Subscribe

Sign up for timely perspectives delivered to your inbox.

Euroland September flash PMI results were disappointing but monetary trends continue to give a hopeful signal for economic prospects.

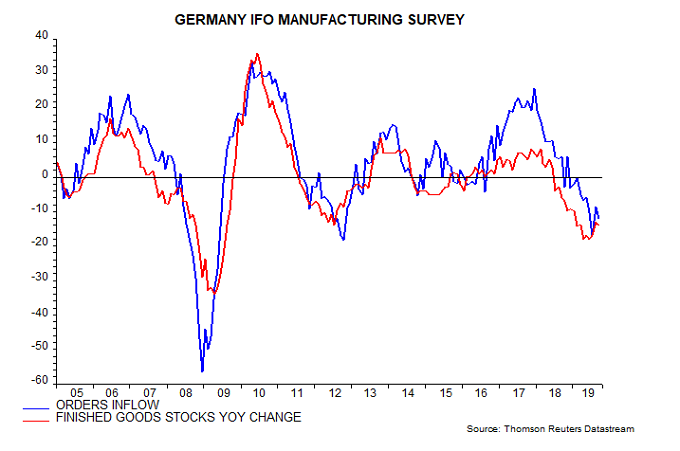

The expectation here has been that the manufacturing PMI would bottom out around Q3, reflecting a recovery in real money momentum from late 2018. Instead, the index fell to a new seven-year low in September – see first chart. Weakness was again focused on Germany, where the PMI has undershot its low during the 2011-12 Euroland recession; the French index, by contrast, continues to hold above 50. The German results, however, were questioned by the September Ifo manufacturing survey (which has a much larger sample size): the orders inflow balance and the rate of change of the finished goods inventories balance held above their recent lows – second chart. Both balances are components of the OECD’s German composite leading indicator.

Weakness was again focused on Germany, where the PMI has undershot its low during the 2011-12 Euroland recession; the French index, by contrast, continues to hold above 50. The German results, however, were questioned by the September Ifo manufacturing survey (which has a much larger sample size): the orders inflow balance and the rate of change of the finished goods inventories balance held above their recent lows – second chart. Both balances are components of the OECD’s German composite leading indicator.

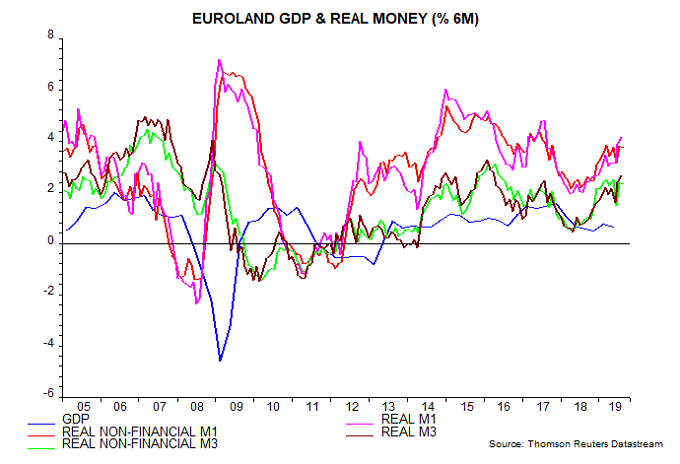

The ECB, meanwhile, today reported further hefty monthly gains in narrow and broad money in August. Six-month growth of real M1 and M3 (i.e. deflated by consumer prices, seasonally adjusted) rose to the highest levels since 2017 and 2016 respectively – third chart.

The headline measures have been boosted by faster growth of deposits held by financial institutions, which may reflect portfolio shifting in response to negative yields and have little implication for spending on goods and services. The forecasting approach here focuses on non-financial M1 and M3, comprising money holdings of households and non-financial businesses: six-month real growth of these measures remains well up on a year ago, though has not risen further recently.

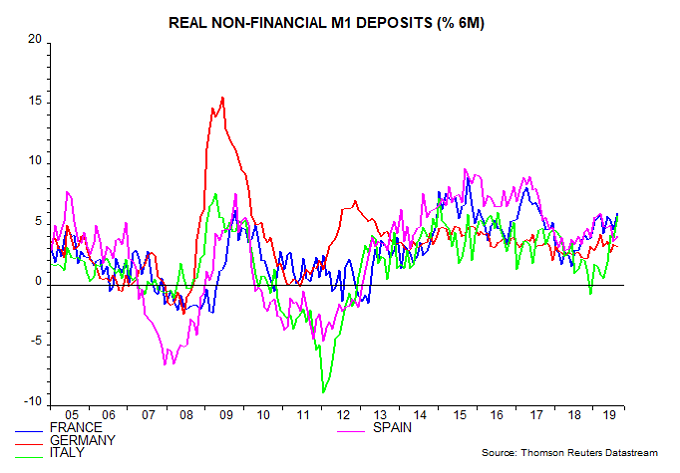

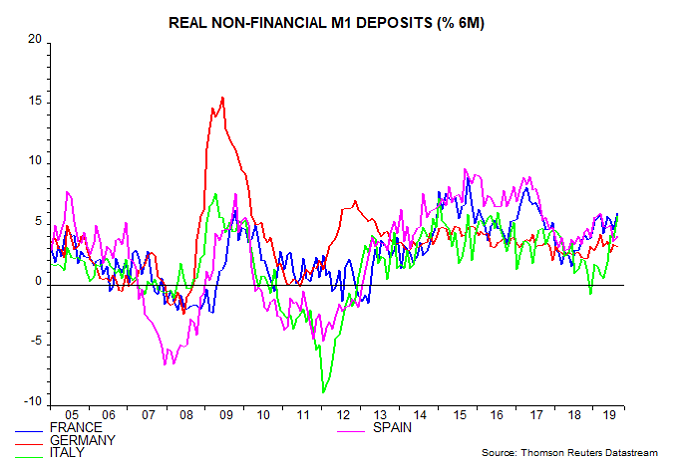

The country breakdown of M1 deposits show that real growth remains strongest in France – consistent with recent resilience in coincident economic data – and has picked up sharply in Italy, suggesting improving prospects. German growth continues to lag but remains solid.

Will the resumption of QE give a further boost to monetary trends? Scepticism is warranted: the announced programme is small – equivalent to 2.0% of GDP per annum – and liquidity created by earlier QE was largely exported and had little impact on M3.