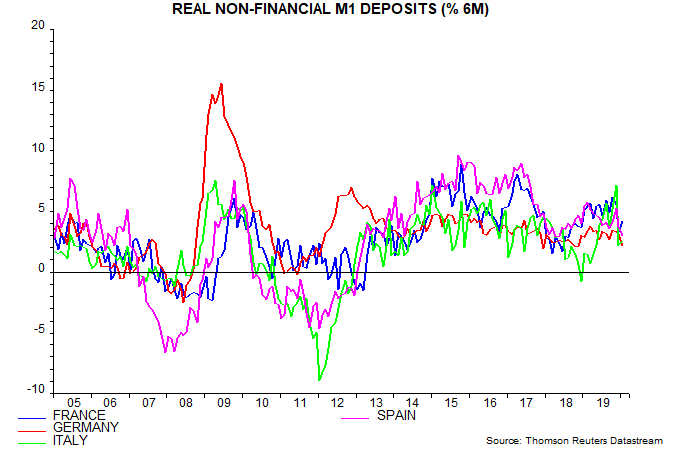

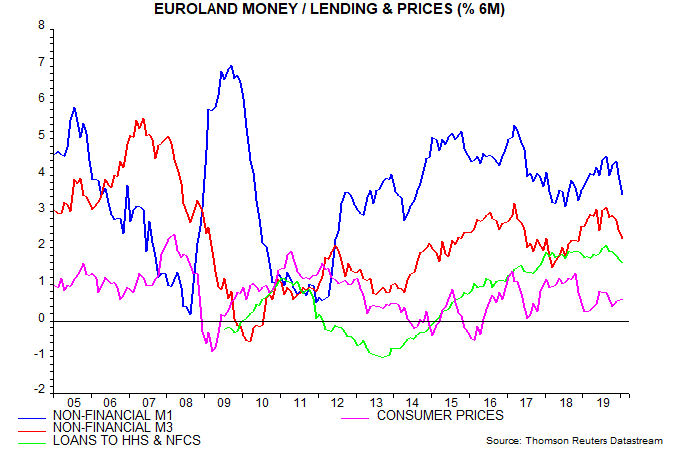

The recent decline mainly reflects a slowdown in nominal money, although six-month consumer price momentum has edged up since October – second chart.  Incorporation of the Euroland number brings down the estimate of global (i.e. G7 plus E7) six-month real narrow money growth in January to 1.7%, a six-month low – see previous post. The estimate will be firmed up following release of January data for Russia, Mexico, Canada and the UK, as well as final Chinese numbers, on Friday / Monday. The pick-up in Euroland real money growth in early 2019 was the basis for a forecast that economic momentum would recover in late 2019 / early 2020. PMI developments were consistent with the story through January but weak December money numbers prompted a negative reassessment. The monetary slowdown is likely to reflect the back-up in Euroland market rates during H2 2019 – a market-weighted average of 10-year government bond yields rose by 50 bp between August and December. With much of this move now reversed, money numbers are expected to improve, perhaps as early as this month. Country level deposit data indicate that the January decline in six-month real narrow money growth was driven by Germany and Spain, with minor recoveries in France and Italy following recent steep falls – third chart.

Incorporation of the Euroland number brings down the estimate of global (i.e. G7 plus E7) six-month real narrow money growth in January to 1.7%, a six-month low – see previous post. The estimate will be firmed up following release of January data for Russia, Mexico, Canada and the UK, as well as final Chinese numbers, on Friday / Monday. The pick-up in Euroland real money growth in early 2019 was the basis for a forecast that economic momentum would recover in late 2019 / early 2020. PMI developments were consistent with the story through January but weak December money numbers prompted a negative reassessment. The monetary slowdown is likely to reflect the back-up in Euroland market rates during H2 2019 – a market-weighted average of 10-year government bond yields rose by 50 bp between August and December. With much of this move now reversed, money numbers are expected to improve, perhaps as early as this month. Country level deposit data indicate that the January decline in six-month real narrow money growth was driven by Germany and Spain, with minor recoveries in France and Italy following recent steep falls – third chart.