Subscribe

Sign up for timely perspectives delivered to your inbox.

Members of the Janus Henderson Australian Fixed Interest Team discuss Commonwealth Bank’s latest hybrid issue and why they are taking advantage of market conditions, breaking with the recent trend of Tier 2 debt issuance from the major banks.

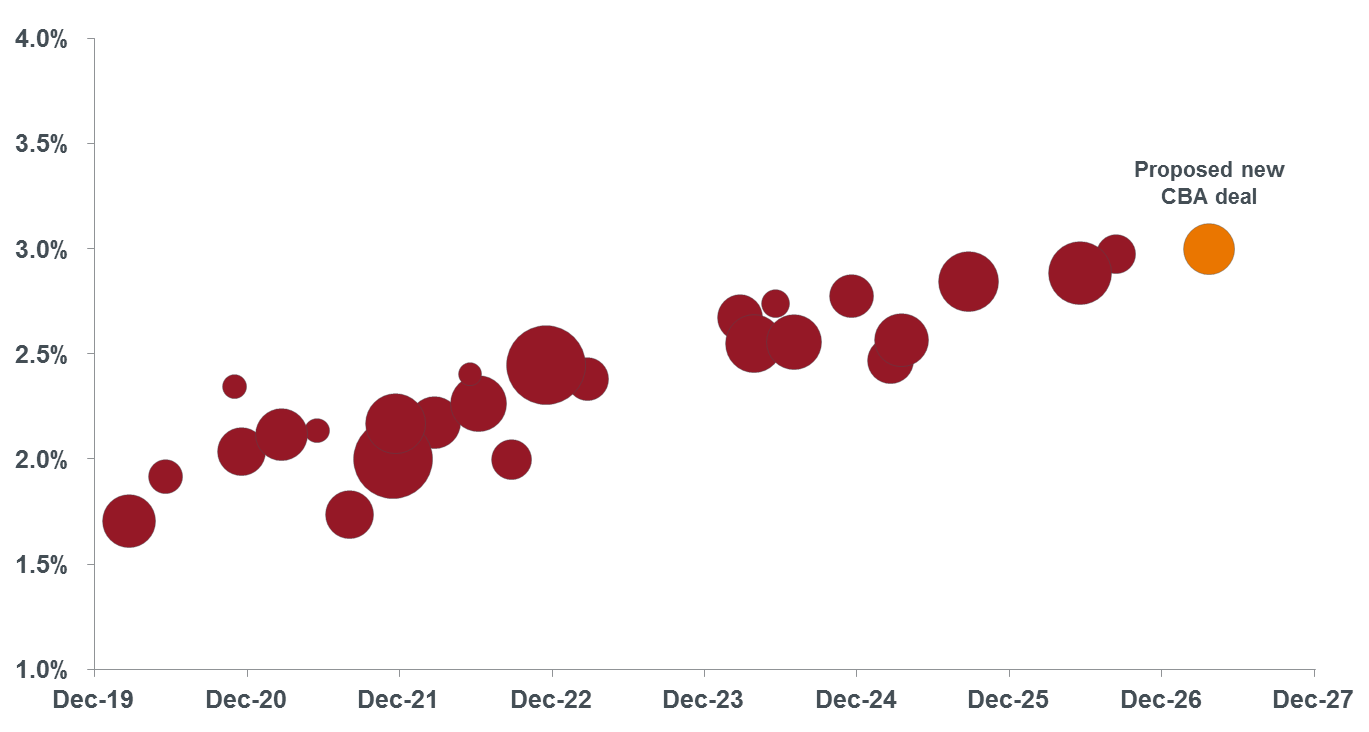

In its first hybrid issuance since November 2018, the Commonwealth Bank of Australia (CBA) has launched PERLS XII Capital Notes (PERLS XII), a new $1.25bn (upsized from the original amount of $750m) hybrid deal to be listed on the ASX under the code CBAPI. This new security will have a 7.5-year call date and is priced at a traded margin of 3.0% above the bank bill swap rate (BBSW).

This new PERLS XII security intends to raise new capital rather than refinance an existing hybrid security.

The deal was announced amid tailwinds for the hybrid market. An easing of investor concerns around franking credits sparked a post-election rally for bank hybrids that has been sustained by investors’ fierce global pursuit of yield and a general lack of hybrid issuance (combined with redemptions) in the market.

The latest CBA hybrid deal follows the issuance of Tier 2 securities by the major banks in either domestic or US dollar markets since mid-July as they moved to start meeting higher capital obligations after APRA introduced total loss absorbing capacity (TLAC) requirements. This requires the major banks to issue another 3% of loss absorbing capital, or approximately an additional $50bn collectively, by the start of 2024.

