Knowledge. Shared Blog

October 2019

“Whatever It Takes:” Reflecting on Mario Draghi’s Run as European Central Bank President

-

Oliver Blackbourn, CFA

Oliver Blackbourn, CFA

Portfolio Manager

Oliver Blackbourn, a Portfolio Manager on the UK-based Multi-Asset Team, comments on the departure of Mario Draghi as ECB president as the central bank itself potentially reaches the limits of what can be achieved through monetary policy.

Key Takeaways

- Next week, Mario Draghi will leave the European Central Bank (ECB) after eight years as the bank’s president.

- Mr. Draghi will likely be remembered as a dynamic central banker who was prepared to push boundaries, famously stating that the ECB would do “whatever it takes” to preserve the euro at the height of the eurozone debt crisis.

- In our view, the ECB now appears to be reaching the limits of its monetary policy toolkit, and any future slowdown is likely to require government fiscal action rather than further monetary policy easing.

As Mario Draghi’s tenure as president of the European Central Bank (ECB) comes to an end, it is becoming increasingly clear that the central bank may be reaching the limits of its monetary toolkit. The “whatever it takes” stance Mr. Draghi set forth as the ECB’s mandate at the height of the eurozone debt crisis is quickly turning into “whatever they can do.” The truth seems to be that there is only so much a central bank, hemmed in by competing interests and ideology, can achieve with its monetary policy mandate.

Mr. Draghi’s persistent calls for structural reform have gone unheeded, but any future slowdown is likely to require government fiscal action rather than further monetary policy easing.

Despite the seemingly fractious end to his time in office, Mr. Draghi is likely to be remembered as a dynamic central banker, prepared to push the boundaries when others hesitated. Whether you agree with the policy decisions or not, he was prepared to act – and to drag colleagues and politicians with him. However, Mr. Draghi may be leaving at an appropriate time, as it is difficult to see how much more innovative the ECB can be within the restrictions of its mandate. Interest rates sit well below zero, and quantitative easing has already pushed various major European sovereign bond market yields into negative territory.

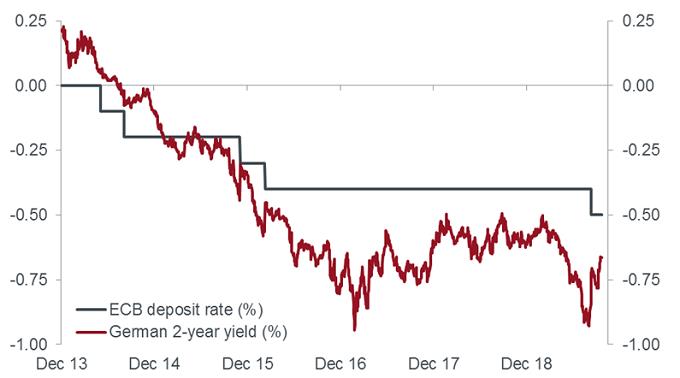

The chart below shows that the policy-sensitive two-year German bund yield has moved within a fairly narrow range for the last three years, suggesting that policy has been reaching a limit. At the same time, concerns have risen about the negative consequences of such environments and whether continuing to ease further would actually be helpful to the real economy.

Finding the Limits of ECB Monetary Policy

[caption id=”attachment_245046″ align=”alignnone” width=”680″] Source: Janus Henderson Investors, Bloomberg, as of 10/22/19. Past performance is not a guide to future performance.[/caption]

Source: Janus Henderson Investors, Bloomberg, as of 10/22/19. Past performance is not a guide to future performance.[/caption]

At the start of ECB press conferences on monetary policy decisions, we have habitually seen Mr. Draghi call for eurozone governments to take action on structural reform to boost growth. With this plea having fallen on deaf ears, fiscal stimulus may now remain the only meaningful action left to counteract a future slowdown in the eurozone economy.

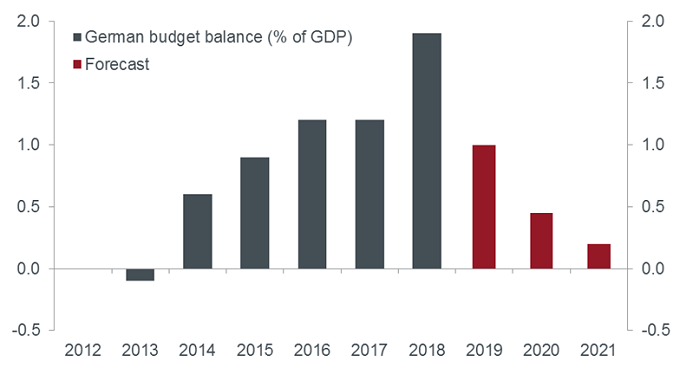

Whereas other central banks may look to help governments finance future fiscal stimulus via low borrowing costs, any suggestion of this within the strict boundaries of the eurozone’s rules would prove highly controversial. In addition, the budget and debt limits set out under the Maastricht Treaty mean that many larger eurozone countries have limited room to maneuver on the fiscal front. Germany is an exception following its commitment to a budget surplus in recent years, as shown in the chart below.

Slowly Shifting Away from the German Budget Surplus

[caption id=”attachment_245057″ align=”alignnone” width=”680″] Source: Janus Henderson Investors, Bloomberg, as of 10/22/19[/caption]

Source: Janus Henderson Investors, Bloomberg, as of 10/22/19[/caption]

Attitudes appear to be changing, but it is a slow process. Investments in infrastructure and environmentally friendly projects are possible exceptions and may be the vanguard of a new regime of looser fiscal policy. Just don’t expect too much, too quickly.

The implications of a shift to fiscal easing may be profound. Despite likely being anchored by low interest rates, bond markets could begin to price in greater future inflation and higher real yields due to the expectation for stronger economic growth. With yield curves steepening as longer-term yields rise, we would expect to see more cyclical stock markets, such as the eurozone, outperform. However, we are, at best, seeing the first signs of a change in attitude – there is still a lot of resistance to overcome before this becomes reality. In the meantime, as Christine Lagarde replaces Mr. Draghi as ECB president, you have to wonder if the central bank has done almost everything it can do in terms of monetary policy.

Knowledge. Shared

Blog

Back to all Blog Posts

Subscribe for relevant insights delivered straight to your inbox

I want to subscribe