Subscribe

Sign up for timely perspectives delivered to your inbox.

Nick Maroutsos, Co-Head of Global Bonds, sets out some of the reasons why Asia ex-Japan debt offers a potentially attractive destination for globally-minded bond investors.

For much of 2018, the allure of Asia ex-Japan bonds as a differentiated source of returns waned, while US yields grinded higher on the back of interest rate hikes by the US Federal Reserve (Fed) and expectations that Europe and Japan would eventually wind down their quantitative easing (QE) programmes. Subsequent developments, however, have breathed new life into the rationale for maintaining exposure to Asian debt. Slow growth forced Japan and Europe to delay monetary tightening and – after raising rates in December – the Fed pivoted to a more accommodative stance, sending Treasury yields lower across all maturities.

With 10-year Treasury yields at two-and-a-half-year lows, Asia ex-Japan debt can again be viewed as an attractive destination for globally-minded bond investors seeking to generate carry in a low return environment. This argument is further reinforced by the region’s sound fiscal position and the steady development of its capital markets.

To be sure, with the exception of a few basket cases, bond yields are low globally. This is a reflection of growth concerns in what has become an extended economic cycle and the consequence of investors again being nudged towards riskier asset classes by persistently easy developed market monetary policy. As of mid-June, the yield on the Bloomberg Barclays US Aggregate Bond Index (US Agg) – comprised of government debt, investment grade corporate bonds and securitised debt – was 2.63%. A corresponding benchmark in the eurozone (Bloomberg Barclays Euro Aggregate Bond Index) yielded 0.25%, and the yield on a global benchmark (Bloomberg Barclays Global Aggregate Bond Index) was 1.58%. A broad Asia ex-Japan bond index (Bloomberg Barclays Asia USD Investment Grade Bond Index), on the other hand, yielded 3.36%.

While yields are higher in absolute terms, of greater importance is the amount of return an investor potentially generates per unit of risk accepted. For the US Agg, with a duration¹ of 5.78 years, each unit of risk – as measured by a year of duration – carries with it 0.46% of yield. In Europe, a year of duration is accompanied by 0.04% of yield, while in Asia ex-Japan, it is a much more palatable 0.63%.

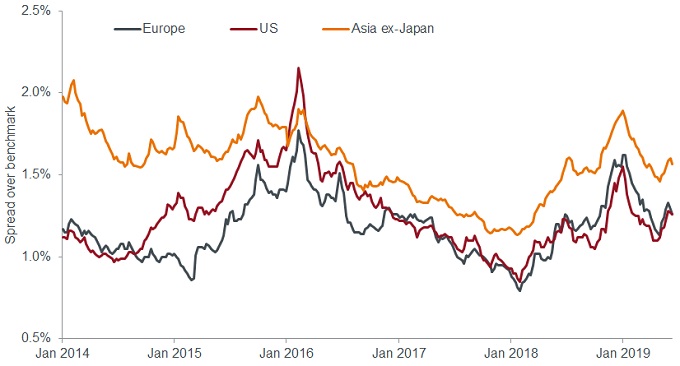

When one isolates investment grade corporates from the broader bond universe, this advantage is even more pronounced given the presence of the credit risk premium. Spreads on Asia ex Japan investment grade corporates were 156 basis points² (bp) over their respective benchmark as of mid-June compared to 126bp in both the US and Europe. On a yield-per-unit of risk basis, one year of duration in Asia ex Japan corporates is matched with 0.77% of yield; in the US and Europe, the figures for investment grade corporates are 0.44% and 0.16%, respectively.

Chart 1: Regional investment grade corporate spreads over risk-free benchmarks

[caption id=”attachment_222938″ align=”alignnone” width=”680″] Source: Bloomberg, as at 14 June 2019[/caption]

Source: Bloomberg, as at 14 June 2019[/caption]

Furthermore, many of the region’s corporations are linked to the secular themes that are fuelling economic growth and reconfiguring societies. For example, over the past five years, nearly 50% of the region’s investment grade bond issuance has emanated from the financial sector. Key drivers are an increase in personal banking and growing usage of retirement programmes and insurance products as the region’s population seeks to protect its newfound wealth. A more robust regulatory framework in the wake of the late 1990s Asian Financial Crisis increased bondholder protections, and the infrastructure of debt markets has improved. Insurance companies and pension funds have also created natural buyers for domestic debt, adding additional liquidity to capital markets.

While the financial sector and government debt dominate new issuance, other sectors have also increased their presence in bond markets, among them industrials, utilities and energy companies. Many of these are tied to the region’s infrastructure boom and are often backed by high value physical assets and, in many cases, implicit government support. Banking, infrastructure and the increasing spending power of the consumer – with consumer discretionary companies being another source of new bond issuance – are all components of the region’s multi-year effort to advance its economies. Given these tailwinds, along with improved corporate governance, we believe that the credit premium, or the additional yield commanded by investors for holding these bonds over government bonds, may overstate the risks attached to Asian corporate issuers. Consequently, the persistently higher spreads these securities have provided compared to their developed market peers reinforce the argument that this asset class can serve as a source of attractive risk-adjusted returns.

As with the credit risk premium, the liquidity premium embedded in the region’s corporate bonds may not accurately reflect positive recent developments. An increasing base of domestic buyers, in addition to international investors on the hunt for yield, have added depth to erstwhile shallow markets and, in the process, drawn in additional investors previously concerned about liquidity. Inclusion in global benchmarks has further improved market function as passive strategies must increase exposure to the region to match its rising share in global benchmarks.

International investors often prefer to purchase bonds denominated in hard currency, and the market has evolved to meet that need. In the seven years leading up to 2017, investment grade bonds issued in G3 currencies (euro, US dollar and Japanese yen) rose more than fourfold to US$231 billion. And while issuance slipped in 2018, it still exceeded US$200 billion for the second year running.

Chart 2: Asia ex-Japan G3 currency bond issuance

Source: Bloomberg, annual data, as at 31 December 2018. Denotes issuance across all credit ratings.

China has dominated corporate issuance, representing nearly 60% of total investment grade issuance over the past five years, but other countries have also expanded their bond markets. South Korea, Hong Kong, Indonesia and India have each issued more than US$40 billion in investment grade debt over the past five years.

The region’s relatively strong fiscal position also adds to the argument that the credit risk premium currently assigned to it is overblown. A risk of holding hard currency debt is the mismatch between currencies in which an issuer’s revenues are generated and obligations are paid. With a country’s fiscal position a potential weight on its currency, hard-currency investors must be mindful of macro factors when selecting regions in which to invest. But here, many Asian countries pass the test as their ratios of total debt to gross domestic product (GDP) fall well below those of developed markets.

The rumours of QE’s demise were greatly exaggerated. Again faced with low yields in home markets, investors are seeking value where available. Just as during the years following the Global Financial Crisis, the Asia ex-Japan region looks to be an important source of global growth – and of investment returns. Still, risks remain. Implicit in low yields is a slowing global economy. Given connected supply chains, Asia would likely not escape a downdraft. A slowdown, however, is not the same as a recession. And while growth may subside, the secular themes propelling the region’s growth are largely linked to the consumer and infrastructure, putting Asia at an advantage over commodity-producing regions that would more acutely feel the brunt of an end to the global economic cycle.

1Duration measures the sensitivity of a bond’s price to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

2Basis point (bp) equals 1/100 of a percentage point. 1bp = 0.01%, 100bp = 1%.