Subscribe

Sign up for timely perspectives delivered to your inbox.

With negative yielding bonds peaking at more than US$17 trillion, Shan Kwee, Portfolio Manager – Credit at Janus Henderson Investors, discusses why fixed interest investors need to carefully weigh up the risks of preserving their levels of income.

Just five years ago, the level of negative yielding global debt was zero. At that time, at least 40% of the bond market offered investors more than 5% yield. Today, available income has evaporated, with just 5% of the public debt markets offering a yield of 5% or more. This is a rather narrow pond to fish in and one that is more than likely occupied by a few piranhas.

With the Reserve Bank of Australia (RBA) lowering rates to a record low cash rate of 0.75% and signalling further cuts, fixed interest investors accustomed to yields of 3% or 4% are faced with a decision. Either recalibrate income expectations in light of a lower yield environment, or move out along the risk curve to maintain a higher level of income.

This risk/reward trade-off brings the role of fixed interest within an investor’s portfolio into sharper focus. Fixed interest assets play a defensive role, typically providing a counterbalance to other higher-risk assets, while delivering a regular income stream. High quality income assets with duration are often referred to as ‘portfolio insurance’ for this reason.

Table 1: Sector returns during equity market drawdowns (%)

| Period | Shares | Bonds | High Yield |

|---|---|---|---|

| September 1987 to February 1988 | -43.5 | 5.1 | 6.9 |

| July 1990 to December 1990 | -16.2 | 9.9 | -8.9 |

| May 1992 to October 1992 | -13.5 | 4.3 | 4.2 |

| June 2001 to September 2001 | -12.0 | 4.3 | -4.7 |

| January 2002 to February 2003 | -15.0 | 10.3 | 1.8 |

| October 2007 to February 2009 | -48.3 | 15.5 | -26.5 |

| March 2011 to September 2011 | -15.5 | 7.1 | -5.4 |

| February 2015 to February 2016 | -12.2 | 3.0 | -8.5 |

| August 2018 to December 2018 | -9.9 | 1.8 | -4.1 |

| Event averages | -20.7 | 6.8 | -5.0 |

Source: Janus Henderson Investors, Bloomberg, Shares = All Ords Accum, Bonds = Bloomberg Ausbond Composite Bond Index (All Maturities) previously UBSA Composite (All Maturities), US High Yield = ICE BofAML US High Yield Master ll.

However, investors that target higher yielding income investments are being compensated for taking on more risk. I’m sure we’re all familiar with the phrase “there’s no such thing as a free lunch”. Issuers reward these investors with higher rates of interest in exchange for taking on a greater risk of default and price volatility for holding assets with poorer liquidity, capital subordination, structuring complexity or lower credit quality.

While each investor will have their own risk tolerance, over-exposure to riskier, higher yielding assets can compromise the level of ‘portfolio insurance’ that higher quality and more liquid income investments can offer, albeit at a lower yield.

