Subscribe

Sign up for timely perspectives delivered to your inbox.

Last week’s MPC communications and recent data suggest a cut in Bank rate at the next meeting on 19 December.

The MPC’s latest forecast signals an easing bias: inflation is projected to be below the 2% target in two years’ time (at 1.89%), assuming an unchanged 0.75% level of Bank rate. This contrasts with the August forecast, when the two-year-ahead projection was above 2% (2.10%).

The MPC was understandably reluctant to cut rates, or pre-commit to a reduction, at the start of a general election campaign. The two dovish dissents, however, underlined the shift of opinion signalled by the inflation forecast.

The economy may yet be shown to have entered a recession despite this week’s news of a 0.3% rise in GDP in Q3 (below a Bank staff estimate of 0.4%). The Q3 level was only 0.1% (0.07% before rounding) higher than Q1. Initial estimates tend to be revised down when the economy is weakening – recall the downgrade from +0.2% to -0.7% for Q2 2008, the first quarter of the last recession.

Monthly data show that GDP fell in August and September, and the September level was 0.1% lower than March. GDP is currently estimated to have surpassed the March level for a single month in July but this is questioned by data on total hours worked in the economy, which fell by 0.5% between the three-month periods centred on March and July respectively.

The MPC’s forecast implies high recession risk, with an assessed probability of 31% that GDP in Q1 2020 will be lower than in Q1 2019.

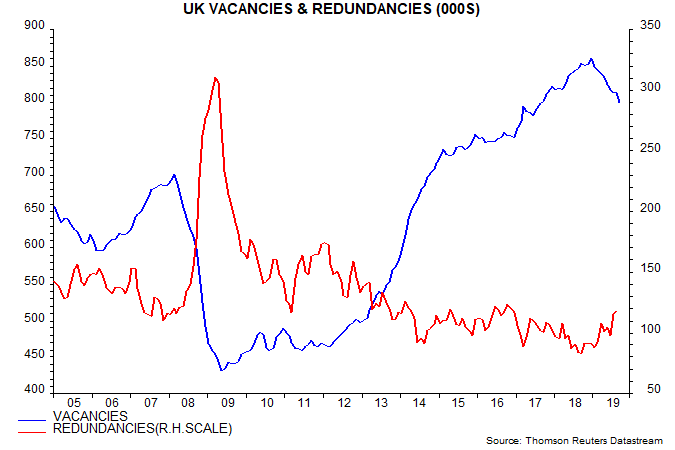

Data since the MPC meeting support the case for easing. As well as the GDP undershoot, yesterday’s labour market report showed a cooling of earnings growth along with a further fall in vacancies and rise in redundancies – see first chart.

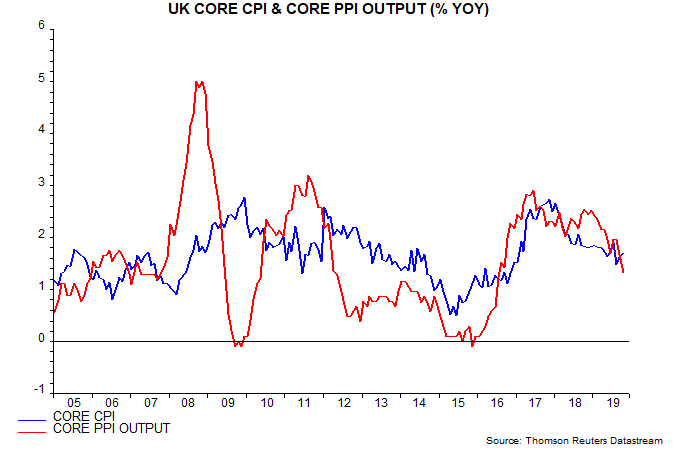

CPI inflation fell to 1.5% (1.46% before rounding) in October, consistent with the MPC forecast of a 1.42% average in Q4. The decline reflected gas and electricity price cuts, with the core rate – defined here to exclude energy, food, alcohol, tobacco, education and estimated VAT effects – edging up to 1.7%. Core PPI output inflation, by contrast, fell further and usually leads CPI trends – second chart.