Subscribe

Sign up for timely perspectives delivered to your inbox.

The US Federal Reserve’s policy shifts have helped support markets in 2019. US Fixed Income managers, Darrell Watters, Mayur Saigal and Mike Keough, share their views on the likelihood, timing and scale of any rate cuts in the coming months.

From the Federal Reserve (Fed)’s January pause to its June pledge to “act as appropriate to sustain the expansion,” Fed policy shifts have helped support markets in 2019. While the US Treasury market has rallied and interest rates have declined significantly on concern that the Fed’s more accommodative policy is driven by weakening economic conditions, risk markets, including equities and corporate credit, have honed in on the potential benefits of rate cuts.

Interest rate cuts may ultimately be supportive for the US economy but investors should be careful what they wish for, given that what drives them typically is not. The Fed’s ability to engineer a soft landing is a delicate task, and as the tug of war between slowing growth and easing monetary policy plays out over the next few quarters, it is likely to be accompanied by periods of heightened uncertainty.

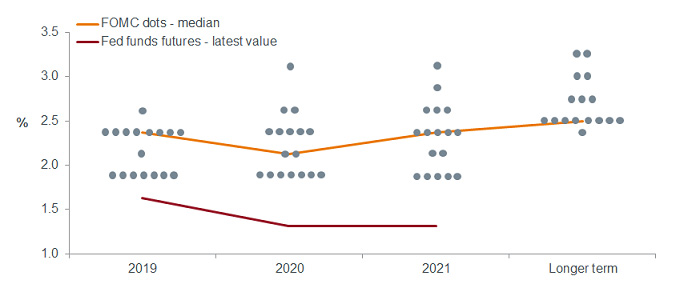

Futures markets are dovish but Fed is data dependentUS gross domestic product (GDP) growth registered 3.1% in the first quarter of 2019, corporate earnings — while decelerating — are still growing, unemployment is at a multi-decade low, wage pressures are contained and consumer spending remains strong. The assumption that the Fed will implement an insurance cut to reverse the current mid-cycle slowdown amid a constructive economic landscape could ultimately lead to disappointment, particularly when projections of the Federal Open Market Committee (FOMC), the Fed’s policymaking body, are still skewed towards holding rates steady through year end as shown in chart 1, with only one cut in 2020.

Chart 1: FOMC projections versus fed funds futures

Source: Bloomberg, as at 21 June 2019

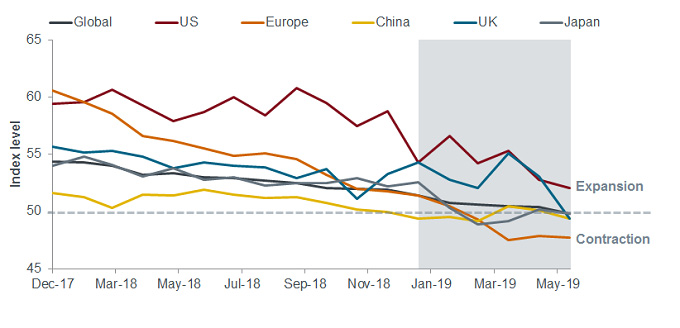

Trade — the biggest threatDespite the Fed’s pivot and China’s recent stimulus, global manufacturing data has continued to decline this year, as highlighted in chart 2. While the US is hovering just above the critical level of 50, many regions have dipped into contraction territory. This picture is unlikely to improve if trade tensions further weigh on business confidence and preclude business investment.

Chart 2: global manufacturing data continues to soften; impetus for a Fed cut in 2019?

[caption id=”attachment_222854″ align=”alignnone” width=”680″] Source: Bloomberg, as at 31 May 2019[/caption]

Source: Bloomberg, as at 31 May 2019[/caption]

The US and China may have come close to an agreement in May but negotiations remain challenged, as these economic superpowers seek to alter policies that were decades in the making. In addition, as the Trump administration sets its sights on other regions, and the rules of the game remain in flux, businesses are having a difficult time making investment decisions. If these headwinds generate concerns of a corporate earnings recession, confidence in the Fed’s ability to engineer a soft landing could wane, in which case we would expect risk assets to reverse course.