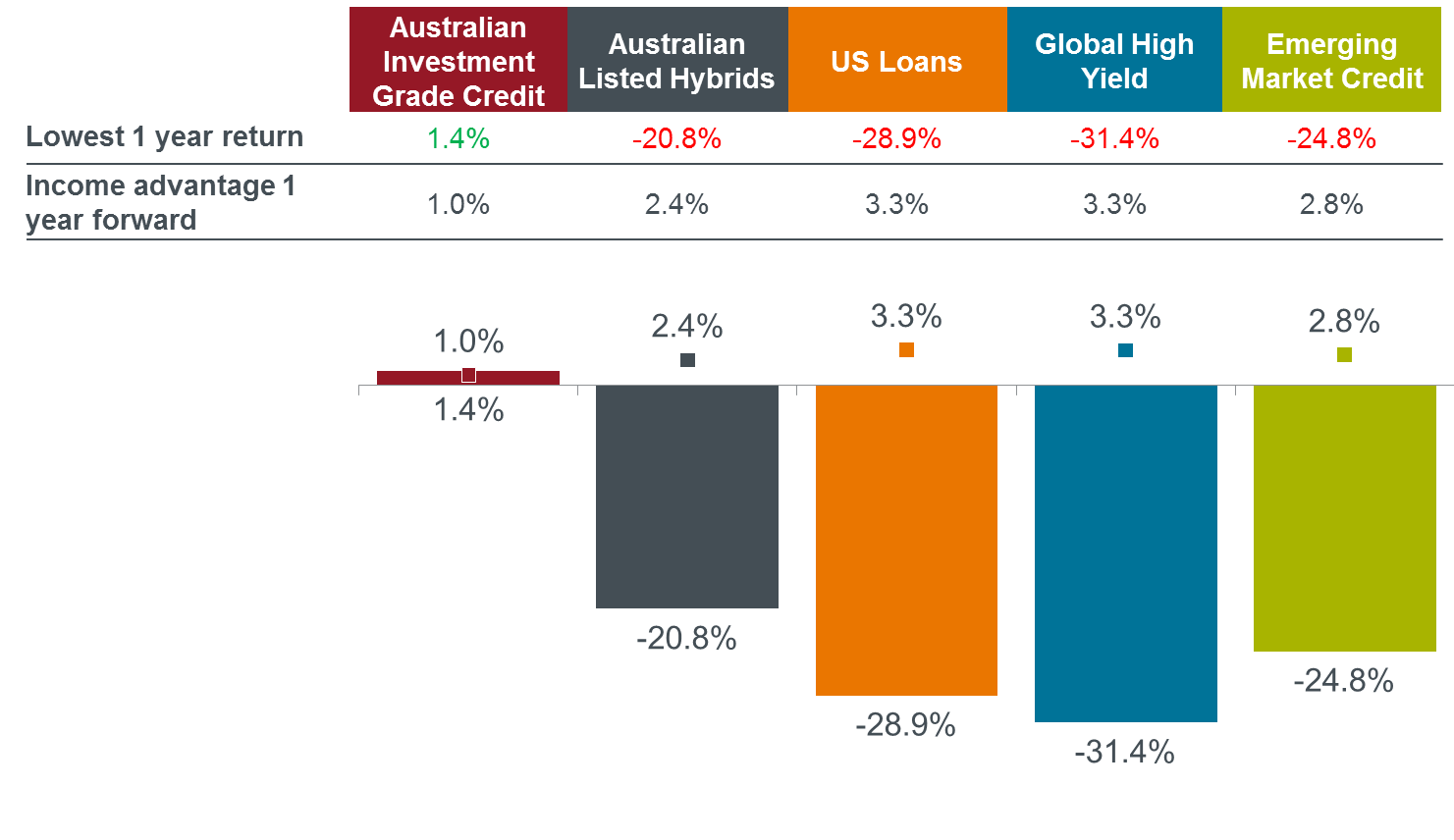

Chart 1: Lowest 12 month return 2003 – 2019

Source: Janus Henderson Investors, Aust IG Credit = Bloomberg Ausbond Credit Index, Aust Hybrids= Evans & Partners ASX Listed Hybrids (including franking), US Loans = S&P LTSA YS Leveraged Loan Index, Global High Yield = BofAML ICE Global High Yield Constrained, EM = JPMorgan CEMBI Broad. Returns Australian dollar hedged as at 31 October 2019. Income advantage takes into account the yield on offer, expected default probability, and loss given default.

While 10-year government bonds provide around 1% yield, there are reasonable opportunities in credit markets that enhance income, while still preserving the core defensive characteristic of a fixed interest allocation.

Given our quality before price mindset, we believe that in the current environment the most attractive assets have shorter tenors and are investment grade, so investors can rely on the benefit of additional income from credit spreads without bearing undue risk.

For investors seeking greater liquidity and capital preservation, assets such as investment grade bonds issued by Australian corporates, infrastructure owners and Real Estate Investment Trusts (REITs) more than double the available income above government bonds, with strong covenants and very low default risk.

Investors that can withstand greater price fluctuations and do not foresee a need to draw on their capital can adjust their risk appetite in search of higher income from credit markets. However, as we look down the risk spectrum, the available risk/reward profile becomes less appealing as the additional yield compensation has been compressed in this low yield environment.

As we noted above, the universe of higher yielding income opportunities has narrowed. Investors looking for yields of 3% or more can consider sub-investment grade bonds or bank hybrids that carry additional credit and liquidity risk, and the resultant tail risk of capital drawdown generally at the same time that equity prices are falling.

For those markets further down the credit and liquidity spectrum that may promise 5% yield or above, there is a very real risk that investors may not be able to redeem all their capital in more stressed markets. This represents only a fraction of public debt markets and the smaller private and illiquid debt pool. Changes in the regulatory capital frameworks in Australia for total loss absorbing capacity (TLAC) and the Reserve Bank of New Zealand’s announced changes from their Capital Review will see much higher levels of issuance of subordinated and capital instruments where investors take on equity conversion risk.

Investors also need to adjust their expectations for the return to be lower than the ‘advertised’ market yield. This is because defaults occur more regularly in these markets, which act as a more meaningful drag on returns. Active management is paramount to understand the individual risks of these securities and to demand appropriate compensation.

In an unprecedented global environment of low or negative yields, many investors would be asking themselves how much income is enough to meet their financial requirements, particularly in the case of retirees. While this may increase the attraction of riskier fixed interest assets, there are significant trade-offs.

The reason investors continue to hold high quality fixed interest assets with some duration is for the benefit of ‘portfolio insurance’. Quite simply, these assets will produce higher returns when riskier assets like high yielding debt and equities fall in tandem. Like most insurance, it appears somewhat costly under normal conditions, but reduces detrimental outcomes when the unpredictable inevitably occurs.

Higher quality credit assets play a role as a portfolio diversification tool which could prove particularly important should market speculation about a potential recession translate into further volatility, a drawdown in asset prices or restricted liquidity.