Given it makes commercial sense for the banks to seek the lowest cost route to meet their TLAC obligations, the market expected the issuance of Tier 2 debt to domestic and global investors after the prudential regulator introduced the measures. TLAC requirements can also be satisfied by issuing Tier 1 securities or via common equity, but these instruments are typically more expensive than Tier 2 securities.

However, beyond assisting with TLAC requirements, CBA’s decision to opt for issuing long-dated Tier 1 securities through its PERLS XII offer appears to be well-timed for a number of reasons, including:

Chart 1: Traded margins of Basel III Tier 1 capital instruments

Source: Janus Henderson, Evans & Partners as at 8 October 2019.

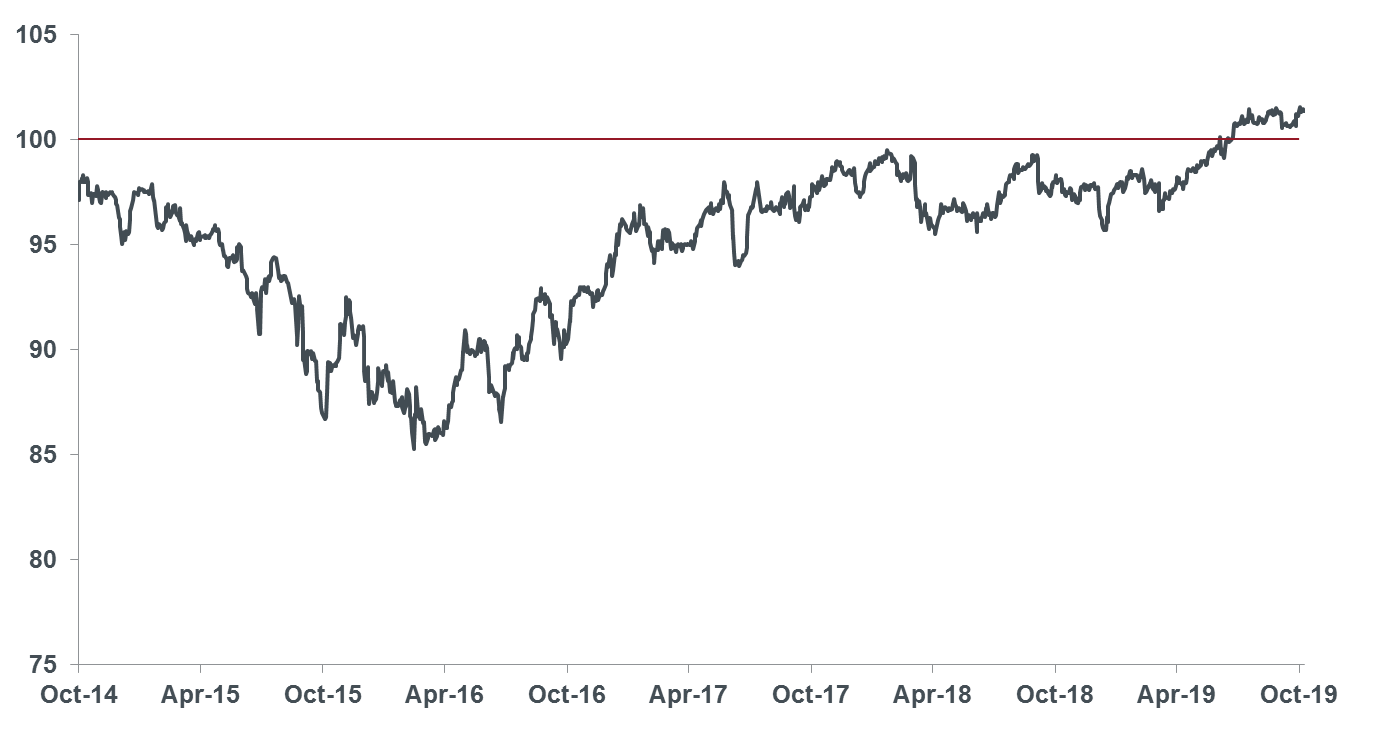

CBA has a history of favourably timed Tier 1 issuance (from the banks’ perspective). In 2014 CBA launched its PERLS VII issue (ASX: CBAPD) with a traded margin of 280 basis points (bps). Credit markets weakened as soon as the securities were priced (they closed on the first day of trading at $97.10) and it wasn’t until earlier this year, just under five years from launch, that the price recovered and traded above par. This is an opportune reminder that often the benefits to the issuer don’t always extend to investors.

Chart 2: PERLS VII (ASX: CBAPD) price history ($)

Source: Bloomberg. As at 8 October 2019.

Turning back to PERLS XII, this new CBA hybrid issue is a timely reminder that it’s important for investors to be conscious of whether they are receiving adequate compensation for term risk, especially in today’s low rate environment.

We would not be surprised to see the other major banks follow in CBA’s footsteps and this additional supply has the potential to place pressure on hybrid spreads and positively impact the Tier 2 market as prospective supply declines.