A potential change in frameworkAverage inflation targeting — targeting 2% over a specified time period — is the solution that has accumulated the most support. This framework would result in the Fed maintaining easy monetary policy until inflation rises, and to offset sustained periods of below-target inflation, allowing above-target inflation for a period of time without raising rates. We would expect a change in policy of this nature to be very well telegraphed and implemented in a slow and methodical manner, making it an unlikely event for 2019.

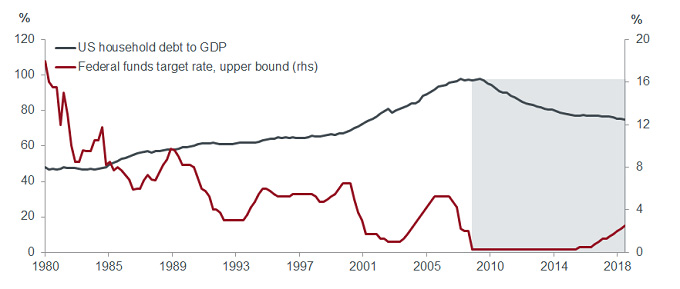

When the cuts come, will they be enough?It also remains to be seen how the consumer will react to rate cuts given the differences that have emerged in consumer habits following the Global Financial Crisis. As rates have steadily declined, consumers have actually been borrowing less as shown in chart 3 and consumer spending has been relatively constrained. During the impending rate cut cycle, lower rates and consumer spending (the primary driver of the US economy) may not provide the level of stimulus they have in cycles past.

Chart 3: consumer borrowing has declined in the low rate environment

[caption id=”attachment_222843″ align=”alignnone” width=”680″] Source: Bloomberg, as at 31 December 2018[/caption]

Source: Bloomberg, as at 31 December 2018[/caption]

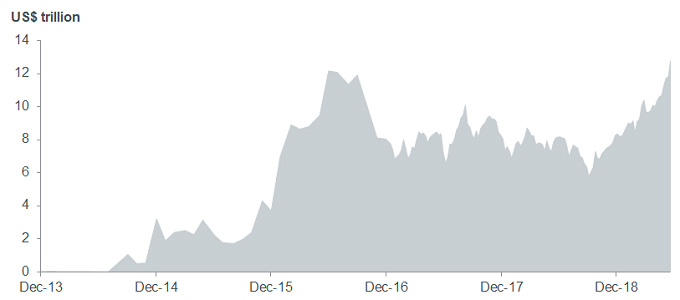

US Treasury yields have trended significantly lower and can go lower still as a result of the Fed pivot, expectations of a lower neutral rate¹ in the US and the potential for renewed accommodation by the ECB. Nearly $13 trillion of negative yielding debt around the globe (chart 4) and an insatiable search for yield are also contributing to strong demand for US government and corporate bonds.

Chart 4: negative yielding debt has ballooned in the era of ultra-accommodative policy

[caption id=”attachment_222832″ align=”alignnone” width=”680″] Source: Bloomberg, as at 21 June 2019

Source: Bloomberg, as at 21 June 2019

Note: Bloomberg Barclays Global Aggregate negative yielding debt, market value in USD. The Bloomberg Barclays Global Aggregate Bond Index is a broad based measure of the global investment grade fixed rate debt markets.[/caption]

Supply/demand technicals also remain favourable for US investment grade corporate credit. After a wave of mergers and acquisitions, we are witnessing a heightened focus on debt repayment and less willingness by management teams to take debt and leverage higher as they have in recent years. Further, while the US economy is slowing, employment and corporate fundamentals remain relatively robust. Given these conditions, it is difficult to envision a sustained a sell-off in corporate credit without recession risks and default rates trending higher. However, there is no doubt that the landscape can change quickly.

As markets await a resolution on trade and the tug of war between slowing growth and accommodative monetary policy wages on, investors may benefit from seeking active managers with the ability to distinguish between short-term volatility events and growing systemic issues. Managers with the ability to adjust portfolios accordingly may be better suited to take advantage of strong risk-adjusted opportunities while the threat of recession remains at bay, and also to avoid the trouble spots that will get hit the hardest when things come unglued.

1The neutral rate is the interest rate that supports the economy at full employment/maximum output while keeping inflation constant.