Subscribe

Sign up for timely perspectives delivered to your inbox.

Janus Henderson Value Plus Income Fund combines fundamental fixed income and high-quality equities in an effort to provide capital appreciation and current income while minimizing downside risk. In a recent interview, Ted Thome, CFA, portfolio manager of the Fund’s equity sleeve, explained why their defensive value approach to fundamental investing is critical to fund performance, particularly in the later stage of the market cycle.

We use a defensive value approach in managing the Fund. Our philosophy is to mitigate the downside, which should help us outperform over a full market cycle with less risk as measured by beta, standard deviation and downside capture. Our process involves investing in what we believe are high-quality companies that are temporarily out of favor, yet have strong balance sheets, stable free cash flow, competitive moats and strong management teams. In terms of selecting individual stocks, we’re focused on being defensive and mitigating downside. We conduct a reward-to-risk evaluation for every security we own using a framework we’ve developed to estimate downside and upside targets. In every case, we want that reward skewed in our favor.

Our focus on defensiveness is an important distinction. There are many value managers who operate in a style we would call “deep value” or those trading at significant discounts to valuations. However, we’re much more focused on high-quality companies with positive secular trends, competitive advantages and, most importantly, defensive characteristics in the event of an economic downturn. We want to make sure they don’t have too much downside at the sector, company or macro level. It’s essential that improvement be in their line of sight.

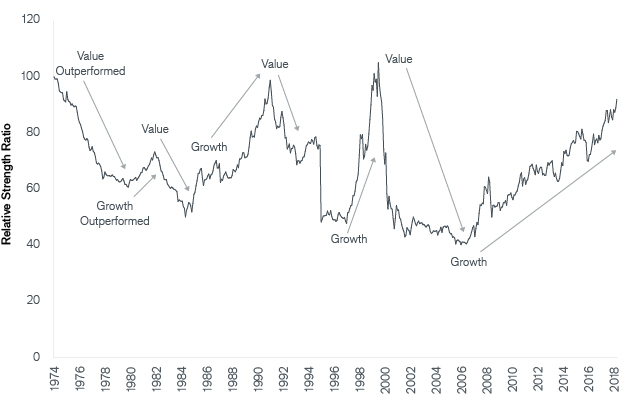

We’re later in the market cycle and valuations are high based on historic measures, so, yes, we think our approach is a good match for current market conditions. We’re actively looking at stocks that we believe have less downside risk than the market. With our approach, we aim to provide an element of capital preservation in a bear market while participating in the upside if the bull market continues. Due to the defensive nature of our portfolio, we may lag in strong bull markets. It’s worth noting that the growth style has outperformed value for more than a decade. History suggests this will reverse at some point. Although we don’t know exactly when that will happen, we believe we are closer to an inflection point.

Our current allocation to equity as of March 31, 2019, is 42%, with futures calculated at market value. The Fund’s prospectus calls for a range of 40%-50%, which makes 45% the neutral level. Being at 42%, it’s a few hundred basis points below the neutral level, which indicates that equity investment opportunities are not that compelling or attractive from a risk/reward perspective at this point in time.

Our bottom-up risk/reward analysis reinforces our feeling that we’re late in the cycle and we have to be more cautious. We’re not sure when the market is going to reverse, but in our view the risk of a reversal is getting greater.

We don’t make sector calls; however, using our bottom-up approach to portfolio construction, we are finding opportunities in health care, financial services and real estate. As of April 30, 2019, the portfolio is overweight those sectors compared to the Russell 1000® Value Index benchmark.

In financial services, we are seeing some opportunities in regional banks located in the smaller markets of high-growth regions. Within health care, the portfolio has a big exposure to health care services. As for real estate, we have overweight exposure within specialized Real Estate Investment Trusts (REITs).

Both sleeves are focused on income. The Fund’s equity investments can include companies of any size that we believe have the potential for high relative dividend yields. As of April 30, 2019, the dividend yield of the Fund’s equity portfolio was 2.64%. The Fund’s SEC yield with and without waivers, as of the same date, was 3.09% and 2.56%, respectively.

View Current Yield and PerformanceThere are three that come to mind. One would be tax-deferred retirement accounts, such as IRAs and 401(k)s. They benefit from tax efficiency since the Fund distributes income monthly. Second would be investors looking for defensive monthly income. Third, and more broadly, would be investors looking to rotate into something more conservative. Many of these investors have had great equity performance over an extended period of time but are starting to worry about the market. The Fund offers those concerned about the market a way to stay invested. They get the potential for monthly income and capital appreciation with historically less downside risk than long-only equity exposure.

Value stocks can continue to be undervalued by the market for long periods of time and may not appreciate to the extent expected.