Subscribe

Sign up for timely perspectives delivered to your inbox.

“It’s tough to make predictions, especially about the future.” While never quite definitively attributed (Yogi Berra?), this familiar bit of humor and wisdom has nevertheless stood the test of time.

Consider a 2013 paper by Itzhak Ben-David, John R. Graham and Campbell R. Harvey, which found the range of outcomes that corporate CFOs provide for one-year stock market forecasts tend to be unrealistically narrow. Over a 10-year period, a panel of CFOs were asked to estimate market return probability ranges that would lead them to be right 80% of the time. However, instead of working 80% of the time, barely more than one in three was correct. The authors note that executives are severely miscalibrated and too sure of their ability to predict the future.1,2

The specter of overconfidence could also loom over decisions to buy dips in the stock market. At its core, “buy the dip” is a speculation that the next move in the market will be higher, thus making the decline (dip) a buying opportunity. It has worked for what seems like a very long time now – nearly 10 years into the current bull market. But, about those predictions … if the CFOs don’t know, then investors should ask themselves whether they really know what the future holds.

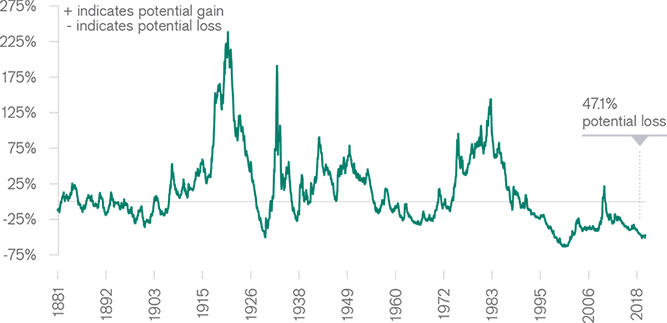

There is also risk of buying, not a mere dip, but rather a prelude to a more serious market decline. Here, the scenario goes from bad to worse for the dip buyer: a reversion to the long-term median cyclically adjusted price-to-earnings (P/E) ratio for the S&P 500® Index has rarely suggested a worse potential loss. For investors who aim to compound returns over the long haul and who cannot tolerate significant losses along the way, buying the dip simply won’t cut it as an investment strategy. We suggest an alternative approach: Don’t buy the dip. Evaluate the dip and buy bargains.

Source: Robert Shiller, http://www.econ.yale.edu/~shiller/data.htm. As of 10/31/18. Median cyclically adjusted P/E (CAPE) is 16.2x over the entire data set. S&P 500 Index at 2,711 is CAPE of 30.6x, suggesting a 47.1% potential loss.

Our investment team at Perkins is evaluating the equity market’s recent dip by reviewing the weakest areas (i.e., stocks with the biggest price declines). As a general matter, it seems that concerns about the duration of the economic cycle are spreading, and each particular sector and industry has its own dynamic to consider. For example, semiconductors & semiconductor equipment was recently the single worst-performing industry group within the MSCI World IndexSM, losing roughly 13% in the three months ended October 31. After several years of surging demand and record profits, companies are now seeing falling prices for memory chips, declining orders for equipment and weakening end demand.

Other areas seeing big declines include several materials and automobile and automotive components companies that have recently warned on earnings due to rising input costs, falling demand and trade war developments. Banks are also under pressure – in Europe on GDP deceleration and euro turbulence caused by Italy, and in the U.S. on weak loan growth and higher funding costs. Aggregating across the market’s laggards, the stock market consensus appears to be grappling with the idea that we may have passed the peak of the current expansion and benign investing environment.

In our opinion, as trading conditions become more volatile and sellers more fearful, the likelihood of identifying bargain stock prices grows. Pain on the other side of the trade is the first, but not the only, criteria for the bargain hunter. Second, the company should have a durable competitive advantage, such that, over time and through market cycles, it will be able to earn more than its fair share of profits. Third, the balance sheet should be well capitalized and liquid to enable the company to endure a much more difficult operating environment should that scenario lie ahead. Finally, a stock’s price should be low enough relative to a company’s earnings power/net asset value to offer a margin of safety (should the market environment weaken further) and attractive return potential (over the long term).

In addition to orienting our research effort around identifying stock bargains, we are mindful of correlations across the various cyclical exposures in our portfolios, as well as the aggregate weights we have in those areas. Given that we don’t know whether the economy and/or market are at the beginning of a major downturn – remember the CFOs and their too narrow predictions! – we are attempting to make our buys slowly and cautiously, particularly in the more cyclical areas of the market. At some point, the bull market will end, and divine patience may prove the most important investing attribute of all.

Thank you for your co-investment with Perkins Investment Management.

Gregory Kolb

Chief Investment Officer,

Portfolio Manager 1 https://www.nber.org/papers/w16215

2 https://www.fuqua.duke.edu/duke-fuqua-insights/executives-hugely-overconfident