Knowledge. Shared Blog

February 2020

COVID-19: Assessing the Impact on Property Markets

Tim Gibson

Tim Gibson

Co-Head of Global Property Equities | Portfolio Manager Guy Barnard, CFA

Guy Barnard, CFA

Co-Head of Global Property Equities | Portfolio Manager

Xin Yan Low, Guy Barnard and Tim Gibson from the Global Property Equities Team discuss the current impact of the coronavirus outbreak and how it is playing a part in the evolving real estate landscape.

Key Takeaways

- Property equities have been resilient, outperforming general equities since the start of the virus outbreak.

- Unsurprisingly, markets and sectors related to retail and tourism have been impacted the most.

- An indirect consequence has been the increased demand for flexible workspace and improved connectivity.

At the time of this writing, the COVID-19 coronavirus has infected more than 75,000 people worldwide, bringing China and other countries in Asia to a near standstill. While we have no particular insight into how this will play out, the impact is already causing significant disruption on the demand side through business and consumer activities, as well as global supply chains.

There may well be unintended consequences that will only become clear with the benefit of hindsight. The key point to focus on is not necessarily the severity of the virus but its duration: In our opinion, this is what will have the greatest impact on the global economy.

What Is the Current Impact on the Real Estate Sector?

Equity markets turned “risk off” in the middle of January, with the outbreak of the COVID-19 virus curtailing any hopes of a recovery in global macroeconomic growth. The defensive nature of property equities has helped the sector outperform general equities globally, as well as in Asia, since the outbreak began.1 Closer to the eye of the storm, Asian equities have lagged most other markets, particularly Hong Kong, which has borne the brunt of the market sell-off.

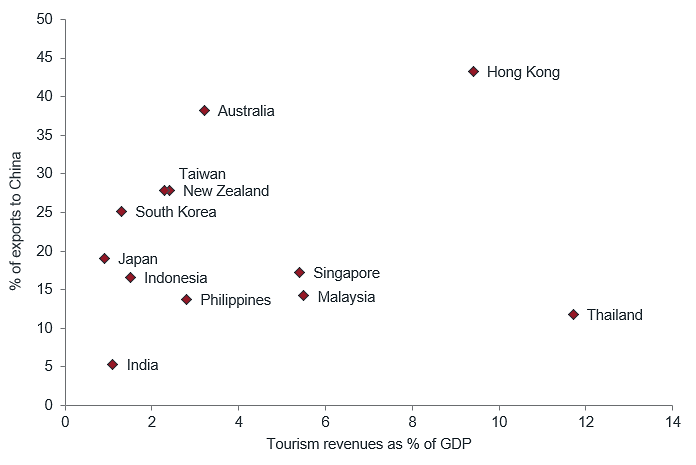

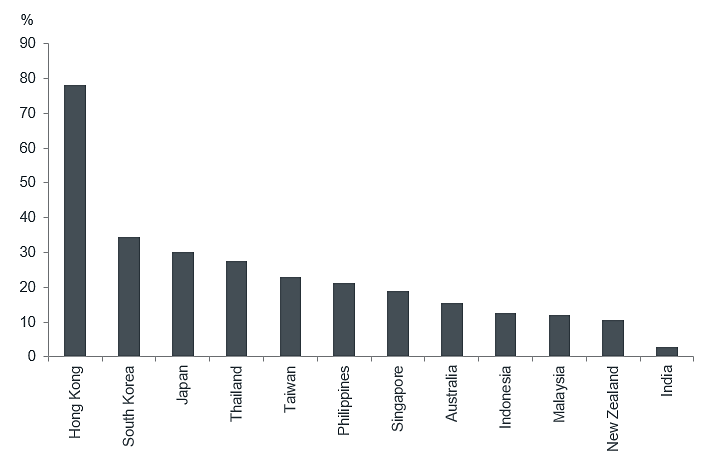

On the ground, markets and sectors related to retail and tourism have seen the greatest impact. The following charts highlight the importance of China to its Asian neighbors in terms of trade and tourism:

Asia Pacific: Trade and Tourism Links to China in 2019

[caption id=”attachment_272729″ align=”alignnone” width=”696″] Source: IMF, UN Comtrade, OECD-WTO TiVA database and CEIC as of 12/31/19. Tourism revenues are 4Q sum to September 2019 for all countries except Thailand (June 2019) and Malaysia (December 2018). [/caption]

Source: IMF, UN Comtrade, OECD-WTO TiVA database and CEIC as of 12/31/19. Tourism revenues are 4Q sum to September 2019 for all countries except Thailand (June 2019) and Malaysia (December 2018). [/caption]

Asia Pacific: Total Tourist Arrivals from China in 2019

[caption id=”attachment_272740″ align=”alignnone” width=”724″] Source: Nomura as of 12/31/19. Note: For Australia, data is shown 4Q sum to September 2019; for India, data is shown for 2018. [/caption]

Source: Nomura as of 12/31/19. Note: For Australia, data is shown 4Q sum to September 2019; for India, data is shown for 2018. [/caption]

Hotels that derive a large proportion of their business from Chinese and/or business travelers have seen a significant decline in occupancies and future bookings. In countries where the virus has spread within the community, people have been staying home and avoiding crowded areas. This has resulted in reduced foot traffic in retail malls while retailers skewed toward luxury spending have seen a meaningful decline in sales. Some landlords have been pressured into bearing some of the loss of income from their tenants and have offered various forms of rental concessions.

In Hong Kong, pro-democracy protests plagued the city for much of the second half of last year, dampening business and consumer sentiment. As such, the virus outbreak is creating a double whammy and prolonging weakness in most property areas there.

Driving the Need for Flexible Workspace and Improved Connectivity

Above and beyond the more obvious and direct impacts, there may be some medium- or longer-term implications for the property sector. Across Asia, the coronavirus outbreak has led many companies to roll out different forms of remote working plans, which is highlighting the viability of flexible workspace solutions and could change the way businesses think about their physical office space requirements in the future. The surge in online shopping and data connectivity, as people stay and work from home during this period, also supports continued demand for underlying infrastructure, such as logistics space and data centers.

Given these implications, we think investors should continue to focus on sub-sectors within real estate that stand to benefit from structural tailwinds, such as technological advances and changing demographics. For example, the logistics/industrial sub-sector and “non-core” specialty sub-sectors, such as data centers, cell towers and manufactured housing communities, may represent areas of opportunity, whereas investors should be very selective in the retail and office space.

It will take time to assess the full impact of the COVID-19 virus on the global economy and the property sector. Potential policy responses by governments and central banks will keep the situation fluid and potentially volatile.

The COVID-19 outbreak is causing some indirect consequences on real estate by accentuating the changing tides driven by technology advances and changing lifestyles, which are altering the demand and usage for real estate. With many uncertainties on the horizon, an allocation to property equities within a balanced portfolio may be beneficial, given the asset class has historically offered lower correlations to general equities and bonds, as well as a lower beta versus general equities.2

Abandon Your Doubts,

Not Your Goals

1Source: Refinitiv Datastream. FTSE EPRA NAREIT Pure Asia Total Return Index (Asian property equities), FTSE World Asia Pacific Total Return Index (Asian equities), FTSE EPRA NAREIT Developed Total Return Index (global REITs), MSCI World Total Return Index (global equities) in USD from 12/31/19 to 2/18/20.

2Source: EPRA, monthly statistical bulletin as of 12/31/19. Comparative total return correlation versus global bonds and global equities. Factset; FTSE EPRA NAREIT Developed Total Return Index beta versus MSCI World Index from December 2010 to December 2019. Beta measures a stock’s volatility in relation to the broad market.

Knowledge. Shared

Blog

Back to all Blog Posts

Subscribe for relevant insights delivered straight to your inbox